There was a time that most everyone who had a computer knew exactly what the word “Wintel” meant.

There was a time that most everyone who had a computer knew exactly what the word “Wintel” meant.

The combination of Microsoft (MSFT) and Intel (INTC) vanquished the competitors. You don’t hear or see too many Commodore, Tandy or Kaypro computers these days running on their own operating systems, or at all, for that matter. The combination became especially potent after MS-DOS became simply the shell for the graphic user interface that Microsoft was luckily able to render from Apple (AAPL) for nothing more than the cost of a legal defense. Although Advanced Microdevices (AMD) computer chips are still finding their way into lower priced computer systems, others, such as Cyrix and Zilog have long since ceded the computer microprocessor space to Intel.

The timing couldn’t have been better. If you’re going to be at the top of the competitive heap what better time than during a phase of tremendous marketplace growth? The real heyday of “Wintel” began with the introduction of the Windows 95 operating system and the mass production of cheaper hardware by the likes of assemblers like Dell (DELL) and Gateway, who back during that era never manufactured a machine with anything other than a Microsoft operating system and an Intel chip.

Wintel. Windows and Intel.

While Apple and its operating system powered by varied IBM (IBM) and Motorola (MSI) chips may have been, according to devotees, a far superior consumer product, it’s market penetration was no more than a nuisance to the Wintel alliance.

But as so often happens with size comes complacency and perhaps losing sight of events going on where your toes used to be. Add to that an occasionally less than inspired leadership and supremacy can devolve into mediocrity.

Not seeing or not being adequately nimble enough to recognize and react to the revolution in personal computing, beginning with the smartphone and then the tablet, Microsoft and Intel both ceded ground to Apple and smaller chip manufacturers in markets that hadn’t previously existed. Those new markets also had the ability to cannibalize existing markets, particularly for personal computers.

Whether Qualcomm (QCOM), ARM Holdings (ARMH) or others, the mobile and tablet markets erupted with neither a “win” nor a “tel” along for the ride.

The past decade has been a veritable wasteland for both Microsoft and Intel with regard to their perceived place in consumer technology. Although Apple Computer successfully transitioned to Intel processors, they didn’t look to Intel for its explosive growth in the mobile market and for the new tablet market. When you’re the size of Intel, the addition of Apple computers to your stable isn’t the kind of stimulus that’s going to push the needle very much. It certainly wasn’t enough to fuel growth.

That’s not to say that neither Microsoft nor Intel have stood still in their own technological and product advances or taken the opportunity to expand into new areas, such as gaming consoles. But their stranglehold on households has diminished during an era when “eco-system” has become the new buzzword replacing “Wintel.”

But faster than you can say “Moore’s Law,” the landscape is changing, yet again, as it appears that Apple is now the one having some difficulty remembering where its toes are located. For more than a decade the very essence of engineering marvels that also captured the consumer’s fancy, Apple has slowed down and has become susceptible to competition.

Unless you have been hiding in a cave you haven’t seen the onslaught of Microsoft ads on television and in movie theaters. They are now pushing their own eco-system in tablets, smartphones and computers, as well as in the gaming world. Less well seen are the acquisition of data centers and ventures to move software into the cloud, including an impending partnership with Oracle (ORCL).

It was once a Windows world and Microsoft is addressing the convergence of the PC, laptop, tablet and communication devices through a singular operating system in order to ensure that it remains a Windows world, with or without Intel. Retaining control of that niche is far more important than capturing a nascent mp3-player market. Success of the Zune wasn’t necessary for continued sales of the Office Suite, but maintaining supremacy of the personal computing and tablet market is required in order for that cash cow to keep the enterprise afloat. It is far more important to get this battle won than some earlier generation diversions.

Even more of a signal of commitment toward the futu

re is the rumored restructuring of Microsoft that will place greater emphasis on hardware as Microsoft takes control of its own destiny in support of vehicles to propagate its software platforms.

Borrowing a page from Ron Johnson, who was credited with the success of the Apple stores, and who didn’t survive his tenure as CEO at JC Penney (JCP) to see the store within a store concept play out, Microsoft, along with Samsung (SSLNF.PK) is employing the concept within a resurgent and re-energized Best Buy (BBY), putting itself directly in the eyes and into the hands of the buying public.

While Intel is no longer Microsoft’s sole and unqualified partner in their new ventures, their future is increasingly looking brighter than it has in years.

Intel is now under the new leadership of an individual who breathes operations, following a period of listless direction that was in sharp contrast to the great vision and leadership that had previously marked Intel’s executive offices. The announcement earlier in the year that Samsung, the very same company that has been eating away at Apple’s place in consumer’s hearts, had selected Intel for its new line of tablets should serve notice that Intel is back.

Add to that the growing presence of Intel chips in smartphones, including those made by Motorola Mobility, which is now owned by Google (GOOG), and you have the largest of the mobile phone operating systems able to be run by a new generation of Intel chips and easily transferred into Android tablets, as well.

Take that ARM.

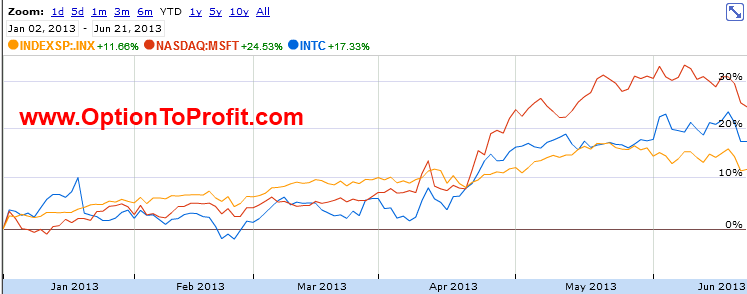

Thus far both Intel and Microsoft have outperformed the S&P 500 in 2013.

Thus far both Intel and Microsoft have outperformed the S&P 500 in 2013.

In 2012 Microsoft continued to receive its share of disparaging comments by analysts taking delight in referring to it as “dead money.” Those jeers ended when shares surpassed $30 at which point everyone seemed to climb aboard. Of course that heralded the end of the upward climb. In 2013 very much the same phenomenon was repeated when shares again broke through the $30 barrier and it again became acceptable to admit that Microsoft was part of your portfolio.

I do not currently own shares but am anxious to purchase them once again if share price returns to the $30 level, as I have used Microsoft as an annuity for years, collecting dividends and premiums from having sold options.

Intel is a bit of a different story. While it too has traded in a fairly narrow range and hasn’t been terribly exciting unless collecting dividends and option premiums, I think that it is fair priced at current levels and would add additional shares below $25.

While the world may no longer be quite the Wintel world it was 10 years ago, as a stock investor, Wintel is a winning combination even if they are going increasingly their own separate ways in the consumer marketplace.

Individually or together, Microsoft and Intel can serve as linchpins of a portfolio, if you’re ready to go for the win.