Somewhere along the line most of us have tried the proven strategy of hanging out with people who were uglier or stupider than we perceived ourselves to be, in order to make ourselves look better by comparison.

Somewhere along the line most of us have tried the proven strategy of hanging out with people who were uglier or stupider than we perceived ourselves to be, in order to make ourselves look better by comparison.

There’s nothing really wrong in admitting that to be the case. It’s really the ultimate in victimless opportunism and can truly be a win-win for everyone involved.

The opportunist hopes to break away from that crowd and the crowd feels elevated by its association, or so goes the opportunist’s rationalization.

Markets are no different and this past week was as good of an example of that tried and tested phenomenon as you might ever find. In this case, the opportunist was the US equity market, but it really can rarely be a win-win situation.

Bonds, currencies and precious metals?

Ugly and stupid.

There were three potentially market rocking stories this week that could have struck fear in stock investors, but neither an upcoming FOMC statement, a pending independence referendum in Scotland, nor history’s largest IPO could do what common sense said should occur, particularly with liquidity being threatened from multiple directions.

You can probably thank the less than attractive alternatives for making stocks look so good to investors.

U.S. equity markets just did what we’ve become so accustomed to, other than for brief moments over the past two years, as the week ended on yet another new record high with the DJIA moving higher each day of the week.

Last week was like a perfect storm, except that the winds blew from all different directions during the latter half of the week.

Last week was like a perfect storm, except that the winds blew from all different directions during the latter half of the week.

The week started a bit ominously, but after a while it was clear that selling was narrow in scope and appeared to be limited to profit taking in some of the year’s big gainers, ostensibly to raise cash for any hoped for Alibaba (BABA) allocation, that was unlikely to materialize for most retail investors.

But when the competition is weak, it doesn’t take much to shine and stand out from the crowd. With the week’s first challenge being whether the FOMC was going to accelerate their time table for raising interest rates, all it took was The Wall Street Journal’s Jon Hilsenrath expressing the belief that the phrase “considerable time,” would remain intact to allow stocks to stand out from the crowd.

Never mind that Hilsenrath had yet to demonstrate an inside track to the Yellen Federal Reserve, as he seemed to have had during the Bernanke era. Also forget about the fact that the FOMC has been using that phrase since March 2014 and sooner or later it has to give way to the relization that “considerable time” has already passed. That’s best left to deal with at some other time in the future.

Neither of those were important as all of the other options were looking worse.

With the outcome of the independence referendum being far from certain stocks had been smart enough not to have predicted the eventual outcome and put itself in jeopardy if independence was ratified. Instead the risk was borne by currencies and foreign stock markets.

Precious metals? Who in the world has been putting new money into precious metals of late?

So stocks looked great, but after getting a makeover last week, suddenly the crowd may not look so unappealing. Even precious metals may find some suitors because they just don’t want to chase after stocks and wind up getting disappointed.

Who knew that the high school experience could have taught so much about the behavior of stocks?

The behavior of stocks this week, was also similar to how high school “A-listers” may have acted when pulling in someone from the “losers.” The welcome isn’t always a full and complete embrace and somewhat circumspect or still maintaining an aura of superiority.

In this case the “A-list” DJIA greatly outperformed other major indexes this past week as the advance didn’t fully embrace a broader selection of stocks.

In this case the “A-list” DJIA greatly outperformed other major indexes this past week as the advance didn’t fully embrace a broader selection of stocks.

Despite last week’s nice gains against the odds, in this perfect storm, everything went right. Yet the embrace was with less conviction than it appeared.

That doesn’t mean that I want to go and join the losers, but I may be circumspect of the superficial appearance of those “A-listers” as next week is about to begin.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories.

By comparison, Yahoo (YHOO) looks even less appealing now that it has given up a portion of its stake in Alibaba.

I purchased a small Yahoo position late this past Thursday, when noticing that the in the money option premium was rising even as shares were declining.

The following day I closed those positions shortly after Alibaba started trading as the gain in shares wasn’t matched by a similar gain the premium, resulting in a net credit greater than allowing the position to be assigned.

The funny thing was that the position never would have been assigned as reportedly Yahoo shares were being used a proxy to shorting Alibaba and share price went substantially lower, as a result, even while the value of Yahoo’s remaining stake in Alibaba appreciated by about an additional 37% from the IPO price.

While that kind of short selling strategy may continue, Yahoo is also reportedly becoming the focus of attention from other sources, while it may still stand to benefit from its continuing Alibaba position.

With lots of attention being directed toward its still unproven CEO, Marissa Mayer, as to what she will do with the IPO proceeds, I expect that the Yahoo option premium will remain elevated as so many factors are now coming into play.

While I like those prospects and expect to re-purchase shares, I don’t think that I’ll be allocating too much to this position because of all of the uncertainty involved, but do like the evolving soap opera.

When it comes to comparisons, there’s little that Blackberry (BBRY) can do to make itself look appealing. Where exactly can it hang out to be able to stand out in the crowd and get the attention of those that vote on popularity? Still, under the leadership of John Chen, Blackberry has ended its slide toward oblivion and at least gives appearances of now having a

s

trategy and the ability to execute.

Blackberry reports earnings this coming week and thanks to a lift provided by a Morgan Stanley (MS) analyst out-performed the NASDAQ 100 for the week.

The option market has assigned an implied move of 9.7% for the coming week and at Friday’s closing price a 1% ROI could be obtained even if shares fell by 13.7%. That kind of comparison makes Blackberry look good to me.

While maybe not looking good in comparison to its chief competitor, CVS Health (CVS) on the basis of its self proclaimed status of the guardians of the nation’s health after belatedly eliminating the sale of cigarettes from its stores, Walgreen looks food to me. That’s especially the case now that it seems to be settling into a trading range after it, too, belatedly, decided against a tax inversion strategy.

Walgreen, as with many other stocks trading in a range, but occasionally punctuated by substantive price moves related to earnings or other events, offers a nice option premium that may exceed the current risk of share ownership.

Until recently the comparison to gold during the summer worked out well for Market Vectors Gold Miners ETF (GDX), having out-performed the SPDR Gold Trust (GLD). More recently, however, the Miners Index has had an abysmal month of September and is approaching a 2 year low. However, its beta is still quite low and shares are now trading below their yearly mid-point range, while offering a premium that may offset what I believe to be limited downside risk.

I don’t look at ETF vehicles very often, but this one may be right in terms of timing and price. The availability of expanded weekly options, strike prices in $0.50 increments and manageable bid-ask spreads makes this potentially a good candidate for serial rollover if it finds some support and begins trading in a range.

Fastenal (FAST) is one of those stocks that may not have much glamour and may not stand out sufficiently to get noticed. To me, though, it is a superstar in the world of covered options as it has traded reliably within a range and consistently returned to the mid-point of that range, where it currently resides.

Having rolled over shares this past Friday after a mid-session drop below the strike, I watched as it recovered enough to close above the strike. Had it been assigned, as originally thought would occur, I knew that at its current price I wanted to re-purchase shares. Instead, now I want to add shares, but being mindful that it will report earnings in just a few weeks.

Despite Alibaba’s successful IPO, it’s still difficult for me to have too much confidence in stocks that have either a heavy reliance on the Chinese economy or are Chinese companies. Fortunately or unfortunately, I do make exceptions for both situations, although far fewer for the latter.

Joy Global (JOY) has extensive interests in China and is very dependent on continued growth of the Chinese economy, which is difficult to measure with reliability. Of course with our own GDP being reported this coming Friday, we know all too well, based on the recent pattern of revisions, that data should always be viewed warily.

With some weakness in this sector, witness the recent drop in Caterpillar (CAT), Joy Global is approaching correction territory over the past month and is beginning to once again look appealing, not having owned shares in nearly a year. These shares can be volatile, but with patience and an inner sense of serenity, the option premiums can atone for moments of anxiety.

Despite still holding a very expensive lot of Coach (COH) shares for far too long, it is still one of my favorite stocks over the longer term time frame, having owned it on 21 occasions over 25 months.

Smarting from the pain of that lot I still hold, it took a while before finding the courage to purchase an additional lot, but that recent lot was assigned this past week and I’m ready to add another in its place, as it seems that Coach has found some support at its current level. In the past Coach has been an excellent covered option trade when it traded in a range. The reason for it offering attractive option premiums was due to its predictably large earnings related moves. However, in the past, it had a wonderful habit of its price reverting to the mean.

If so, I don’t mind executing serial trades, reaping premiums and the occasional premium to help offset the existing paper loss. As the luster from Kors (KORS) seems to be waning there is also less populist battering of Coach, which remains very popular internationally. It’s commitment to maintaining its dividend makes it easy to hold shares while awaiting what I hope is an inevitable, albeit, unusually slow recovery.

Whole Foods (WFM) is another of those companies that I own that is currently well below its purchase price. As with Coach, I eventually found the courage to purchase more shares and have done so 4 times in the past 3 months, as it appears to have also found some price support.

Recently its premiums have become more attractive as the company has become a topic of speculation regarding activist intervention. While I don’t think there’s too much to come of that speculation, I do believe that shares are poised to continue climbing and hopefully in a slow and sustained manner. It goes ex-dividend this week and while not the most generous of dividends it does supplement the potential return offered by also selling call options on shares sufficiently to make it an attractive consideration.

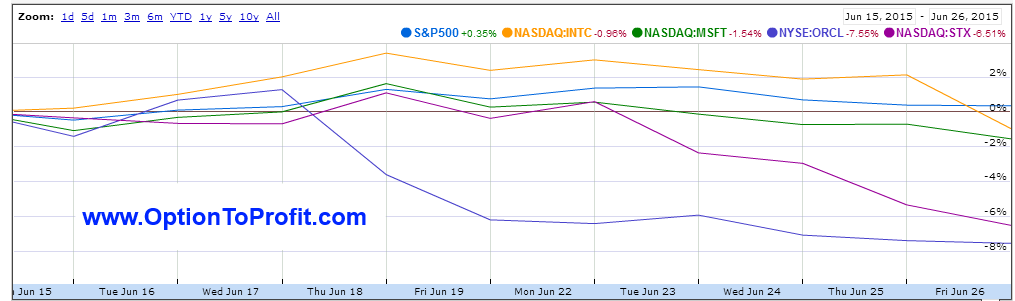

Finally, Oracle (ORCL) is back in the news and in the last couple of years that hasn’t really been a good thing. After a number of disappointing earnings reports over that time, its Chairman and CEO, Larry Ellison, blasted those around him, finding plenty of places to lay blame. His absence from last year’s earnings report and conference in order to attend Oracle Team USA’s effort in the Americas Cup race struck me as inappropriate.

Now the news of Ellison stepping down as CEO, while retaining the Chairmanship, preceded this most recent quarter’s disappointing earnings. It also was a prelude to the announcement of a power sharing plan with the appointment of co-CEOs, because we all know how much high achievers like to share power and glory.

Yet, with this past Friday’s price decline in Oracle it is again becoming a potentially attractive purchase candidate, particularly with an upcoming, albeit modest dividend coming on October 6, 2014.

That happens to be a Monday, and I wish there were more such Monday opportunities for those stocks that I follow. Those are often the best of the “Double Dip Dividend” selections, as early assignment to capture the dividend must occur o�n� the preceding Friday and typically means receiving an entire week’s option premium, while being able to reinvest the exercise proceeds to generate even more income.

Traditional Stocks: Fastenal, Market Vectors Gold Miners ETF, Oracle, Walgreen

Momentum: Coach, Joy Global, Yahoo

Double Dip Dividend: Whole Foods (9/24 $0.12)

Premiums Enhanced by Earnings: Blackberry (9/23 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

To call the stock market of this past week “a dog” probably isn’t being fair to dogs.

To call the stock market of this past week “a dog” probably isn’t being fair to dogs.

Fresh off of his estate’s victory in a copyright infringement suit, Marvin Gaye comes to my mind this week as I can’t help but wonder what’s going on.

Fresh off of his estate’s victory in a copyright infringement suit, Marvin Gaye comes to my mind this week as I can’t help but wonder what’s going on. Maybe I belong to a different generation, but I have certain expectations regarding behavior and responsibility, especially when other’s are your subordinates and maybe even extending to your shareholders.

Maybe I belong to a different generation, but I have certain expectations regarding behavior and responsibility, especially when other’s are your subordinates and maybe even extending to your shareholders.