Who’s wagging who?

Who’s wagging who?

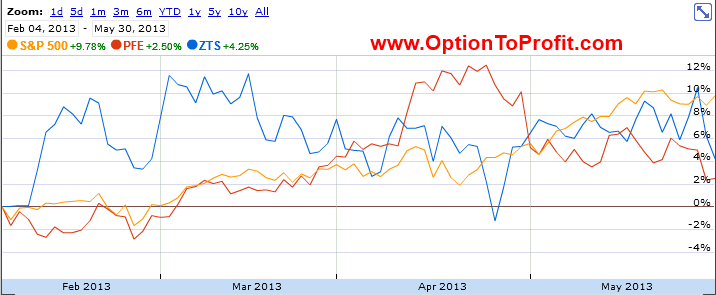

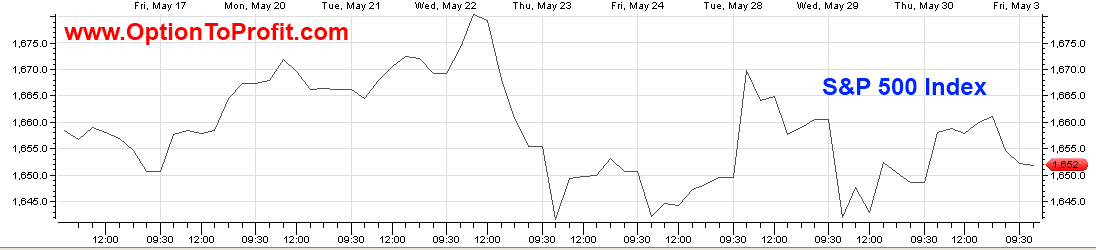

Anytime a major market goes down 7% it has to get your attention, but what seemed to set Japan off? Maybe it was just coincidental that earlier in the day across an ocean, the United States markets had just finished a trading session that was marked by a “Key Reversal,” ostensibly in response to some nuanced wording or interpretation of Federal Reserve Chairman Ben Bernanke’s words in testimony to a congressional committee.

The very next day we showed recovery, but since then it’s been an alternating current of ups and downs, with triple digit moves back in fashion. Intra-day reversals, as in their May 22, 2013 “Key Reversal” extreme have been commonplace in the past week after a long absence

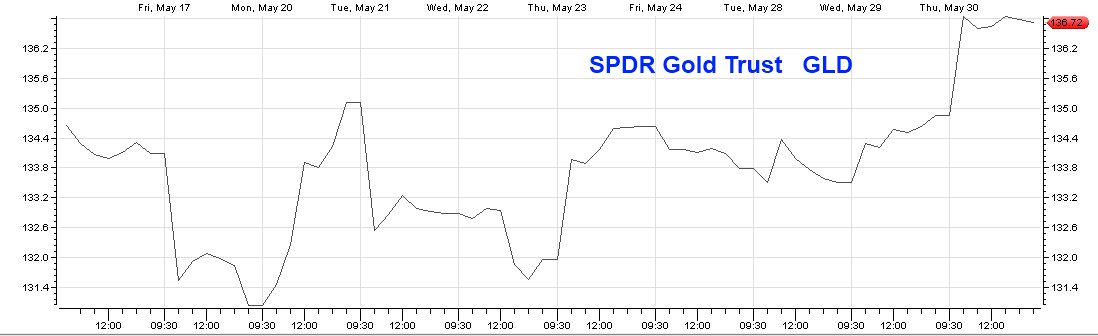

Whether there is any historical correlation, direct or inverse between gold and our markets, gold has been experiencing the same kind of alternating gyrations and actually started really wagging a day before simple words got the better of our markets.

Whether there is any historical correlation, direct or inverse between gold and our markets, gold has been experiencing the same kind of alternating gyrations and actually started really wagging a day before simple words got the better of our markets.

In the meantime, Japan clearly was the last to wag, but buried in the chart is the fact that in the after hours the Nikkei has had significant reversals of the day’s trading and it appears that our own markets have then taken their cues from the Nikkei futures.

In the meantime, Japan clearly was the last to wag, but buried in the chart is the fact that in the after hours the Nikkei has had significant reversals of the day’s trading and it appears that our own markets have then taken their cues from the Nikkei futures.

It may have all started with a daily price fix in London and then it may have been fired up with mere words, but then having gone across the Pacific, it has all come back to our shores with great regularity and indecision.

It may have all started with a daily price fix in London and then it may have been fired up with mere words, but then having gone across the Pacific, it has all come back to our shores with great regularity and indecision.

For me, that is painting an increasing tenuous market and it has shown in individual stocks.

As a covered option seller, I do like alternating moves around a mean. I don’t really care what’s causing a stock to wag back and forth. In fact, doing so is an ideal situation, but more so when the moves aren’t too great and the time frames are short. Certainly the most recent activity has been occurring within short time frames, but the moves may presage something more calamitous or perhaps more fortuitous.

It’s hard to know which and it’s hard to be prepared for both.

Toward those ends I continue to have a sizeable cash position and continue to favor the sale of monthly contracts, but it can’t be all passive, otherwise there’s the risk of letting the world pass you by, so I continue to look for new investing opportunities, although I’ve been executing fewer weekly new positions than it generally takes to make me happy.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details).

I’ve been a fan of Dow Chemical (DOW) for a long time. It’s performance over the past year is a great example of how little a stock’s price has to change in order to derive great profit through the sale of call options and collecting dividends. It is one of those examples of how small, but regular movements round the mean can be a great friend to an investor. While I prefer assignment of my shares over rolling contracts over to the next time period, in this case, Dow Chemical goes ex-dividend at the very beginning of the July 2013 option cycle, thereby adding to the attraction.

I recently sold puts on Intuit (INTU) minutes before earnings were released, having waffled much the way our markets are doing, up until the last minute before the closing bell. Having had two precipitous falls in the weeks before earnings, there wasn’t much bad news left to digest and I was able to buy back puts the following morning, as shares went higher. June isn’t always a kind month to shares of Intuit, but it isn’t consistently a negative period. I think it has still enough stored bad will credit to offer it some stability this June.

Transocean (RIG) is just another of those stocks that’s part of the soap operas created when Carl Icahn puts a company in his cross-hairs. Having just re-initiated the dividend, Transocean has done an incredible job of maintaining value during the period when it ceased dividends and was still subject to lots of liability related to the Deepwater Horizon incident.

There’s nothing terribly exciting about Weyerhauser (WY). I currently own higher priced shares that have withstood the surprisingly low lumber futures thanks to a recent dividend and option premiums. As there is increasing evidence that the economy is growing there’s not too much reason to fear a continued slide in asset value.

Joy Global (JOY) reported earnings last week and I didn’t go along with last week’s suggestion that it would be a good earnings related trade, having also gone ex-divided. Although earnings weren’t stellar, some of the news from Joy Global was and indicated growth ahead, not just for its own operations, but in mining sectors and the economy. Shares seem to have been holding very well at the $55 level

Riverbed Technology (RVBD) is always on my mind for either a purchase or sale of puts in anticipation of a purchase at a lower price. Unfortunately, I don’t always listen to my mind, sometimes forgetting that Riverbed Technology has been a consistent champion of the covered call strategy over a five year period and was highlighted in one of the first articles I wrote for Seeking Alpha, which includes a delightful picture at the end of the article.

Coach (COH) is another of my perennial holdings, however, it was most recently lost to assignment at a substantially lower price, following good earnings. Despite the higher price, it is in the range that I originally initiated purchases and also goes ex-dividend this week. What gives it additional appeal is that now weekly options are available for sale.

Baxter International (BAX) also goes ex-dividend this week and like so many in the health care sector has performed very nicely this year. It recently responded very well to the adverse news related to one of its drugs in the United Kingdom and otherwise has very little putting it a great risk for adverse news. Being currently under-invested in the healthcare sector I’d like to add something to the portfolio and Baxter seems to have low risk at a time that I’m increasingly risk adverse.

Coca Cola Enterprises (CCE) is a stock that I have never owned, despite having considered doing so ever since its IPO, which was more years ago than I care to divulge. It is down approximately 5% from its recent high and appears to have support about $2 lower than its current price. I think that it can withstand any tumult in the overall market with its option premium and dividend offering some degree of comfort in the event of a downturn.

Although, I currently own shares of Williams Companies (WMB) and am uncertain as to whether I will add shares, as I’m over-invested in the energy sector and may favor Transocean to Williams. However, it too, offers a dividend this week and shares seem to be very comfortable at t its current level, which is about 7% lower than its April 2013 high point.

Finally, the lone earnings related trade of the week is Navistar (NAV), now back from the pink sheet dead. Mindful that its last earnings report saw a 50% rise in share price, you can’t completely dismiss a similar move to the downside in the event of a disappointment in earnings or guidance. However, recent reports from Caterpillar (CAT), Cummins Engine (CMI), Joy Global and others suggests that there won’t be horrible news, although you can never predict how the market will react or what other factors may drag an innocent company along for a ride. In Navistar’s case, the weekly futures imply about a 7% move. In the meantime, the sale of a put at a strike price 10% below the current price could provide a 1% ROI. NAy more than that loss and you should be prepared to add Navistar shares to your portfolio and hopefully you’ll enjoy the ride.

Traditional Stocks: Dow Chemical, Intuit, Transocean, Weyerhauser

Momentum Stocks: Joy Global, Riverbed Technology

Double Dip Dividend: Baxter International (ex-div 6/5), Coach (ex-div 6/5), Coca Cola Enterprises (ex-div 6/5), Williams Companies (ex-div 6/5)

Premiums Enhanced by Earnings: Navistar (6/6 AM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.