Weekend Update – November 24, 2013

I don’t know about other people, but I’m getting a little more nervous than usual watching stocks break the 16000 level on the Dow Jones and the 1800 level on the S&P 500.

What’s next 5000 NASDAQ? Well that’s not so ludicrous. All it would take is 4 years of 6% gains and we would could set the time machine back to a different era.

In hindsight I know what I would do at the 5000 level.

For those old enough to remember the predictions of Dow 35000 all we need is a repeat of the past 56 months and we’re finally there and beyond.

This being a holiday shortened trading week adds a little bit to the stress level, because of the many axioms you hear about the markets. The one that I believe has as much validity as the best of them is that low volume can create artificially large market moves. When so many are instead focusing on the historical strength of markets during the coming week, I prefer to steer clear of any easy guide to riches.

When faced with a higher and higher moving market you could be equally justified in believing that momentum is hard to stop as you could believe that an inflection point is being approached. The one pattern that appears clear of late is that a number of momentum stocks are quickly decelerating when faced with challenges.

When I find myself a little ill at ease with the market’s height, I focus increasingly on “beta,” the measure of a stock’s systemic risk compared to the overall market. I want to steer clear of stock’s that may reasonably be expected to be more volatile during a down market or expectations of a declining market.

As a tool to characterize short term risk beta can be helpful, if only various sources would calculate the value in a consistent fashion. For example, Tesla (TSLA), which many would agree is a “momentum” stock, can be found to have a beta ranging from 0.33 to 1.5. In other words, depending upon your reference source you can walk away believing that either Tesla is 50% more volatile than the market or 67% less volatile.

Your pick.

While “momentum” and “beta” don’t necessarily have correlation, common sense is helpful. Tesla or any other hot stock du jour, despite a reported beta of 0.33, just doesn’t seem to be 67% less volatile than the overall market, regardless of what kind of spin Elon Musk might put on the risk.

During the Thanksgiving holiday week I don’t anticipate opening too many new positions and am focusing on those with low beta and meeting my common sense criteria with regard to risk. Having had many assignments to close out the November 2013 option cycle I decided to spread out my new purchases over successive weeks rather than plow everything back in at one time and risk inadvertently discovering the market’s peak.

Additionally, I’m more likely to look at either expanded option possibilities or monthly options, rather than the weekly variety this week. In part that’s due to the low premiums for the week, but also to concerns about having positions with options expiring this week caught in a possible low volume related downdraft and then being unable to find suitable new option opportunities in future weeks. If my positions aren’t generating revenue they’re not very helpful to me.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

While eschewing risk may be in order when you think a market top is at hand, sometimes risky behavior can be just the thing when it comes to assembling a potentially profitable mix of stocks. In this case the risky behavior comes from the customers of Lorillard (LO), Philip Morris (PM) and Molson-Coors (TAP).

With word that Europeans may finally be understanding the risks associated with tobacco and may be decreasing use of their ubiquitously held cigarettes, Philip Morris shares had a rough week. The 6% drop accompanying what should be good news from a public health perspective brings shares back to a much more inviting level. Shares did successfully test an $85 support level and subsequently bounced back a bit too much for my immediate interest, but I would welcome another move toward that level, particularly as I would prefer an entry cost right near a monthly strike level.

Lorillard, on the other hand, has essentially no European exposure, but perhaps in sympathy gave up just a little bit from its 52 week high after a sustained run higher over the past 6 weeks. While there is certainly downside risk in the event of a lower moving market, shares do go ex-dividend this week and think of all of those people lighting up after a hearty Thanksgiving meal. The near term risk factors identified for Europe aren’t likely to have much of an impact in the United States market, where the only real risk factors may be use of the products.

That Thanksgiving meal may very well be complemented with a product from Molson Coors. I imagine there will also be those using a Molson Coors product while using a Lorillard product, perhaps even dousing one in the other. Shares, which are down nearly 5% from its recent highs go ex-dividend this week. Because of the strike prices available, Molson Coors is one position that I may consider using a November 29, 2013 option contract, as many more strike levels are available, something that is useful when attempting to capture both a decent option premium and the dividend, while also enticing assignment of shares.

Speaking of risky behavior, the one exception to the central theme of staying away from high beta names is the consideration of adding shares of Walter Energy (WLT). While the last 9 months have seen its shares plummet, the last three months have been particularly exciting as shares had gone up by as much as 75%. For those with some need for excitement this is certainly a candidate, with a beta value 170% greater than the average of all other recommended positions this week, the stock is no stranger to movement. But speaking of movement, although I don’t look at charts in any depth, there appears to be a collision in the making as the 50 dma is approaching the 200 dma from below. Technicians believe that is a bullish indicator. Who knows. What I do know is that the coal, steel and iron complex, despite a downgrade this past Friday of the steel sector, has been building a higher base and I believe that the recent pullback in Walter Energy is just a good opportunity for a quick trade, perhaps using the sale of puts rather than covered calls.

While not falling into the category of risky behavior, Intel’s (INTC) price movement this week certainly represents odd behavior. Not being prone to exceptionally large moves of late on Thursday it soared 3%, which by Intel’s standards really is soaring. It then fell nearly 6% the following day. While the fall was really not so odd given that Intel forecast flat revenues and flat operating profits, it was odd that the price had gone up so much the previous day. Buying on Thursday, in what may have been a frenzied battle for shares was a nice example of how to turn a relatively low risk investment into one that has added risk.

But with all of the drama out of the way Intel is now back to a more reasonable price and allows the ability to repurchase shares assigned the previous week at $24 or to just start a new position.

While I would have preferred that Joy Global (JOY) had retreated even further from its recent high, its one year chart is a nearly perfect image of shares that had spent the first 6 months of the year above the current price and the next 6 months below the current price, other than for a brief period in each half year when the relationship was reversed. Joy GLobal is an example of stock have a wide range of beta reported, as well, going from 1.14 to 2.17. However, it has also traded in a relatively narrow range for the past 6 months, albeit currently near the high end of that range.

With earnings scheduled later in the December 2013 option cycle there is an opportunity to attempt to thread a needle and capture the dividend the week before earnings and avoid the added risk. However, I think that Joy Global’s business, which is more heavily reliant on the Chinese economy may return to its recent highs as earnings are delivered.

Lowes (LOW) reported earnings this past week, and like every previous quarter since the dawn of time the Home Depot (HD) versus Lowes debate was in full force and for yet another quarter Lowes demonstrated itself to be somewhat less capable in the profit department. However, after its quick return to pricing reality, Lowes is once again an appealing portfolio addition. I generally prefer considering adding shares prior to the ex-dividend date, but the share price slide is equally compelling.

Hewlett Packard (HPQ) is one of those stragglers that has yet to report earnings, but does so this week. Had I known 35 years ago that a classmate would end up marrying its future CEO, I would likely not have joined in on the jokes. It is also one of those companies that I swore that I would never own again as it was one of my 2012 tax loss positions. I tend to hold grudges, but may be willing to consider selling puts prior to earnings, although the strike price delivering a 1% ROI, which is my typical threshold, is barely outside of the implied price move range of 8%. It’s not entirely clear to me where Hewlett Packard’s future path may lead, but with a time perspective of just a week, I’m not overly concerned about the future of the personal computer, even if Intel’s forecasts have ramifications for the entire industry.

Lexmark (LXK) is a company that I like to consider owning when there is also an opportunity to capture a dividend. That happens to be the case this week. When it announced that it was getting out of the printer business investors reacted much as you would have imagined. They dumped shares, which for most people are electronically maintained and not in printed form. After all, why own a printer company that says that printers are a dead end business? Who knew that Lexmark had other things in mind, as it has done quite nicely focusing on business process and content management solutions. While it has been prone to large earnings related moves or when shocking the investment community with such news as it was abandoning its most recognizable line of business, it has also been a rewarding position, owing to dividends and option premiums. However, always attendant is the possibility of a large news related move that may require some patience in awaiting recovery.

Finally, I find myself thinking about adding shares of eBay (EBAY) again this week, just as last week and 10 other times this past year. Perhaps I’m just obsessed with another CEO related missed opportunity. Shares didn’t fare too well based upon an analyst’s report that downgraded the company saying that shares were “range bound at $49-$54.” While that may have been the equivalent of a death siren, for me that was just validation of what had been behind the decision to purchase and repurchase shares of eBay on a regular basis. While being range bound is an anathema to most stock investors, it is a dream come true to a covered option writer.

Happy Thanksgiving.

Traditional Stocks: eBay, Intel, Lowes, Philip Morris

Momentum Stocks: Joy Global, Walter Energy

Double Dip Dividend: Lexmark (ex-div 11/26), Lorillard (ex-div 11/26), Molson-Coors (ex-div 11/26)

Premiums Enhanced by Earnings: Hewlett Packard (11/26 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – November 17, 2013

Things aren’t always as they seem.

Things aren’t always as they seem.

As I listened to Janet Yellen face her Senate inquisitors as the hearing process began for her nomination as our next Federal Reserve Chairman, the inquisitors themselves were reserved. In fact they were completely unrecognizable as they demonstrated behavior that could be described as courteous, demur and respectful. They didn’t act like the partisan megalomaniacs they usually are when the cameras are rolling and sound bites are beckoning.

That can’t last. Genteel or not, we all know that the reality is very different. At some point the true colors bleed through and reality has to take precedence.

Closing my eyes I thought it was Woody Allen’s sister answering softball economic questions. Opening my eyes I thought I was having a flashback to a curiously popular situational comedy from the 1990s, “Suddenly Susan,” co-starring a Janet Yellen look-alike, known as “Nana.” No one could possibly sling arrows at Nana.

These days we seem to go back and forth between trying to decide whether good news is bad news and bad news is good news. Little seems to be interpreted in a consistent fashion or as it really is and as a result reactions aren’t very predictable.

Without much in the way of meaningful news during the course of the week it was easy to draw a conclusion that the genteel hearings and their content was associated with the market’s move to the upside. In this case the news was that the economy wasn’t yet ready to stand on its own without Treasury infusions and that was good for the markets. Bad news, or what would normally be considered bad news was still being considered as good news until some arbitrary point that it is decided that things should return to being as they really seem, or perhaps the other way around..

While there’s no reason to believe that Janet Yellen will do anything other than to follow the accommodative actions of the Federal Reserve led by Ben Bernanke, political appointments and nominations have a long history of holding surprises and didn’t always result in the kind of comfortable predictability envisioned. As it would turn out even Woody Allen wasn’t always what he had seemed to be.

Certainly investing is like that and very little can be taken for granted. With two days left to go until the end of the just ended monthly option cycle and having a very large number of positions poised for assignment or rollover, I had learned the hard way in recent months that you can’t count on anything. In those recent cases it was the release of FOMC minutes two days before monthly expiration that precipitated market slides that snatched assignments away. Everything seemed to be just fine and then it wasn’t suddenly so.

As the markets continue to make new closing highs there is division over whether what we are seeing is real or can be sustained. I’m tired of having been wrong for so long and wonder where I would be had I not grown cash reserves over the past 6 months in the belief that the rising market wasn’t what it really seemed to be.

What gives me comfort is knowing that I would rather be wondering that than wondering why I didn’t have cash in hand to grab the goodies when reality finally came along.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

Sometimes the most appealing purchases are the very stocks that you already own or recently owned. Since I almost exclusively employ a covered option strategy I see lots of rotation of stocks in and out of my portfolio. That’s especially true at the end of a monthly option cycle, particularly if ending in a flourish of rising prices, as was the case this week.

Among shares assigned this past week were Dow Chemical (DOW), International Paper (IP), eBay (EBAY) and Seagate Technology (STX).

eBay just continues to be a model of price mediocrity. It seems stuck in a range but seems to hold out enough of a promise of breaking out of that range that its option premiums continue to be healthy. At a time when good premiums are increasingly difficult to attain because of historically low volatility, eBay has consistently been able to deliver a 1% ROI for its near the money weekly options. I don’t mind wallowing in its mediocrity, I just wonder why Carl Icahn hasn’t placed this one on his radar screen.

International Paper is well down from its recent highs and I’ve now owned and lost it to assignment three times in the past month. While that may seem an inefficient way to own a stock, it has also been a good example of how the sum of the parts can be greater than the whole when tallying the profits that can arise from punctuated ownership versus buy and hold. Having comfortably under-performed the broad market in 2013 it doesn’t appear to have froth built into its current price

Although Dow Chemical is getting near the high end of the range that I would like to own shares it continues to solidify its base at these levels. What gives me some comfort in considering adding shares at this level is that Dow Chemical has still under-performed the S&P 500 YTD and may be more likely to withstand any market downturn, especially when buoyed by dividends, option premiums and some patience, if required.

Unitedhealth Group (UNH) is in a good position as it’s on both sides of the health care equation. Besides being the single largest health care carrier in the United States, its purchase of Quality Software Services last year now sees the company charged with the responsibility of overhauling and repairing the beleague

red Affordable Care Act’s web site. That’s convenient, because it was also chosen to help set up the web site. It too, is below its recent highs and has been slowly working its way back to that level. Any good news regarding ACA, either programmatically or related to the enrollment process, should translate into good news for Unitedhealth

Seagate Technology simply goes up and down. That’s a perfect recipe for a successful covered option holding. It’s moves, in both directions, can however, be disconcerting and is best suited for the speculative portion of a portfolio. While not too far below its high thanks to a 2% drop on Friday, it does have reasonable support levels and the more conservative approach may be through the sale of out of the money put options.

While I always feel a little glow whenever I’m able to repurchase shares after assignment at a lower price, sometimes it can feel right even at a higher price. That’s the case with Microsoft (MSFT). Unlike many late to the party who had for years disparaged Microsoft, I enjoyed it trading with the same mediocrity as eBay. But even better than eBay, Microsoft offered an increasingly attractive dividend. Shares go ex-dividend this week and I’d like to consider adding shares after a moth’s absence and having missed some of the run higher. With all of the talk of Alan Mullally taking over the reins, there is bound to be some let down in price when the news is finally announced, but I think the near term price future for shares is relatively secure and I look forward to having Microsoft serve as a portfolio annuity drawing on its dividends and option premiums.

I’m always a little reluctant to recommend a possible trade in Cliffs Natural Resources (CLF). Actually, not always, only since the trades that still have me sitting on much more expensive shares purchased just prior to the dividend cut. Although in the interim I’ve made trades to offset those paper losses, thanks to attractive option premiums reflecting the risk, I believe that the recent sustained increase in this sector is for real and will continue. Despite that, I still wavered about considering the trade again this week, but the dividend pushed me over. Although a fraction of what it had been earlier in the year it still has some allure and increasing iron ore prices may be just the boost needed for a dividend boost which would likely result in a significant rise in shares. I’m not counting on it quite yet, but think that may be a possibility in time for the February 2014 dividend.

While earnings season is winding down there are some potentially interesting trades to consider for those with a little bit of a daring aspect to their investing.

Not too long ago Best Buy (BBY) was derided as simply being Amazon’s (AMZN) showroom and was cited as heralding the death of “brick and mortar.” But, things really aren’t always as they seem, as Best Buy has certainly implemented strategic shifts and has seen its share price surge from its lows under previous management. As with most earnings related trades that I consider undertaking, I’m most likely if earnings are preceded by shares declining in price. Selling puts into price weakness adds to the premium while some of the steam of an earnings related decline may be dissipated by the selling before the actual release.

salesforce.com (CRM) has been a consistent money maker for investors and is at new highs. It is also a company that many like to refer to as a house of cards, yet another way of saying that “things aren’t always as they seem.” As earnings are announced this week there is certainly plenty of room for a fall, even in the face of good news. With a nearly 9% implied volatility, a 1.1% ROI can be attained if less than a 10% price drop occurs, based on Friday’s closing prices through the sale of out of the money put contracts.

Then of course, there’s JC Penney (JCP). What can possibly be added to its story, other than the intrigue that accompanies it relating to the smart money names having taken large positions of late. While the presence of “smart money” isn’t a guarantee of success, it does get people’s attention and JC Penney shares have fared well in the past week in advance of earnings. The real caveat is that the presence of smart money may not be what it seems. With an implied move of 11% the sale of put options has the potential to deliver an ROI of 1.3% even if shares fall nearly 17%.

Finally, even as a one time New York City resident, I don’t fully understand the relationship between its residents and the family that controls Cablevision (CVC), never having used their services. As an occasional share holder, however, I do understand the nature of the feelings that many shareholders have against the Dolan family and the feelings that the publicly traded company has served as a personal fiefdom and that share holders have often been thrown onto the moat in an opportunity to suck assets out for personal gain.

I may be understating some of those feelings, but I harbor none of those, personally. In fact, I learned long ago, thanks to the predominantly short term ownership afforded through the use of covered options, that it should never be personal. It should be about making profits. Cablevision goes ex-dividend this week and is well off of its recent highs. Dividends, option premiums and some upside potential are enough to make even the most hardened of investors get over any personal grudges.

Traditional Stocks: Dow Chemical, eBay, International Paper, Unitedhealth Group

Momentum Stocks: Seagate Technology

Double Dip Dividend: Cablevision (ex-div 11/20), Cliffs Natural (ex-div 11/20), Microsoft (ex-div 11/19)

Premiums Enhanced by Earnings: Best Buy (11/19 AM), salesforce.com (11/18 PM), JC Penney (11/20 AM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Cisco was a Friend of Mine

You have to be of a certain age to recognize the Cisco Kid character, but somewhat younger to be familiar with the song that paid homage to the fictional character.

You have to be of a certain age to recognize the Cisco Kid character, but somewhat younger to be familiar with the song that paid homage to the fictional character.

After terrible earnings and poorly received guidance that stunned most everyone, Cisco (CSCO) hasn’t made many friends, but it’s still a friend of mine.

Maybe the problem is all in the name. No, not Cisco, there are worse things in the world than being confused for a food services company. Maybe the problem is in the name John Chambers.

Barely two years ago it was a John Chambers, as head of Standard and Poors’ Sovereign Debt Committee who lowered the debt rating of US Treasury debt. He wasn’t very popular at the time, as many people are put off when they can connect the dots and point fingers at the catalyst for a market wide plunge.

But the John Chambers who is the CEO of Cisco has seen his popularity mirror that of many stocks, in general, as it has gone up and down and up again.

Now it’s down.

Not too long ago John Chambers was said to be on the short list to be the Treasury Secretary in the Bush administration. He was regarded as a model CEO of the new economy and his slow drawl and transparency were welcome alternatives to the obfuscation spun by so many others. His candor during interviews in the immediate moments of earnings being released were always respected.

Then the bottom fell out from Cisco and there were calls for his ouster. Seeing share price in 2011 challenge the lows of 2009 wasn’t the sort of thing that engendered confidence and the calls went out for his head. At that point Treasury Secretary may have been looking pretty good, but that ship had long sailed.

But Chambers was eventually rehabilitated. Rising stock prices, perhaps buoyed by aggressive buybacks, will do that for you. In fact, if you conveniently have data points extend only from the lows in August 2011 to yesterday, Cisco actually out-performed the broader index.

Ironically, John Chambers is somewhat like fictional The Cisco Kid, who actually started his life as a cruel outlaw, but became regarded as being a heroic character. It’s just that Chambers can stay a hero.

Chambers has been there and done that, but now he’s back in that dark place, where people are even poking fun at his drawl and once again saying that his ship has sailed. Perhaps plunges on two successive earnings releases will create that kind of feeling. He certainly may have cut back a bit on his candor, as even his appearance yesterday offered little insight into the disappointment that awaited.

In fact, many asked, given how substantive the alterations in forward guidance were, why Cisco didn’t pre-announce or issue revised guidance weeks ago.

Personally, I don’t see the difference between getting hit with an earnings related surprise earlier, rather than when scheduled. I actually prefer knowing the date and time that i may see my shares subject to evisceration.

I owned Cisco shares and have done so on 5 different occasions this year. My shares had calls written upon them and were due to expire November 22, 2013. Barely a few hours ago they seemed certain to be assigned. Now they are more likely to be seeking rollover opportunity to a future date.

As most everyone has piled on the sell wagon, much as had occurred with Oracle (ORCL), which also had two successive share plunges after disappointing earnings, I believe that for the short term trader and particularly for the covered option trader, this most recent fall in share price is just an entry opportunity.

Yesterday, I did something that I very rarely do. I purchased shares in the after hours. Usually when I do so, in the anticipation that by morning calmer heads will prevail, I’m typically wrong. That was the case with Cisco this morning.

In addition to buying shares in the after hours, another thing that I rarely do is to purchase shares without immediately or very shortly after selling calls on those shares. In essence, both actions were counter to my overall desire to limit risk.

While I’m usually on the wrong side of momentum when entering, I look at these positions as ones to generate both capital gains from shares and option premium income, whereas for the majority of my positions I emphasize premium and dividend income.

In the case with Oracle, opportunity existed after bad news and exaggerated downward price movements. SInce I tend to be short term oriented, I only care about the opportunity and not about structural issues that may have longer term impact.

While earnings represented a risk and shares moved quite a bit more than the implied movement, suggesting that investors were surprised and unprepared, I think the risk is now greatly discounted.

I make no judgment regarding the ability of Cisco, whether under Chambers’ leadership or anyone else to compete in the marketplace and to recapture its glory or restore Chambers to a position of honor.

Instead, Cisco is nothing more than a vehicle. The Cisco Kid had his horse, John Chambers had his buybacks and for some the shares of this beleaguered company are the vehicle of the day.

Weekend Update – November 10, 2013

Is there life after momentum slows?

Is there life after momentum slows?

There was no shortage of stocks taking large price hits last week, as earnings season had already begun its slowdown phase. However, for some of the better known momentum stocks the slightest mis-steps were all the reason necessary to flee with profits.

For those who live long enough, it should never come as a surprise that some things are just destined to slow down.

Momentum fits into that category, although based on the past week it’s more of a question of falling down than slowing down for some.

After the fact, no one seemed to be surprised.

In a week that saw a decrease in the ECB’s main lending rate that was widely described as being a “surprise'” later in the day came reports that most economists expected the cut. The market clearly didn’t, however, as the economists may have neglected to pass on their views.

And then there was a surprisingly large increase in non-farm payroll jobs. Somehow everyone was taken off guard and the market responded by interpreting good news as good news and finished the week with a flourish.

What surprised me, however, was that there was such a disconnect between the anticipated numbers and the actual report, which covered the period of the government shutdown. The disconnect had to do with methodology, as forecasts didn’t take into account that government statistics considered furloughed employees to be employed, since they were to receive back, through legislative action.

Oops.

In effect, Friday’s rally was based on a misunderstanding of methodology. It will also certainly be interesting to see what impact Ben Bernanke’s statement after the market’s close may have on Monday’s trading.

I think the unemployment rate probably understates the degree of slack in the labor market. I think the employment-population ratio overstates it somewhat, because there are important downward trends in participation

Unfortunately, Friday’s gains complicate the goal of finding bargain priced stocks in the coming week, but with a little water having been thrown on the fire there may be opportunity yet.

Everyone, including me, likes to look for clues and cues that have predictive value. Parallels are drawn at every opportunity to what we know from the past in the expectation that it can foretell the future.

For some the sudden increase in IPOs coming to market and the sudden fall of many momentum stocks heralds a market top. In hindsight, if it does occur, it will be regarded as “no surprise.” If it doesn’t occur within the attention span of most paying attention it will simply be conveniently ignored.

For others the reversal of fortune may represent values and not value traps.

But no matter what the case there is life after momentum slows. It’s just a question of accommodation to new circumstances.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

eBay (EBAY) like so many stocks that I consider tends to trade in a range. While eBay is often criticized for being “range bound” there is some comfort in knowing that it is less likely to offer an unwanted surprise than many other stocks. My shares were assigned this past week and are now trading at the upper range of where I may normally initiate a position. However, having owned shares on ten separate occasions this year I would be anxious to do so again on the slightest of pullbacks.

Although hardly a momentum stock, Mondelez (MDLZ) had some earnings woes this past week, although it did recover a bit, perhaps simply being carried along by a rallying market. Shares are still a little higher than I would like for an entry point, but I expect that as a short term selection it will match market performance, while in a market turn-down it will exceed performance.

Fastenal (FAST) is another fairly sedate company, yet its stock often has some large moves. I see Fastenal as a leading indicator of economic activity, but also very sensitive to the economy. I think its most recent price weakness will be reversed as the impact of a resolution of the government’s shutdown trickles down to the economy. I currently own shares with a contract set to expire this week, but at this price am considering doubling down on what in essence can be a weekly option contract during the final week of the November 2013 cycle.

Deere (DE) is another range bound stock, that in hindsight I should have bought on numerous occasions over the past few months. Good option premiums, a good dividend and not facing some of the same external pressures as another favorite, Caterpillar (CAT), makes Deere a perennially good selection within its sector.

I currently ow

n shares of both Eli Lilly (LLY) and International Paper (IP), both of which go ex-dividend this week. Unlike many other stocks that I discuss, I have not owned either on multiple occasions this year and my current shares are now below their cost. Both emerged unscathed after recent earnings reports, although both are down considerably from their recent highs and both have considerably under-performed the S&P 500 from the time for its first in a series of market highs on May 21, 2013. That latter criterion is one that I have been using with some regularity as the market has continued to reach new highs in an effort to identify potential late comers to the party.

Which finally brings me to the momentum stocks that have my attention this week, some of which may be best approached through the sale of put options and may be best avoided in a weakening market.

Much has been said of the “ATM effect” on Facebook (FB), as speculation that investors were selling Facebook shares to raise money to buy Twitter (TWTR) shares. Following an abrupt reversal during its conference call when there was a suggestion that adolescents were reducing their Facebook use shares have just not regained their traction. Sometimes it’s just profit taking and not driven by the allure of a newer stock in town. But assuming that the “ATM effect” has some validity and with a large gap between the Twitter IPO price and its 7% lower price on its first full day of trading, I can’t imagine now taking the opportunity to sell Facebook in order to purchase Twitter shares. On its own merits Facebook may be a momentum stock that has a cushion of protection until its next earnings report, unless an errant comment gets in the way, again.

Chesapeake Energy (CHK) is much higher than the level at which I last owned shares at $21. Waiting for a return has been fruitless and as a result, rather than having owned shares on 15 occasions, as in 2012, thus far, I’ve only had five bouts of ownership. With the melodrama surrounding its founder and ex-CEO in its past, Chesapeake may begin trading a bit more on fundamentals rather than hopes for a return to its glory days. at such, its price action may be less unidirectional than it has been over the past four months. After last week’s earnings report related drop, while still higher than I would like, I think there may be reason to consider a new entry, perhaps through the sale of put options.

Freeport McMoRan (FCX) is a stock that has been testing my patience through the year. More precisely, however, I’ve had no real issue with Freeport McMoRan’s leadership, in fact, given metal prices, it has done quite well. What I don’t understand is how it has been taking so long for markets to appreciate its strategic initiatives and long term strategies. For much of the year my shares have been non-performing, other than for dividend payments, but with a recent run higher some are generating option premium income streams. Despite the run higher, I am considering adding more shares as the entire metals complex has been showing strength and some stability, as well.

Finally, while I’ve said before that I don’t spend too much time looking at charts, a recent experience with Tesla (TSLA) was perhaps a good reason to at least acknowledge that charts can allow you to look at the past.

While it’s probably always a good week to be Elon Musk, relatively speaking last week wasn’t so good, as both Tesla and Solar City (SCTY) were treated harshly after earnings were released. The spin put around another reported car fire that its resultant heat could be garnered to power several mud huts didn’t give shares much of a boost, perhaps because that might have cannibalized SolarCity sales, with the two companies likely having much overlap in ownership.

Tesla reported earnings last week and took a drubbing through successive days.

A reader of last week’s article asked:

“George, what are your thoughts on a sale of Puts on TSLA which reports Tuesday?”

My response was:

“TSLA isn’t one that I follow, other than watching in awe.

But purely on a glance at this week’s option pricing the implied volatility is about 12% and you can get a 1% ROI on a strike that’s about 17% lower, currently $135

It looks as if it may have price support in the $134-$139 range, but it’s hard to know, because its ascent has been so steep that there may not be much of a real resting point.

In a very speculative portion of my portfolio I might be able to find some money to justify that trade.”

As it turned out Tesla closed the week at $137.95 and now has my attention. You do have to give some credit to its chart on that one. WIth disappointment over its sales, supply chain issues and reports of car fires and even Elan Musk suggesting that “Tesla’s stock price is more than we have any right to deserve,” it has fallen by nearly 21% from the time of that comment, barely 2 weeks prior to earnings. Although to be entirely fair shares did fully recover from a 7.5% decline in the aftermath of the statement in advance of earnings.

While still not knowing where the next resting point may be in the $119-$122 range, representing as much as another 13% price drop. With earnings out of the way to

enhance option premiums the risk-reward proposition isn’t as skewed toward reward. However, for those looking to recapture of bit of their own momentum, despite the realization that the end may be near, a put sale can return an ROI of approximately 1.4% at a strike price nearly 6% below Friday’s close is not breached.

The nice thing about momentum slowing is that if you fall the floor isn’t as far away as it used to be.

Traditional Stocks: Deere, eBay, Fastenal, Mondelez

Momentum Stocks: Chesapeake Energy, Facebook, Freeport McMoRan, Tesla

Double Dip Dividend: Eli Lilly (ex-div 11/13), International Paper (ex-div 11/13)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Disclosure: I am long CAT, CHK, DE, FAST, FCX, IP, LLY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

A Put Primer

There was a lot of stress this week over the sale of puts on Abercrombie and Fitch.

There was a lot of stress this week over the sale of puts on Abercrombie and Fitch.

Most of the stress was by me. Not because of the ridiculous price action, which is standard fare for these shares, but because I had to figure out how best to track the outcome of the trade when some people. including me had early assignment of the puts, while others did not and were heading toward assignment at the end of the day.

That also means different trading strategies because some would potentially have shares in hand upon which to sell calls today, while others would be faced with the decision to either roll over the puts or await assignment and hope to be able to sell calls on Monday.

The problem with that latter is that it’s hard to predicate anything on a hope, especially since today was an ideal day to rollover the puts as ANF had a large share gain intra-day. Who knows what Monday brings?

My guess, but that’s all it can ever be is that if the market is sound next week ANF will make up some more ground in advance of its earnings report on November 21, 2013.

Between the known fact that shares were stronger today and the unknowns awaiting next week, compounded by what ridiculous more news may come at earnings makes the gift horse especially appealing.

Later I’ll show you why improving price was important using some screenshots I took during the day while following shares looking for opportiunities.

But since this is a primer, let’s start at the beginning.

To start, a put is an option contract that when bought is a statement that the buyer expects the shares to go down in value, in which case the value of his option will increase.

The buyer typically wants to trade in and out of option positions, because their money is greatly leveraged. They don’t usually want to be assigned and have to take over ownership of shares.

The put seller is usually the more bullish participant in the trade. They think that the shares may go up or down, but if they go down they’re not likely to go below the strike price. The big caveat is that put sellers should be willing to own the shares just in case they are assigned and they end up owning them, as happened to me and a small number of other subscribers.

In the case of Abercrombie and Fitch its shares plummeted on the day before their planned Analysts’s Meeting, the first they had held in over two years.

On the evening before that meeting they presented revised guidance and it wasn’t very good news. I hate revised guidance, even when it’s good. There’s no way to prepare for it unless you have inside information.

I almost purchased shares in the after-hours, but decided to wait until the next day.

At first, when trading started I was upset for having waited as the price significantly improved but was still low enough to seem to warrant a position. However, just to hedge, I decided to use an out of the money put in anticipation of some continued price drop.

As an aside, but an appropriate one, I think the current market may be an appropriate one for the use of more put sales rather than initiating new positions and covered calls. That’s simply an expression of a bearish sentiment. Even though I’ve been cautious and have kept cash reserves, I’ve not used the SOS strategy as a further expression of bearishness, but I think there may be a greater role for put sales now.

Obviously, understanding them is requisite for their use.

But, back to Abercrombie and Fitch. Thanks to the utterings of the CEO, who is not terribly regarded as a person, due to his rather odd behavior and opinions, shares suddenly went much lower during mid-day trading and then everyone on television just piled on. If you ever have any doubt about the power of basic cable television, just watch the ticker and price changes as specific stocks are discussed, especially when event driven. But even then, the continued drop surprised me, thinking that an additional 2% drop was enough of a cushion after an already 5% drop in shares.

So shares dropped even more. Normally, the escape strategy when having sold puts that are now in the money is to simply roll them over at the same strike price, assuming you continue to be reasonably bullish. Otherwise, you can roll down to a lower strike price, but that will cut into your net premium, perhaps even causing a “net debit” from the transaction.

However, Abercrombie and Fitch made any kind of transaction difficult because the more it was in the money the less became the time value of the contracts, being instead made up almost entirely of intrinsic value, that is the difference between the strike and the current value. To make it worse, there was a large gap between the bid and ask prices.

The net result was that at one point earlier in the day a rollover trade would have resulted in incurring a Net Debit.

The net result was that at one point earlier in the day a rollover trade would have resulted in incurring a Net Debit.

You don’t want a net debit. You would prefer to make money, even if it’s not that much money.

In this scenario you would have still been obligated to buy shares for $35.50 a week later, but it would have cost you $0.20 of your earlier option premium profit.

As long time subscribers know, I have patience.

In this case the patience was measured in hours and not option cycles.

In the meantime, though the price of shares started recovering in the late morning, the Net Debit went only to break-even.

In the meantime, though the price of shares started recovering in the late morning, the Net Debit went only to break-even.

The differential between the expiring contract and that of the next week saw naturally more erosion in the expiring contract as price moved in a direction toward the strike price. Obviously, that’s not something in your control. It’s just a measured risk, knowing that even if nothing is done you’ll end up with shares in your account on Monday morning and then just do with them as is done with every other holding.

But simply being at break-even is fine if the brokerage is your uncle. Otherwise, it’s not very satisfying.

Then it went to a Net Credit.

Then it went to a Net Credit.

Bingo.

That’s what you want. In fact, you can see from the timestamp on this image and the previous one, that even though the price of shares was more favorable earlier, the premium differential actually improved as the clock was ticking, even though shares moved away from the strike.

The problem was that the bid-ask spread was still on the large side, leaving only a small net profit

The problem was that the bid-ask spread was still on the large side, leaving only a small net profit

Here’s where it’s helpful to look at the call side of things.

Even though pricing isn’t always rational, it’s reasonable to expect that whatever irrationality there is would be equally distributed between call buyers and put buyers.

Hard to prove, but equally hard to argue.

On the call side of things the equivalent trade, that is selling the November 16, 2013 $35.50 call was yielding a bid of $0.18 with a more normal differential between bid and ask.

So in placing a trade to rollover the puts, rather than using the bid on the sale and the ask on the purchase (as outlined here), for a Net Credit of $0.08, use an intermediate figure determined on the call side of the aisle.

For those that haven’t owned Abercrombie and Fitch in the past, it is a stock that can be very rewarding with a modicum of patience and has been ideally suited for a covered option strategy, but all in all I would much rather see put sales expire and simply decide whether I want to pursue the stock on my own terms the following week, as was recently done with Coach, another company that takes big price hits, but always seems to work its way back into good graces.

In general, if your put sale shares are just slightly in the money you are usually much better off simply rolling over the puts just as you would normally rollover a call position sold on shares that you own.

Unfortunately, I don’t have it documented with screenshots, but for my personal trades some of you may have noticed that I’ve been doing that with the ProShares Ultra Silver ETN (AGQ) speculative hedging position. In this case using a $20 strike price I haven’t really cared too much whether the price was above or below the strike. I just allowed events to dictate whether rolling over when expecting a price increase in silver or sitting on the sidelines when expecting price increases. As with stocks, it’s all about being able to do the trades on a serial basis and watching the premiums add up.

When history repeats itself it can be a beautiful thing.

If this is your first foray with Abercrombie and Fitch I believe that this is a good price at which to do it over and over again, whether through the sale of puts of through the use of covered calls.

I’ll leave the personal feelings about the CEO to others, as long as there is a way to milk some dividends from this pig.

Weekend Update – November 3, 2013

Some things are just unappreciated until they’re gone.

Some things are just unappreciated until they’re gone.

If you can remember those heady days of 2007, it seemed as if every day we were hitting new market highs and everyone was talking about it when not busy flipping houses.

Some will make the case that is the perfect example of a bubble about to burst, similar to when a bar of gold bullion appears on the cover of TIME magazine, just in time to mark the end of a bull run.

On the other hand, when everyone is suddenly talking about perhaps currently being in a bubble it may be a good time to plan for even more of a good thing.

That’s emblematic of the confusion swirling in our current markets. Earnings are up. Better than expected by most counts, yet revenues are down. The stock market can do only one thing and so it goes higher.

In case you haven’t been paying attention, 2013 has been a year of hitting record after record. Yet the buzz is absent, although house flipping is back. Not that I go to many social events but not many are talking about how wild the market has been. That’s markedly different from 2007.

Listening to those who purport to know about human behavior and markets, that means that we are not yet in a stock market bubble and as such, the market will only go higher, yet that’s at odds with the rampant bubble speculation that is being promoted in some media.

I’m a little more cynical. I see the paucity of excitement as being reflective of investors who have come to believe that consistently higher markets are an entitlement and have subsequently lost their true value. No one seems to appreciate a new record setting close, anymore. The belief in the right to a growing portfolio is no different from the right to use a calculator on an exam. Along with that right comes the loss of ability and appreciation of that ability.

Without spellchecker, the editors at Seeking Alpha would have a hard time distinguishing me from a third grader, but spelling really isn’t something I need to due. It’s just done for me.

While many were unprepared in 2007 because they were caught up in a bubble, 2013 may be different. In 2007 the feeling was that it could only get better and better, so why exercise caution? But in 2013 the feeling may be that there is nothing unusual going on, so what is there to be cautious about?

AS markets do head higher those heights are increasingly met with ennui instead of wonder and awe. It’s barely been more than five years since we last felt the wrath of an over-extended market but I’m certain that the new daily records will be missed once they’re gone.

As a normally cautious person when it comes to investing, but not terribly willing to sacrifice returns for caution my outlook changes with frequency as new funds find their way into my account after the previous week’s assignment of options I had sold.

This past week I didn’t have as many assignments as I had expected owing to some late price drops on Friday, so I’m not as likely to go on a spending spree this coming week, as I don’t want to dig deeply into my cash reserve. This week I’m inclined to think more in terms of dividend paying stocks and relatively few higher beta names, although opportunity is situational and Monday morning’s opening bell may bring surprise action. I appreciate surprise and for the record, I appreciate every single bit of share appreciation and income that comes my way as a gift from this market.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

I currently own shares of MetLife (MET) and have done so several times this year. MetLife reported earnings this past week. They reported a nearly $2 billion turnaround in profits, but missed estimates, despite strength in every metric. They re-affirmed that a lower interest rate environment, as might be expected with a continuation of Quantitative Easing, could impact its assets’ performance in the coming year. That was the same news that created a buying opportunity in the previous quarter, so it should not have come as too much of a surprise. What did, however come as a surprise was the announcement that MetLife would no longer be offering earnings per share guidance. According to its CEO “we will instead expand our discussion of key financial metrics and business drivers, creating a more informed view of MetLife’s future prospects.” The price drop and it’s ex-dividend date this week make it a likely candidate for using my limited funds this week.

I’ve long believed that Robert ben Mosche, CEO of AIG (AIG) was something of a saint. Coming out of comfortable retirement in Croatia to attempt an AIG rescue, he continued on his quest even while battling cancer and still found the time to re-pay AIG’s very sizeable debt to US taxpayers. Who needs that sort of thing when you can live like royalty off the Mediterranean coast?

AIG was punished after reporting earnings this past week. It’s hard to say whether the in line earnings, but slightly lower revenue was to blame for the nearly 7% drop or whether joining forces with MetLife was to blame. Not that they literally joined forces, it’s just that ben Mosche announced that AIG will no longer comment on its “aspirational goals,” which was a way of saying that they too were no longer going to provide guidance. I haven’t owned shares in 2 months and that was at a lower price point than even after the large Friday drop, but I think the opportunity has re-arrived.

Wells Fargo (WFC) goes ex-dividend this week and as much as I’ve silently prayed for its share price to drop back to levels that I last owned them, it just hasn’t worked out that way. To a large degree Wells Fargo has stayed above the various banking controversies and has deflected much of the blame and scrutiny accorded others. At some point it becomes clear that prices aren’t likely to drop significantly in the near term, so it may be time to capitulate and get back on the wagon. However, what does give me some solace is that shares have trailed the S&P 500 during the three time frames that I have been recently using, each representing a near term top of the market; May 21, August 2 and September 19, 2013.

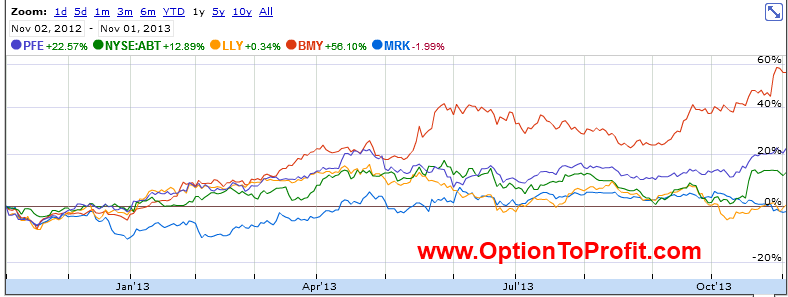

In the world of big pharma, Merck (MRK) has shared in little of the price strength seen by some others. In fact, of late, the

best Merck has been able to do to prompt its shares higher have all come on the less constructive side of the ledger. Only the announcement of workforce reductions and other cost cutting steps have been viewed positively.

But at some point a value proposition is created which isn’t necessarily tied to pipelines or other factors pertinent to long term price health. In this case, a quick 7% price drop is enough to warrant consideration of a company paying an attractive dividend and offering appealing enough option premiums to sustain interest in shares even if they stagnate while awaiting the next price catalysts. Besides, if you’re selling covered calls, there’s nothing better than share price stagnation.

But at some point a value proposition is created which isn’t necessarily tied to pipelines or other factors pertinent to long term price health. In this case, a quick 7% price drop is enough to warrant consideration of a company paying an attractive dividend and offering appealing enough option premiums to sustain interest in shares even if they stagnate while awaiting the next price catalysts. Besides, if you’re selling covered calls, there’s nothing better than share price stagnation.

What is a week without drawing comparisons between Michael Kors (KORS) and Coach (COH)? Coach has become everyone’s favorite company to disparage, although on any given day it may exchange places with Caterpillar. Kors, is of course, the challenger that has displaced Coach in the hearts of investors and shoppers. Having sold Coach puts in advance of earnings and then purchasing shares even after those expired, those were assigned this past week. However, at this price level Coach is still an appealing covered option purchase and well suited for a short term strategy, even if there is validity to the thesis that it is ceding ground to Kors.

Kors, on the other hand, is doing everything right, including entering the S&P 500. It’s hard not to acknowledge its price ascent, even after a large secondary offering. While I know nothing of fashion and have no basis by which to compare Coach and Kors, I do know that as Kors reports earnings this week the option market is implying approximately 7.5% price move in either direction. However, anything less than a 10% decline in price can still deliver a 1% ROI

Williams Companies (WMB) is one of those companies that seems to fly under the radar. Although I’ve owned shares many times there has never been a reason compelling me to do so on the basis of its business fundamentals. Instead, ownership has always been prompted by an upcoming dividend or a sudden price reversal. In this case I just had shares assigned prior to earnings, which initially saw a big spike in price and then an equally large drop, bringing it right back to the level that I have found to be a comfortable entry point.

Riverbed Technology (RVBD) reported earnings last week and I did not purchase additional shares or sell puts, as I thought I might. Too bad, because the company acquitted itself well and shares moved higher. I think that shares are just starting and while RIverbed Technology has probably been my most lucrative trading partner over the years, purely on the basis of option premiums, this time around I am unlikely to write call options on all new shares, as I think $18 is the next stop before year end, particularly if the overall market doesn’t correct.

What can anyone add to the volumes that have been said about Apple (AAPL) and Intel (INTC)? Looking for insights is not a very productive endeavor, as the only new information is likely to currently exist only as insider information. Both are on recent upswings and both have healthy dividends that get my attention because of their ex-dividend dates this week. Intel offers nothing terribly exciting other than its dividend, but has been adding to its price in a stealth fashion of late, possibly resulting in the assignment of some of my current shares that represent one of the longest of my holdings, going back to September 2012. While I have always liked Intel it hasn’t always been a good covered call stock because when shares did drop, such as after earnings, the subsequent price climbs took far too long to continually be able to collect option premiums. However, without any foreseeable near term catalysts for a significant price drop it offers some opportunities for a quick premium, dividend and perhaps share appreciation, as well.

Finally, in its short history of paying dividends Apple’s shares have predominantly moved higher after going ex-dividend, although there was one notable exception. Given the factors that may be supporting Apple’s current price levels, including pressure from activist investors and Apple’s own buybacks, I’m not overly concerned about the single historical precedence and think that the triumvirate of option premium, dividend and share appreciation makes it a good addition to even a conservative portfolio.

Traditional Stocks: AIG, Merck, Williams Companies

Momentum Stocks: Coach, Riverbed Technology

Double Dip Dividend: Apple (ex-div 11/6), Intel (ex-div 11/5), MetLife (ex-div 11/6), Wells Fargo (ex-div 11/6)

Premiums Enhanced by Earnings: Michael Kors (11/5 AM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.