|

Daily Market Update – April 30, 2014 (Close) A bad first quarter GDP and mediocre earnings were the news items to open the morning that would have its crescendo a few hours later when the FOMC announcement was to be made. As it would turn out , that crescendo was pretty muted. While the announcement itself wasn’t too likely to have much in the way of new news it was likely to be interpreted by traders through the lens of this morning’s GDP statistic, with those wondering whether a slowing GDP will be a reason for the Federal Reserve to slow down its tapering, battling with those who believed the GDP number simply reflected awful weather and nothing systemic. Those are usually the battles that are best watched from the sidelines, but since today is a Wednesday that’s already the default position. There has been very little rational basis behind the reactions following these FOMC releases lately, so default isn’t a bad way to go, otherwise you can’t expect anything other than even odds. Instead, the battle itself came to a complete draw as there was barely a peep from anyone, not even much in the way of the usual knee jerk reaction that has become so common and laughable. With new weekly options appearing tomorrow, based on the experience of the past couple of weeks I may again look for opportunity to execute rollovers on Thursday, rather than waiting until Friday. Hopefully today will be a positive kind of day although the pre-open is looking very non-committal, as that’s usually the case in advance of the afternoon announcement. In last week’s case rolling over positions on Thursday was really serendipitous, as it avoided the impact of the market plunge on Friday, that I never would have otherwise expected. No matter how you dissect things, it never hurts to have luck on your side. With lots of positions set to expire this week and a fair number looking as if they are in a position to be assigned, I would love to see that be the case, but not only is the challenge of the FOMC ahead, but also Friday’s Employment Situation Report. I would very much like to see cash reserves increased after a few weeks of drawing down reserves, although this week was one of conservation. Having cash makes it unnecessary to be defensive. While the Employment Situation Report tends to be a positive trading day, last month served as an exception to that rule, as the day snatched defeat from victory, with a mid-day sell-off after a nice opening gain. That might alert people to the possibility that a defensive position may not be altogether ridiculous, given some of the challenged faced this week and the remaining potential for international chaos. In the meantime there continues to be an unraveling of the more speculative corner of the market and any rational person would have to be wondering whether that’s just an early warning signal, as it has been just that in the past. With more earnings yet to go there could easily be Still, you can’t overlook the fact that the market is within striking distance of its all time highs.and as the day was winding to its close all eyes were on the DJIA which was just a few points away from that high point. Again. The market just keeps doing that, despite all of the times that most everyone believed that it was finally ready to take a break. Talk about mixed messages.

|

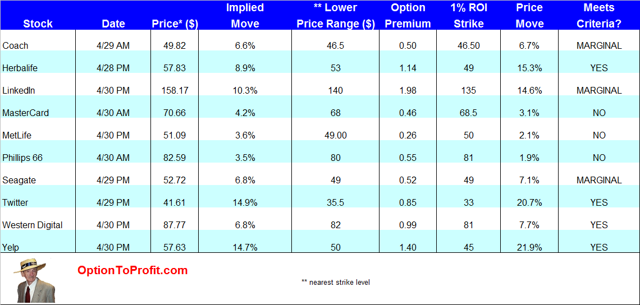

Increasingly for that more speculative portion of my portfolio I look at earnings season as being a great time to generate quick, albeit sometimes nerve wracking, income from those stocks that can be unpredictable in their typical daily trading and even more so when earnings and guidance are at hand.

Increasingly for that more speculative portion of my portfolio I look at earnings season as being a great time to generate quick, albeit sometimes nerve wracking, income from those stocks that can be unpredictable in their typical daily trading and even more so when earnings and guidance are at hand.