To call the stock market of this past week “a dog” probably isn’t being fair to dogs.

To call the stock market of this past week “a dog” probably isn’t being fair to dogs.

Most everyone loves dogs, or at least can agree that others may be able to see some positive attributes in the species. It’s hard, however, to have similar equanimity, even begrudgingly so, toward the markets this week.

What started off strongly on Monday and somehow wasn’t completely disavowed the following day, devolved unnecessarily on Wednesday and without any strong reason for doing so.

In fact, it was a week of very little economic news. We were instead focused on societal news that likely made little to no impression on the markets as a whole, although one sector did stand out.

That sector was health care, as the Supreme Court’s decision on the Affordable Care Act was a re-affirmation of a key component of the legislation and delayed any need to come up with an alternative, while still allowing Presidential contenders to criticize it heading into election season.

That’s a win – win.

It also keeps the number of uninsured at their lowest levels ever and puts more money in the pockets of hospitals and insurers, alike.

That’s another win – win.

While those two are usually on the opposite sides of most health care related arguments investors definitely agreed that the Affordable Care Act was and will continue to be additive to their bottom lines.

There is no health care flag, however.

The “Rainbow Flag” got a big thumbs up last week as the Supreme Court re-affirmed the right to dignity and the universal right to have access to divorce courts. The Court’s decision and its impact on businesses and the economy was a topic of speculation that was designed to fill air time and empty columns in the business section, as it came on a quiet day to end the week.

The Confederate Flag, of course, got a big thumbs down, after 150 years of quiet and thoughtful deliberation over its merits and what it represented. The decision by major retailers to stop sales of items with the Confederate flag on them can only mean that their demand wasn’t very significant and those items will probably be sent overseas, just as is done with the tee shirts of the losing Super Bowl team, so we can expect to see lots of photos of strangely attired impoverished third world children in the future.

And that leaves Greece, the EU, the IMF and the World Bank. For those most part, those aren’t part of our societal concerns, but they do concern markets.

Just not too much this past week.

The European Union was very forward thinking in the design of its flag. Rather than being concrete and having the 12 stars represent its member nations, those stars are said to represent characteristics of those member states. In other words Greece could leave the EU and the flag remains unchanged. Although the symbolism of the stars being arranged in a circle to represent “unity” may have to come under some scrutiny.

The growing realization is that would likely not be the same for the EU itself, as an exit by Greece would ultimately be “de minimis.” Either way, we should get some more information this week, as IMF chief Christine Legarde’s June 30th line in the sand regarding Greece’s repayment is quickly approaching.

It may be too late for a proposed “Plan B” for Greece to prevent default, as the European Union is now in its 86th trimester.

Still, despite a week of little news, somehow it was another week of pronounced moves in both directions that ultimately managed to travel very little from home.

New and existing home sales data suggested a strengthening in that important sector and the revised GDP indicated that the first quarter wasn’t as much of a dog as we all had come to believe. But there really wasn’t enough additional corroborating data to make anyone jump to the conclusion that core inflation was now exceeding the same objective that Janet Yellen had just stated weren’t being met.

So any concerns about improving economic news shouldn’t have led anyone to begin expressing their fears of increased interest rates by selling their stocks.

But it did.

Wednesday’s sell-off followed the news that the revised 2015 first quarter GDP was only down by 0.2% and not the previously revised 0.7%.

That makes it seem as if nerves and expectations for a long overdue correction or even a long overdue mini-correction are ruling over common sense and rational thought.

As usual, the week’s poten

tial stock selections are classified as being in Traditional, Double-Dip Dividend, Momentum or “PEE” categories.

The coming week is a holiday shortened one and will have the Employment Situation Report coming on Thursday, potentially adding to interest rate nervousness if numbers continue to be strong.

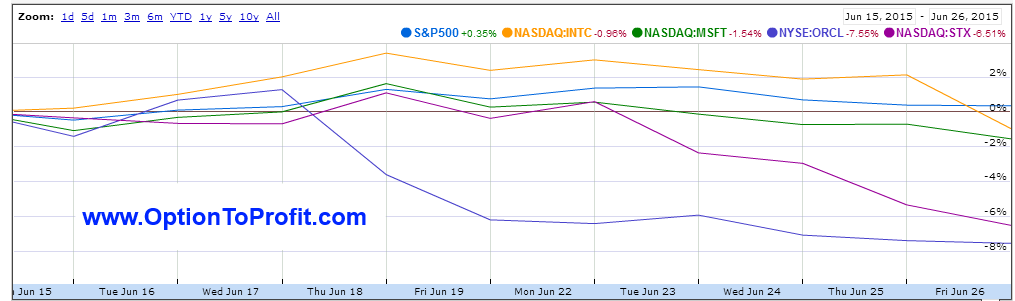

After Micron Technology’s (NASDAQ:MU) earnings disappointment last week it may be understandable why a broad brush was used within the technology sector to drive prices considerably lower on Friday. However, it wasn’t Micron Technology that introduced the weakness. The past two weeks haven’t been particularly kind to the sector.

At a time that I’m under-invested in technology and otherwise very reluctant to commit new funds, the sector has a disproportionate share of my attention in competition for whatever little I’m willing to let go.

With Oracle (NYSE:ORCL) having also recently reported disappointing earnings and Intel (NASDAQ:INTC), Microsoft (NASDAQ:MSFT) and Seagate Technology (NASDAQ:STX) reporting in the next 3 weeks, it may be an interesting period.

While Micron Technology brought up concerns about PC sales, they are more dependent upon those than some others that have found salvation in laptops, tablets and mobile devices.

What was generally missing from Micron’s report, however, was placing the blame for lower revenues on currency exchange, unlike as was just done by Oracle. Micron focused squarely on decreasing product demand and pricing pressure.

That lack of adverse impact from currency exchange is a theme that I’m expecting as the upcoming earnings season begins. Whereas the previous earnings reports provided dour guidance on expectations of USD/Euro parity, the Dollar’s relative weakness in the most recent quarter may provide some upside surprises.

With share prices in Microsoft and Intel having dropped, this may be a good time to add positions in both, as they could both be significant beneficiaries of an improvement in currency exchange, as both await any bump coming from the introduction of Windows 10. I haven’t owned shares of Microsoft for a while and have been looking for a new entry point. At the same time, I do own shares of Intel and have been looking for an opportunity to average down and ultimately leave the position, or at least underwrite some of the paper losses with premiums on contracts written on an additional lot of shares.

While Seagate Technology doesn’t report its earnings until July 15th, following its weakness over the last 7 weeks, I’m considering the sale of puts in the weeks in advance of earnings. Those premiums are elevated and will become even more so during the actual week of earnings. In the event of an adverse price move, there might be a need to rollover the puts to try and avoid or delay assignment. However, at some point in the August 2015 option cycle the shares will be ex-dividend, so a shift in strategy, pivoting to share ownership maybe called for if still short the put options.

While Oracle and Cisco (NASDAQ:CSCO) don’t report earnings for a while, both have upcoming ex-dividend dates that add to their appeal. In the case of Oracle, it’s ex-dividend date is on Monday of the following week, which opens the possibility of ceding the dividend to early assignment in exchange for getting two weeks of premium and the opportunity to recycle proceeds from an assignment into another income producing position.

Also going ex-dividend on the Monday of the following week is The Gap (NYSE:GPS). It is one of my favorite stocks, even though it rarely seems to be doing anything right these days.

Part of its allure is that it continues to provide monthly sales data and the uncertainty with those report releases consistently creates option premium opportunities usually seen only quarterly for most stocks as they prepare to release earnings.

As long as The Gap continues to trade in a range, as it has done for quite some time, there is opportunity by holding shares and serially selling calls, while collecting dividends, as the company attempts to figure out what it wants to be, as it closes stores, yet announces plans to take over the Times Square Toys ‘R Us location, for those NYC tourists that just have to jet a pair of khakis to remember their trip.

Finally, American Express (NYSE:AXP) goes ex-dividend this week. It has been extremely range bound ever since the initial shock of losing its co-branding relationship with Costco (NASDAQ:COST) in 2016.

My wife informed me this morning that after about 30 years of near exclusive use of American Express, she has replaced it with another credit card. While that’s not related to the Costco news, it is something that American Express will likely be experiencing more and more in the coming months. That may, of course, explain the spate of mailings I’ve recently received to entice continuing loyalty.

While that comes at a cost, that’s still tomorrow’s problem and the market has likely discounted the costs of the partnership dissolution, as well as the lost revenues.

I like the price range and I like the option premium and dividend opportunities for as long as they may persist, but my loyalty to shares may only go for a week at a time.

Traditional Stocks: Intel, Microsoft

Momentum Stocks: Seagate Technology

Double-Dip Dividend: American Express (6/30), Cisco (7/1), Oracle (7/6), The Gap (7/6)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.