Schadenfreude suits me just fine.

Schadenfreude suits me just fine.

Is it really “schadefreude” when you don’t really know or see the people upon whom misfortune has been heaped?

For those that aren’t familiar with the word, “schadenfreude” is the strangely good feeling that some people derive when others fail or are subject to misfortune.

In Talmudic teaching the highest form of charity is when neither the donor nor the recipient are aware of one another’s identity. Complete ignorance raises the act of charity to a higher level.

Of course, we will never be able to answer the question of whether there is really a sound produced when a tree falls in the forest and there is no one present to lay witness. A single degree of separation can completely call into question that which seems patently obvious. Ignorance of an event can be is as if it doesn’t even exist.

Being a covered option seller, I do take some perverse pleasure and satisfaction when the market goes lower, even though I know that the vast majority of investors, especially the individual investor, fares well only when the markets are moving higher.

When I sell longer term call options, such as the monthly variety, I just love seeing the share price exceed my strike level early during the term of the contract, only to watch those gains dissipate as the term nears its end, especially if the end returns right to the strike price.

Somewhere, I just know that someone is asking themselves why they didn’t take their profits when they had the chance.

That’s pretty bad, right? But I never see that person. I’m not really certain that they even exist, except for the fact that I was once that person. To a large degree I believe that I was deeply ignorant back in those days with regard to the discipline of securing profits. These days I’ve simply added ignorance to the fortunes of those on the other end of trades to the list of things unknowable. Additionally, not knowing who they are is the highest form of ignorance.

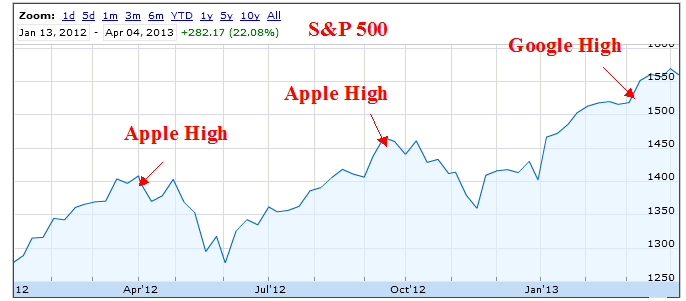

As this past week was one that I immensely enjoyed and briefly put away my short term pessimism in order to trade at levels that reflect a more bullish tone, I’m now on the fence as to whether the bullish feeling can be sustained given what the past may be revealing.

After hitting market peaks 2 weeks ago and then alternatively going from the worst week of 2013 to one of the best weeks of 2013, I continue to believe that we are replicating the first 5 months of 2012.

So while I’m very happy with the higher tract that stocks took this past week, I’m especially happy to see assignments take place and have the cash settle in my account, to hold or to invest, as the market reveals itself.

So while I’m very happy with the higher tract that stocks took this past week, I’m especially happy to see assignments take place and have the cash settle in my account, to hold or to invest, as the market reveals itself.

Although I would much rather be fully invested, I really do want to see give backs of many gains at this point. Having a sizeable portion in cash and evolving from the use of weekly contracts to monthly ones, or even the occasional June 2013 cycle, makes it easy to make that wish.

If history is a guide, the last correction we experienced lasted just one month and then was completely recovered 2 months after it ended.

I can live with that, at least while cash is on the sidelines. If it happens, and assuming that it’s within tolerable levels, such as 10%, I’ll be reasonably happy, but not in a schadenfreude kind of way, although that kind of admission would certainly get me much more attention. Everyone notices the misanthropic guy and wishing that stock prices retreat may be the highest form of misanthrope, especially if it disproportionately impacts widows and orphans.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details). Additionally, as in previous weeks there is a greater emphasis on stocks that offer monthly contracts only, eschewing the usual preference for the relatively higher ROI of weekly options for the guarantee of premiums for a longer period in order to ride out any turbulence. Additionally, as with the previous week, we are at the height of earnings season and thus far there have been some surprises, perhaps offering more opportunity to sell well out of the money puts prior to earnings.

I really can’t recall the last time I owned shares of ExxonMobil (XOM). Although it is one of the shares that I consistently follow, it rarely has piqued my short term interest. That may be changing a bit as I look at its upcoming and increased dividend. At a time that I’m expecting to be on the precipice of a market decline that is technically driven, rather than fundamentally, I would be more inclined to limit new investments to more defensive stocks that are likely to outperform a falling market during a period of economic stability or growth.

Although Apple (AAPL) was a potential earnings related trade last week, I ultimately waited for earnings and instead purchased shares the next day. Those were assigned, but if shares open the week near the $410 level, I am interested in establishing a new position and using an out of the money monthly contract in order to have an opportunity to also secure the newly increased dividend. I believe that Apple will out-perform the market in the near term and will offer trading opportunities in addition to appealing option premiums.

With last week’s selection Cisco (CSCO) among those assigned, Oracle (ORCL) also one of last week’s potential picks went unrequited. It also under-performed Cisco as some of the networking companies were depressed following Broadcom’s (BRCM) earnings. I’ll be looking to Oracle as a potential purchase this week as well, as the technology sector may be showing some signs of catching up to the overall market with Microsoft (MSFT) and Intel (INTC) showing strength.

As news related to the Chinese economy seems to wag our own stock market, the heavy machinery titans have been slammed back and forth as what is called “news” is so often re-interpreted or presented in different lights that create an alternation between good economic news and bad economic news on a near daily basis. Very often the sector moves in unison even when the exposure to China is limited. While Joy Global (JOY) has significant exposure, PACCAR (PCAR)certainly has less so. Both have recovered a bit this past week as have Caterpillar (CAT) and Deere (DE). ALl, however, continue to trail the S&P 500 in 2013.

Petrobras (PBR) suspended its regular dividend payment in 2012. I’m somewhat embarrassed to still be holding shares priced in the $19-20 range, purchased just before a slew of bad news. Having held onto shares even as they sank as much as almost 25%, it has been clawing its way back. Among the positive signs are the recent announcement of two special dividends. With the hope for some stability in its share price after bad news regarding pricing and production issues have now been digested, it may be time to restart accumulating shares.

Last week playing earnings related trades was a very timely strategy. I don’t know if the pleasant surprises will continue, but I think there may again be some very reasonable risk-reward propositions available, as long as you don’t mind the possibility of owning shares after it’s all said and done.

Among those reporting is Facebook (FB), which despite having received an IPO allocation and currently owning shares at various price points, has become one of my favorite stocks. The existence of extended weekly options opens up many more opportunities to generate option premiums and mitigate the potential impact of sudden adverse moves in share price. At Friday’s closing price, a weekly put sale at a strike price 12.5% below the close could return a 0.7% ROI. For those more adventurous, a strike price only 9% lower could yield a 1.4% return.

Pfizer (PFE) reports earnings this week and fits into the profile that appeals to me the most when considering an earnings related trade. This past week it sustained a large price drop, which is usually the signal that clears me to sell puts on shares. However, in this case, I more likely to consider an outright purchase on shares, not only for some capital appreciation and option premium income, but also in order to capture the May 8, 2013 dividend payment.

Humana (HUM) has been on a true rollercoaster ride. As often happens with health care stocks the various interpretations of how changing legislation or pricing structure may impact share price sends the shares in irrational and alternating directions. With earnings approaching and shares down almost 10% from its 2 week ago high, it represents a potentially acceptable risk-reward offer. If it falls less than another7% the ROI is approximately 1%. That, however, is for the time remaining on a monthly contract, which makes it a little less appealing to me, but still under consideration.

Finally, I’m not certain how much longer the world needs an independent Open Table (OPEN) but it has the kind of pricing volatility at the time of earnings release to make it worth considering a purchase of shares and the sale of deep in the money calls or simply a sale of deep out of the money puts.

Traditional Stocks: ExxonMobil, Oracle, Paccar, Pfizer

Momentum Stocks: Apple, Joy Global

Double Dip Dividend: Petrobras (ex-div 4/30)

Premiums Enhanced by Earnings: Facebook (5/1 PM), Humana (5/1 AM), Open Table (5/2 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.