Daily Market Update – April 28, 2014 (Close) When the morning started I thought this week may be an interesting one. Well, if today is an indication, I’ve had enough interesting stiff to last me for the week. The movements today wewn’t the kind that we see very often. Where the market got back its confidence in the final hour is really a mystery. For starters, nothing happened over the weekend on the international scene, as was the fear on Friday and may have accounted for the weakness to end last week. Even those used to having seen these kind of brinksmanship games may have thought that something, perhaps unintentional, was going to result in an adverse event and subsequent fall-out in the markets. So without that overhang it’s getting off to a push higher with word of increased merger and buy out activity and a sense of relief. The relief, could still, however, be short-lived.. Then later in the week are the FOMC announcement and the Employment Situation Report. The last time around both of those saw surprising strong turnaround sell-offs following initially positive responses. In both cases neither the initial responses nor the reversals were very rational because neither really introduced any new news. Also this morning, just before the opening bell came word that some further sanctions will be levied against Russia, but like the previous ones, they are directed toward individuals, so it remains to be seen how the market looks at them. Basically, the more biting the sanctions the more bearish the market reaction. This is another week that I would be content to let prices move higher even if that was without much in the way of new purchases for the week. I would like to see the higher prices open up opportunities to just sell more calls on existing positions. As with some previous weeks, with enough positions set to expire this Friday, where possible I’d like to begin populating next week or even the monthly expiration with expiring contracts, rather than adding to the already lengthy list this week. With a handful of assignments my cash reserves are higher but they are so after coming off from a recent low point. I would very much like to see that level get even higher so I’m not likely to chase after new positions and may return to the low level of buying activity from two and three weeks ago. As long as there are opportunities to generate income from existing positions that’s acceptable, but only for so long. With the market pointing toward a higher open this morning I will sit and see if it has any legs before getting overly excited. With news of some additional sanctions against Russia will certainly come some response which may have its own impact, so I plan to tread softly this morning. After a few weeks of really nothing going on it’s actually nice to see some many different factors entering into the equation, although I may end up regretting that feeling, as sometimes boredom is better than unnecessary excitement. While anything can bring opportunity too much of the unknown isn’t something that really benefits anyone. Hopefully some clarity and some rational thought returns to the market and lets it simply concentrate on earnings and fundamentals, although hoping for that may itself be fairly irrational, given past history. Today’s market did nothing to add to the clarity but at least you have to have a little more confidence heading into tomorrow after the really nice reversal of the reversal. Then again, there’s always tomorrow to throw a wrench into well thought out plans, but it is a Tueday and we all know what that means. |

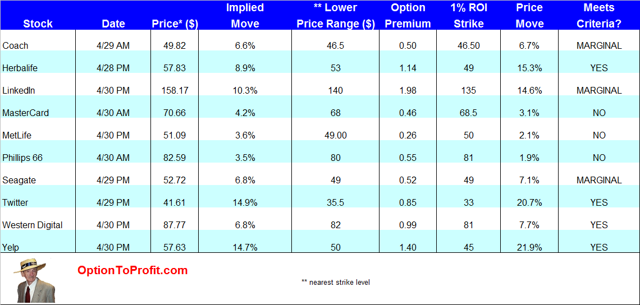

Increasingly for that more speculative portion of my portfolio I look at earnings season as being a great time to generate quick, albeit sometimes nerve wracking, income from those stocks that can be unpredictable in their typical daily trading and even more so when earnings and guidance are at hand.

Increasingly for that more speculative portion of my portfolio I look at earnings season as being a great time to generate quick, albeit sometimes nerve wracking, income from those stocks that can be unpredictable in their typical daily trading and even more so when earnings and guidance are at hand.