The investing community is either really old or thinks it’s really well versed in history.

The investing community is either really old or thinks it’s really well versed in history.

The prospects of interest rates going higher must be evoking memories of the Jimmy Carter era when personal experiences may have been pretty painful if on the wrong side of a prime interest rate of 21.5%.

I’d be afraid, too, of reliving the prospects of having to take out a 20% loan on my Chevrolet Vega.

The interest rate isn’t what would bother me, though. That Vega still evokes nightmares.

If not old enough to have had those personal experiences, then investors must be great students of history and simply fear the era’s repeat.

Unfortunately, neither group seems to readily recall the experiences of the intervening years when hints of inflation appearing over the horizon were addressed by a responsive Federal Reserve and not the Federal Reserve presided over by the last Chairman to have come from a corporate background.

It’s unfortunate only because the stock market has been held hostage, despite having reached new highs recently, by fears of a return to a long bygone era, which was also characterized by a passive Federal Reserve Chairman who opposed raising interest rates as a fiscal tool and while inflation was rapidly growing, believed that it would self-correct.

G. William Miller was certainly correct on that latter belief as rates did self-correct once reaching that 21.5% level, although they lasted longer than did most people’s Vegas, while Miller’s length of tenure as Chairman of the Federal Reserve did not.

Passivity and benign neglect weren’t the best ways to approach an economy then and probably not a very good way to do so now.

This past week seemingly provided more of the confirmatory data the FOMC has been waiting upon to make the long signaled move that has also been long feared. Following the previous week’s Employment Situation Report and this past week’s JOLTS report and Retail Sales report, every indication is now pointing to an economy that is heating up.

Not as much as the crankcase of my Vega that caused so many engine blocks to crack, but enough to get the FOMC to act in a way that the interest rate dovish Miller would not.

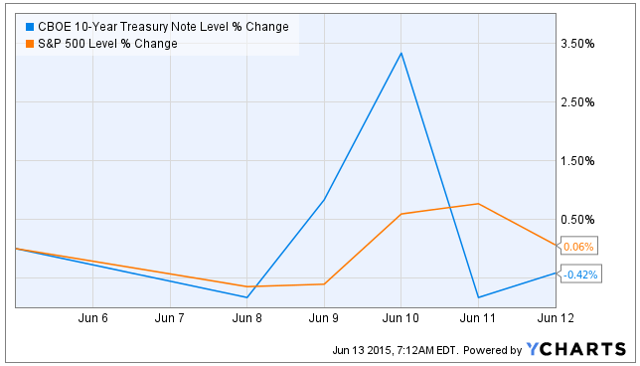

Still, the various bits of information coming in during the week caused major moves in both stock and bond markets, although the cumulative impact was negligible, even while the details were attention getting.

While Janet Yellen has been referred to as a “dove,” when compared to Miller, she is a ravenous hawk who only needs a clear signal of when to swoop. While the FOMC will meet this week it’s not too likely that there will be any policy changes announced, although sometimes it’s all about the wording used to describe the committee’s thoughts.

As recently as 2 weeks ago many were thinking that rate hikes might not come until 2016. However, now the prevailing chatter is that September 2015 is the target date for action.

However with the July 2015 meeting coming at the very end of the month and the opportunity to peruse another month’s worth of data what would be easier than making that decision then, particularly coming in-between June and September scheduled press conferences?

That would take most by surprise, but at least it gets this ordeal over.

Like so many things in life, the anticipation can be the real ordeal as the reality pales in comparison. Somehow, though, that’s not a lesson that’s rea�dily learned.�

Unless the upcoming earnings season will have some very nice upside surprises due to a continuing strengthening of the US Dollar that never arrived, there doesn’t appear to be any catalyst on the horizon to prompt the stock market to test its highs. That is unless we finally get a chance to remove the yoke of fear.

Real students of history will know that the fear of those interest rate hikes, especially in the early stages of an overtly improving economy, is unwarranted.

After a week of not opening a single new position I’d love to see some clarity that can only come from FOMC decisiveness. It may well be a long hot summer ahead, but it’s time to embrace the heating up of the economy for what it is and celebrate its arrival and put the ghost of G. William to rest.

As usual, the week’s potential stock selections are classified as being in Traditional, Double-Dip Dividend, Momentum or “PEE” categories.

While markets were gyrating wildly this past week and news regarding Greece, the IMF and ECB kept going back and forth, I found myself shaking my head as the biggest story of the week seemed to be the upcoming CEO change at Twitter (TWTR).

Although I am short puts and have a real interest in seeing shares rise, I sat wondering why a company that was so small, employed so few people and contributed so little to the economy, could possibly receive so much attention for a really inconsequential story.

Beyond that, the company could go away tomorrow and its 300 million monthly active users wouldn’t be facing a gap very long others in Silicon Valley could step in to fill that gap in a heartbeat and do so without all of the dysfunction characterizing the company.

One thing that strikes me is that with the change the Board of Directors will continue to have 3 past CEOs. A friend of mine was once Chairman of an academic department that had 4 past Chairman still active on the faculty. He said it was absolutely intolerable and he couldn’t act with

out continuing second guessing and sniping.

Among the characteristics of some selections this week is strong and unequivocal leadership. Right or wrong, it helps to be decisive.

It also helps to offer a dividend, as that’s another recurring theme for me, of late.

General Electric (GE) has been led by the same individual for nearly 15 years. While it may not be helpful to his legacy to compare General Electric’s stock performance relative to the S&P 500 under his tenure to that of his predecessor, no one can accuse GE of standing still and being indecisive.

The one thing that I continually bemoan is that I haven’t owned shares of GE as often as I should have over the past few years. Despite it’s relative under-performance over the years, other than 2015 YTD, it has been a very reliable covered call position. Its fairly narrow trading range, reasonable premium and its safe and excellent dividend are a great combination if not looking for dizzying growth and the risk that attends such growth.

Shares are ex-dividend this week and that may be the motivator I need to consider committing some funds at a time when I’m not terribly excited about doing so.

Although Larry Ellison has stepped back from some of his responsibilities at Oracle (ORCL), there’s not too much doubt that he is in charge. Who other than such a powerful leader could convince two other powerful business leaders to be in a CEO sharing arrangement?

Oracle reports earnings this week and is expected to go ex-dividend during the July 2015 option cycle. The options market is predicting only a 3.9% price move over the course of the coming week.

There isn’t an appealing premium available for selling puts outside of the price range predicted by the options market, but Oracle is a company that I wouldn’t mind owning, rather than simply taking advantage of it to generate earnings volatility induced premiums. It’ like GE, is a company that I haven’t owned frequently enough over the years, as it has also been a very good covered call position, even while frequently trailing the S&P 500 over recent years.

Cypress Semiconductor (CY) is another company with a strong leader, who also happens to be a visionary. It’s stock price surged upon news that it was going to acquire Integrated Silicon Solution (ISSI), but over the past week has been on somewhat of a rollercoaster ride as the buyout went from Cypress Semiconductor missing a self-designated deadline to obtain regulatory approval, to then arranging financing and culminating in ISSI announcing that it had accepted the Cypress offer.

Or so it seemed.

That rollercoaster ride is likely to continue next week as the coveted buyout target has just recommended accepting an offer from a Chinese private equity consortium just a day after announcing it had accepted Cypress’ offer.

A special meeting of ISSI stockholders has now been called for June 19, 2015. Wi�th a close eye on that meeting and its outcome, I would consider waiting until then to make a decision of Cypress Semiconductor shares, that will go ex-dividend the following week.

While it’s clear that the market valued the combination of the two companies, the disappointment may now be factored in, although perhaps not fully. Cypress Semiconductor is a company that I’ve long admired, particularly as it has acted as an technology incubator and have liked as a covered option trade, although at a lower price.

American Express (AXP) has also been led by a strong CEO for nearly 15 years. Of late, he may have been subject to some criticism for the opacity related to the company’s relationship with Costco (COST), as their co-branding credit card agreement will be ending in 2016 and surprisingly represented a large share of American Express’ profits. However, for much of the earlier years American Express was a good investment vehicle and offered a differentiated and profitable product.

Since that announcement and once the surprise was digested, American Express has traded in a narrow range following a precipitous drop in shares that discounted the earnings hit that was still to be a year away.

That steadiness in share price with the overhang of uncertainty, has made shares another good covered call and they, too, will be ex-dividend during the July 2015 option cycle.

International Paper (IP) may stand as the exception to the previous stocks. It has a new CEO and won’t be offering a dividend until the August or September 2015 cycle.

In fact, its recently retired CEO was once on a CNNMoney list of the 5 most over-paid CEOs.

What it does have is a recent 10% decline in share price that has finally brought it back to the neighborhood in which I wouldn’t mind considering shares. Like GE and Oracle, in hindsight, I wish I had owned shares more frequently over the years, not because of its share out-performance, as that certainly figured into the poor value received from its past CEO, but rather from that steady combination of option premiums and dividends along with a reasonably steady share price.

Finally, although the sector isn’t very large, there hasn’t been a shortage of activity going in within the small universe of telecommunications companies and cable and satellite providers, of late.

Verizon (VZ) has been making its own news with a �proposed buyout of AOL (AOL), which is a relatively small one when compared to the other deals being made or proposed.

While matching the performance of the S&P 500 YTD, it is lagging well behind in the past month, but in doing so, it is also becoming more attractive, as it returns to the $47 neighborhood. It also will be going ex-dividend in the July 2015 option cycle and always has a reasonable option premium relative to the manageable risk that it generally offers.

At a time when there is ongoing market certainty there is a certain amount o

f comfort that comes from dividends and that comfort makes decisions easier to make.

Traditional Stocks: American Express, Cypress Semiconductor, International Paper, Verizon

Momentum Stocks: none

Double-Dip Dividend: General Electric (6/18)

Premiums Enhanced by Earnings: Oracle (6/17 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

June 8 – 12, 2015

June 8 – 12, 2015