![]() Everything is crystal clear now.

Everything is crystal clear now.

After three straight weeks of losses to end the trading week, including deep losses the past two weeks everyone was scratching their heads to recall the last time a single month had fared so poorly.

What those mounting losses accomplished was to create a clear vision of what awaited investors as the past week was to begin.

Instead, it was nice to finish on an up note to everyone’s confusion.

When you think you are seeing things most clearly is when you should begin having doubts.

Who saw a two day 350 point gain coming, unless they had bothered to realize that this week was featuring an Employment Situation Report? The one saving grace we have is that for the past 18 months you could count on a market rally to greet the employment news, regardless of whether the news met, exceeded or fell short of expectations.

That’s clarity. It’s confusing, but it’s a rare sense of clarity that comes from being so successful in its ability to predict an outcome that itself is based upon human behavior.

As the week began with a 325 point loss in the DJIA voices started bypassing talk of a 10% correction and starting uttering thoughts of a 15-20% correction. 10% was a bygone conclusion. At that point most everyone agreed that it was very clear that we were finally being faced with the “healthy” correction that had been so long overdue.

When in the middle of that correction nothing really feels very healthy about it, but when people have such certainty about things it’s hard to imagine that they might be wrong. With further downside seen by the best and brightest we were about to get healthier than our portfolios might be able to withstand.

It was absolutely amazing how clearly everyone was able to see the future. What made things even more ominous and sustaining their view was the impending Employment Situation Report due at the end of the week. Following last month’s abysmal numbers, ostensibly related to horrid weather across the country, there wasn’t too much reason to expect much in the way of an improvement this time around. Besides, the Nikkei and Russian stock markets had just dipped below the 10% threshold that many define as a market correction and as we’re continually reminded, it’s an inter-connected world these days. It wasn’t really a question of “whether,” it was a matter of “when?”

Then there was all that talk of how high the volatility was getting, even though it had a hard time even getting to October 2013 levels, much less matching historical heights. As everyone knows, volatility comes along with declining markets so the cycle was being put in place for the only outcome possible.

After Monday’s close the future was clear. Crystal clear.

Instead, the week ended with an 0.8% gain in the S&P 500 despite that plunge on Monday and a highly significant drop in volatility. The market responded to a disappointing Employment Situation Report with what logically or even using the “good news is bad news” kind of logic should not have been the case.

Now, with a week that started by confirming the road to correction we were left with a week that supported the idea that the market is resistant to a classic correction. Instead of the near term future of the markets being crystal clear we are left beginning this coming week with more confusion than is normally the case.

If it’s true that the market needs clarity in order to propel forward this shouldn’t be the week to commit yourself. However, the only thing that’s really clear about our notions is that they’re often without basis so the only reasonable advice is to do as in all weeks – look for situational opportunities that can be exploited without regard to what is going on in the rest of the world.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

If you’re looking for certainty, or at least a company that has taken steps to diminish uncertainty, Microsoft (MSFT) is the one. With the announcement of the appointment of Satya Nadella, an insider, to be its new CEO, shares did exactly what the experts said it wouldn’t do. Not too long ago the overwhelming consensus was that the appointment of an outsider, such as Alan Mullaly would drive shares forward, while an insider would send shares tumbling into the 20s.

Microsoft simply stayed on its path with the news of an inside candidate taking the reigns. Regardless of its critics, Microsoft’s strategy is more coherent than it gets credit for and this leadership decision was a quantum leap forward, certainly far more important than discussions of screen size. With this level of certainty also comes the certainty of a dividend and attractive option premiums, making Microsoft a perennial favorite in a covered option strategy.

The antithesis of certainty may be found in the smallest of the sectors. With the tumult in pricing and contracts being promulgated by T-Mobile (TMUS) and its rebel CEO John Legere, there’s no doubt that the margins of all wireless providers is being threatened. Verizon (VZ) has already seen its share price make an initial response to those threats and has shown resilience even in the face of a declining market, as well. Although the next ex-dividend date is still relatively far away, there is a reason this is a favorite among buy and hold investors. As long as it continues to trade in a defined range, this is a position that I wouldn’t mind holding for a while and collecting option premiums and the occasional dividend.

Lowes (LOW) is always considered an also ran in the home improvement business and some recent disappointing home sales news has trickled down to Lowes’ shares. While it does report earnings during the first week of the March 2014 option cycle, I think there is some near term opportunity at it’s current lower price to see some share appreciation in addition to collecting premiums. However, I wouldn’t mind being out of my current shares prior to its scheduled earnings report.

Among those going ex-dividend this week are Conoco Phillips (COP), International Paper (IP) and Eli Lilly (LLY). In the past month I’ve owned all three concurrently and would be willing to do so again. While International Paper has outperformed the S&P 500 since the most recent market decline two weeks ago, it has also traded fairly rangebound over the past year and is now at the mid-point of that range. That makes it at a reasonable entry point.

Conoco Phillips appears to be at a good entry point simply by virtue of a nearly 12% decline from its recent high point which includes a 5% drop since the market’s own decline. With earnings out of the way, particularly as they have been somewhat disappointing for big oil and with an end in sight for the weather that has interfered with operations, shares are poised for recovery. The premiums and dividend make it easier to wait.

Eli Lilly is down about 5% from its recent high and I believe is the next due for its turn at a little run higher as the major pharmaceutical companies often alternate with one another. With Pfizer (PFE) and Merck (MRK) having recently taken those honors, it’s time for Eli Lilly to get back in the short term lead, as it is for recent also ran Bristol Myers Squibb (BMY) that was lost to assignment this past week and needs a replacement, preferably one offering a dividend.

Zillow (Z) reports earnings this week. In its short history as a publicly traded company it has had the ability to consistently beat analyst’s estimates and then usually see shares fall as earnings were released. That kind of doubled barrel consistency warrants some consideration this week as the option market is implying an 11% move this week. While that is possible, there is still an opportunity to generate a 1% ROI for the week if the share price falls by anything less than 16%.

While I’m not entirely comfortable looking for volatility among potential new positions two that do have some appeal are Coach (COH) and Morgan Stanley (MS).

Coach is a frequent candidate for consideration and I generally like it more when it’s being maligned. After last week’s blow-out earnings report by Michael Kors (KORS) the obvious next thought becomes how their earnings are coming at the expense of Coach. While there may be truth to that and has been the conventional wisdom for nearly 2 years, Coach has been able to find a very comfortable trading range and has been able to significantly increase its dividend in each of the past 4 years in time for the second quarter distribution. It’s combination of premiums, dividends and price stability, despite occasional swings, makes it worthy of consistent consideration.

I’ve been waiting for a while for another opportunity to add shares of Morgan Stanley. Down nearly 12% in the past 3 weeks may be the right opportunity, particularly as some European stability may be at hand following the European Central Bank’s decision to continue accommodation and provide some stimulus to the continent, where Morgan Stanley has interests, particularly being subject to “net counterparty exposure.” It’s ride higher has been sustained and for those looking at such things, it’s lows have been consistently higher and higher, making it a technician’s delight. I don’t really know about such things and charts certainly aren’t known for their clarity being validated, but its option premiums do compel me as do thoughts of a dividend increase that it i increasingly in position to institute.

Finally, if you’re looking for certainty you don’t have to look any further than at Chesapeake Energy (CHK) which announced a significant decrease in upcoming capital expenditures, which sent shares tumbling on the announcement. Presumably, it takes money to make money in the gas drilling business so the news wasn’t taken very well by investors. A very significant increase in option premiums early in the week suggested that some significant news was expected and it certainly came, with some residual uncertainty remaining in this week’s premiums. For those with some daring this may represent the first challenge since the days of Aubrey McClendon and may also represent an opportunity for shareholder Carl Icahn to enter the equation in a more activist manner.

Traditional Stocks: Lowes, Microsoft, Verizon

Momentum Stocks: Chesapeake Energy, Coach, Morgan Stanley,

Double Dip Dividend: Conoco Phillips (ex-div 2/13), International Paper (ex-div 2/12), Eli Lilly (ex-div 2/12)

Premiums Enhanced by Earnings: Zillow (2/12 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – August 4, 2013

To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.

To summarize: The New York Post rumors, “The Dark SIde” and the FOMC.

This was an interesting week.

It started with the always interesting CEO of Overstock.com (OSTK) congratulating Steve Cohen, the CEO of SAC Capital, on his SEC indictment and invoking a reference to Star Wars to describe Cohen’s darkness, at least in Patrick Byrne’s estimations.

It ended with The New York Post, a one time legitimate newspaper suggesting that JC Penney (JCP) had lost the support of CIT (CIT), the largest commercial lender in the apparel industry, which is lead by the charisma challenged past CEO of The NYSE (NYX) and Merrill Lynch, who reportedly knows credit risk as much as he knows outrageously expensive waiting room and office furniture.

The problem is that if CIT isn’t willing to float the money to vendors who supply JC Penney, their wares won’t find their way into stores. Consumers like their shopping trips to take place in stores that actually have merchandise.

At about 3:18 PM the carnage on JC Penney’s stock began, taking it from a gain for the day to a deep loss on very heavy volume, approximately triple that of most other days.

Lots of people lost lots of money as they fled for the doors in that 42 minute span, despite the recent stamp of approval that George Soros gave to JC Penney shares. His money may not have been smart enough in the face of yellow journalism fear induced selling.

The very next morning a JC Penney spokesperson called the New York Post article “untrue.” It would have helped if someone from CIT chimed in and set the record straight. While the volume following the denial was equally heavy, very little of the damage was undone. As an owner of shares, Thane’s charisma would have taken an incredible jump had he added clarity to the situation.

So someone is lying, but it’s very unlikely that there will ever be a price to be paid for having done so. Clearly, either the New York Post is correct or JC Penney is correct, but only the New York Post can hide behind journalistic license. In fact, it would be wholly irresponsible to accuse the article of promoting lies, rather it may have recklessly published unfounded rumors.

By the same token, if the JC Penney response misrepresents the reality and is the basis by which individuals chose not to liquidate holdings, the word “criminal” comes to my mind. I suppose that JC Penney could decide to create a “Prison within a Store” concept, if absolutely necessary, so that everyday activities aren’t interrupted.

For the conspiracy minded the publication of an article in a “reputable” newspaper in the final hour of trading, using the traditional “unnamed sources” is problematic and certainly invokes thoughts of the very short sellers demonized by Patrick Byrne in years past.

Oh, and in between was the release of the FOMC meeting minutes, which produced a big yawn, as was widely expected.

I certainly am not one to suggest that Patrick Byrne has been a fountain of rational thought, however, it does seem that the SEC could do a better job in allaying investor concerns about an unlevel playing field or attempts to manipulate markets. Equally important is a need to publicly address concerns that arise related to unusual trading activity in certain markets, particularly options, that seem to occur in advance of what would otherwise be unforeseen circumstances. Timing and magnitude may in and of themselves not indicate wrongdoing, but they may warrant acknowledgement for an investing public wary of the process. A jury victory against Fabrice Tourre for fraud is not the sort of thing that the public is really looking for to reinforce confidence in the process, as most have little to no direct interaction with Goldman Sachs (GS). They are far more concerned with mundane issues that seem to occur with frequency.

Perhaps the answer is not closer scrutiny and prosecution of more than just high profile individuals. Perhaps the answer is to let anyone say anything and on any medium, reserving the truth for earnings and other SEC mandated filings. Let the rumors flow wildly, let CEOs speak off the top of their heads even during “quiet periods” and let the investor beware. By still demanding truth in filings we would still be at least one step ahead of China.

My guess is that with a deluge of potential misinformation we will learn to simply block it all out of our own consciousness and ignore the need to have reflexive reaction due to fear or fear of missing out. In a world of rampantly flying rumors the appearance of an on-line New York Post article would likely not have out-sized impact.

Who knows, that might even prompt a return to the assessment of fundamentals and maybe even return us to a day when paradoxical thought processes no longer are used to interpret data, such that good news is actually finally interpreted as good news.

I conveniently left out the monthly Employment Situation Report that really ended the week, but as with ADP and the FOMC, expectations had already been set and reaction was muted when no surprises were in store. The real surprise was the lack of reaction to mildly disappointing numbers, perhaps indicating that we’re over the fear of the known.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories. (see details).

One of last week’s earnings related selections played true to form and dropped decidedly after earnings were released. Coach (COH) rarely disappoints in its ability to display significant moves in either direction after earnings and in this case, the disappointment was just shy of the $52.50 strike price at which I had sold weekly puts. However, with the week now done and at its new lower price, I think Coach represents a good entry point for new shares. With its newest competitor, at least in the hearts of stock investors, Michael Kors (KORS) reporting earnings this week there is a chance that Coach may drop if Kors reports better than expected numbers, as the expectation will be that it had done so at Coach’s expense. For that reason I might consider waiting until Tuesday morning before deciding whether to add Coach to the portfolio.

Although I currently own two higher priced lots of its shares, I purchased additional shares of Mosaic (MOS) after the plunge last week when perhaps the least known cartel in the world was poised for a break-up. While most people understand that the first rule of Cartel Club is that no one leaves Cartel Club, apparently that came as news to at least one member. The shares that I purchased last week were assigned, but I believe that there is still quite a bit near term upside at these depressed prices. While theories abound, such as decreased fertilizer prices will lead to more purchases of heavy machinery, I’ll stick to the belief that lower fertilizer prices will lead to greater fertilizer sales and more revenue than current models might suggest.

Barclays (BCS) is emblematic of what US banks went through a few years ago. The European continent is coming to grips with the realization that greater capitalization of its banking system is needed. Barclays got punished twice last week. First for suggesting that it might initiate a secondary offering to raise cash and then actually releasing the news of an offering far larger than most had expected. Those bits of bad news may be good news for those that missed the very recent run from these same levels to nearly $20. Shares will also pay a modest dividend during the August 2013 option cycle, but not enough to chase shares just for the dividend.

Royal Dutch Shell (RDS.A) released its earnings this past Thursday and the market found nothing to commend. On the other hand the price drop was appealing to me, as it’s not every day that you see a 5% price drop in a company of this caliber. For your troubles it is also likely to be ex-dividend during the August 2013 option cycle. While there is still perhaps 8% downside to meet its 2 year low, I don’t think that will be terribly likely in the near term. Big oil has a way of thriving, especially if we’re at the brink of economic expansion.

Safeway (SWY) recently announced the divestiture of its Canadian holdings. As it did so shares surged wildly in the after hours. I remember that because it was one of the stocks that I was planning to recommend for the coming week and then thought that it was a missed opportunity. However, by the time the market opened the next morning most of the gains evaporated and its shares remained a Double Dip Dividend selection. While its shares are a bit higher than where I most recently had been assigned it still appears to be a good value proposition.

Baxter International (BAX) recently beat earnings estimates but wasn’t shown too much love from investors for its efforts. I look at it as an opportunity to repurchase shares at a price lower than I would have expected, although still higher than the $70 at which my most recent shares were assigned. In this case, with a dividend due early in September, I might consider a September 17, 2013 option contract, even though weekly and extended weekly options are available.

I currently own shares of Pfizer (PFE), Abbott Labs (ABT) and Eli Lilly (LLY) in addition to Merck (MRK), so I tread a little gingerly when considering adding either more shares of Merck or a new position in Bristol Myers Squibb (BMY), while I keep an eye of the need to remain diversified. Both of those, however, have traded well in their current price range and offer the kind of premium, dividend opportunity and liquidity that I like to see when considering covered call related purchases. As with Baxter, in the case of Merck I might consider selling September options because of the upcoming dividend.

Of course, to balance all of those wonderful healthcare related stocks, following its recent price weakness, I may be ready to add more shares of Lorillard (LO) which have recently shown some weakness. The last time its shares showed some weakness I decided to sell longer term call contracts that currently expire in September and also allow greater chance of also capturing a very healthy dividend. As with some other selections this month the September contract may have additional appeal due to the dividend and offers a way to collect a reasonable premium and perhaps some capital gains while counting the days.

Finally, Green Mountain Coffee Roasters (GMCR) is a repeat of last week’s earnings related selection. I did not sell puts in anticipation of the August 7, 2013 earnings report as I thought that I might, instead selecting Coach and Riverbed Technology (RVBD) as earnings related trades. Inexplicably, Green Mountain shares rose even higher during that past week, which would have been ideal in the event of a put sale.

However, it’s still not to late to look for a strike price that is beyond the 13% implied move and yet offers a meaningful premium. I think that “sweet spot” exists at the $62.50 strike level for the weekly put option. Even with a 20% drop the sale of puts at that level can return 1.1% for the week.

The announcement on Friday afternoon that the SEC was charging a former Green Mountain low level employee with insider trading violations was at least a nice cap to the week, especially if there’s a lot more to come.

Traditional Stocks: Barclays, Baxter International, Bristol Myers Squibb, Lorillard, Merck, Royal Dutch Shell, Safeway

Momentum Stocks: Coach, Mosaic

Double Dip Dividend: Barclays (ex-div 8/7)

Premiums Enhanced by Earnings: Green Mountain Coffee Roasters (8/7 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – July 28, 2013

Stocks need leadership, but it’s hard to be critical of a stock market that seems to hit new highs on a daily basis and that resists all logical reasons to do otherwise.

Stocks need leadership, but it’s hard to be critical of a stock market that seems to hit new highs on a daily basis and that resists all logical reasons to do otherwise.

That’s especially true if you’ve been convinced for the past 3 months that a correction was coming. If anything, the criticism should be directed a bit more internally.

What’s really difficult is deciding which is less rational. Sticking to failed beliefs despite the facts or the facts themselves.

In hindsight those who have called for a correction have instead stated that the market has been in a constant state of rotation so that correction has indeed come, but sector by sector, rather than in the market as a while.

Whatever. By which I don’t mean in an adolescent “whatever” sense, but rather “whatever it takes to convince others that you haven’t been wrong.”

Sometimes you’re just wrong or terribly out of synchrony with events. Even me.

What is somewhat striking, though, is that this incredible climb since 2009 has really only had a single market leader, but these days Apple (AAPL) can no longer lay claim to that honor. This most recent climb higher since November 2012 has often been referred to as the “least respected rally” ever, probably due to the fact that no one can point a finger at a catalyst other than the Federal Reserve. Besides, very few self-respecting capitalists would want to credit government intervention for all the good that has come their way in recent years, particularly as it was much of the unbridled pursuit of capitalism that left many bereft.

At some point it gets ridiculous as people seriously ask whether it can really be considered a rally of defensive stocks are leading the way higher. As if going higher on the basis of stocks like Proctor & Gamble (PG) was in some way analogous to a wad of hundred dollar bills with lots of white powder over it.

There have been other times when single stocks led entire markets. Hard to believe, but at one time it was Microsoft (MSFT) that led a market forward. In other eras the stocks were different. IBM (IBM), General Motors (GM) and others, but they were able to create confidence and optimism.

What you can say with some certainty is that it’s not going to be Amazon (AMZN), for example, as you could have made greater profit by shorting and covering 100 shares of Amazon as earnings were announced. than Amazon itself generated for the quarter. It won’t be Facebook (FB) either. despite perhaps having found the equivalent of the alchemist’s dream, by discovering a means to monetize mobile platforms.

Sure Visa (V) has had a remarkable run over the past few years but it creates nothing. It only facilitates what can end up being destructive consumer behavior.

As we sit at lofty market levels you do have to wonder what will maintain or better yet, propel us to even greater heights? It’s not likely to be the Federal Reserve and if we’re looking to earnings, we may be in for a disappointment, as the most recent round of reports have been revenue challenged.

I don’t know where that leadership will come from. If I knew, I wouldn’t continue looking for weekly opportunities. Perhaps those espousing the sector theory are on the right track, but for an individual investor married to a buy and hold portfolio that kind of sector rotational leadership won’t be very satisfying, especially if in the wrong sectors or not taking profits when it’s your sector’s turn to shine.

Teamwork is great, but what really inspires is leadership. We are at that point that we have come a long way without clear leadership and have a lot to lose.

So while awaiting someone to step up to the plate, maybe you can identify a potential leader from among this week’s list. As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories (see details).

ALthough last week marked the high point of earnings season, I was a little dismayed to see that a number of this week’s prospects still have earnings ahead of them.

While I have liked the stock, I haven’t always been a fan of Howard Schultz. Starbucks (SBUX) had an outstanding quarter and its share price responded. Unfortunately, I’ve missed the last 20 or so points. What did catch my interest, however, was the effusive manner in which Schultz described the Starbucks relationship with Green Mountain Coffee Roasters (GMCR). In the past shares of Green Mountain have suffered at the ambivalence of Schultz’s comments about that relationship. This time, however, he was glowing, calling it a “Fantastic relationship with Green Mountain and Brian Kelly (the new CEO)… and will only get stronger.”

Green Mountain reports earnings during the August 2013 option cycle. It is always a volatile trade and fraught with risk. Having in the past been on the long side during a 30% price decline after earnings and having the opportunity to discuss that on Bloomberg, makes it difficult to hide that fact. In considering potential earnings related trades, Green Mountain offers extended weekly options, so there are numerous possibilities with regard to finding a mix of premium and risk. Just be prepared to own shares if you opt to sell put options, which is the route that I would be most likely to pursue.

Deere (DE) has languished a bit lately and hasn’t fared well as it routinely is considered to have the same risk factors as other heavy machinery manufacturers, such as Caterpillar and Joy Global. Whether that’s warranted or not, it is their lot. Deere, lie the others, trades in a fairly narrow range and is approaching the low end of that range. It does report earnings prior to the end of the monthly option cycle, so those purchasing shares and counting on assignment of weekly options should be prepared for the possibility of holding shares through a period of increased risk.

Heading into this past Friday morning, I thought that there was a chance that I would be recommending all three of my “Evil Troika,” of Halliburton (HAL), British Petroleum (BP) and Transocean (RIG). Then came word that Halliburton had admitted destroying evidence in association with the Deepwater disaster, so obviously, in return shares went about 4% higher. WHat else would anyone have expected?

With that eliminated for now, as I prefer shares in the $43-44 range, I also eliminated British Petroleum which announces earnings this week. That was done mostly because I already have two lots of shares. But Transocean, which reports earnings the following week has had some very recent price weakness and is beginning to look like it’s at an appropriate price to add shares, at a time that Halliburton’s good share price fortunes didn’t extend to its evil partners.

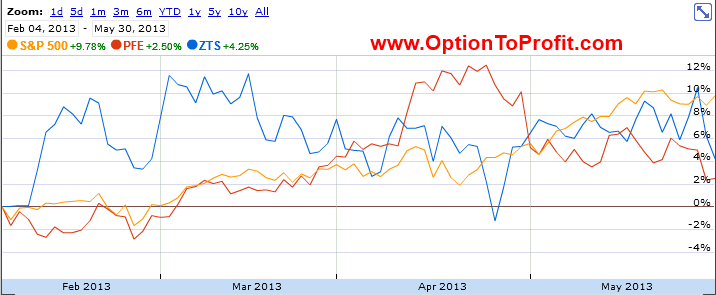

Pfizer (PFE) offers another example of situations I don’t particularly care for. That is the juxtaposition of earnings and ex-dividend date on the same or consecutive days. In the past, it’s precluded me from considering Men’s Warehouse (MW) and just last week Tyco (TYC). However, in this situation, I don’t have some of the concerns about share price being dramatically adversely influenced by earnings. Additionally, with the ex-dividend date coming the day after earnings, the more cautious investor can wait, particularly if anticipating a price drop. Pfizer’s pipeline is deep and its recent spin-off of its Zoetis (ZTS) division will reap benefits in the form of a de-facto massive share buyback.

My JC Penney (JCP) shares were assigned this past week, but as it clings to the $16 level it continues to offer an attractive premium for the perceived risk. In this case, earnings are reported August 16, 2013 and I believe that there will be significant upside surprise. Late on Friday afternoon came news that David Einhorn closed his JC Penney short position and that news sent shares higher, but still not too high to consider for a long position in advance of earnings.

Another consistently on my radar screen, but certainly requiring a great tolerance for risk is Abercrombie and Fitch (ANF). It was relatively stable this past week and it would have been a good time to have purchased shares and covered the position as done the previous week. While I always like to consider doing so, I would like to see some price deterioration prior to purchasing the next round of shares, especially as earning’s release looms in just two weeks.

Sticking to the fashion retail theme, L Brands (LTD) may be a new corporate name, but it retains all of the consistency that has been its hallmark for so long. It’s share price has been going higher of late, diminishing some of the appeal, but any small correction in advance of earnings coming during the current option cycle would put it back on my purchase list, particularly if approaching $52.50, but especially $50. Unfortunately, the path that the market has been taking has made those kind of retracements relatively uncommon.

In advance of earnings I sold Dow Chemical (DOW) puts last week. I was a little surprised that it didn’t go up as much as it’s cousin DuPont (DD), but finishing the week anywhere above $34 would have been a victory. Now, with earnings out of the way, it may simply be time to take ownership of shares. A good dividend, good option premiums and a fairly tight trading range have caused it to consistently be on my radar screen and a frequent purchase decision. It has been a great example of how a stock needn’t move very much in order to derive outsized profits.

MetLife (MET) is another of a long list of companies reporting earnings this week, but the options market isn’t anticipating a substantive move in either direction. Although it is near its 52 week high, which is always a precarious place to be, especially before earnings, while it may not lead entire markets higher, it certainly can follow them.

Finally, it’s Riverbed Technology (RVBD) time again. While I do already own shares and have done so very consistently for years, it soon reports earnings. Shares are currently trading at a near term high, although there is room to the upside. Riverbed Technology has had great leadership and employed a very rational strategy for expansion. For some reason they seem to have a hard time communicating that message, especially when giving their guidance in post-earnings conference calls. I very often expect significant price drops even though they have been very consistent in living up to analyst’s expectations. With shares at a near term high there is certainly room for a drop ahead if they play true to form. I’m very comfortable with ownership in the $15-16 range and may consider selling puts, perhaps even for a forward month.

Traditional Stocks: Deere, Dow Chemical, L Brands, MetLife, Transocean

Momentum Stocks: Abercrombie and Fitch, JC Penney

Double Dip Dividend: Pfizer (ex-div 7/31)

Premiums Enhanced by Earnings: Green Mountain Coffee Roasters (8/7 PM), Riverbed Technology (7/30 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – June 30, 2013

The hard part about looking for new positions this week is that memories are still fresh of barely a week ago when we got a glimpse of where prices could be.

The hard part about looking for new positions this week is that memories are still fresh of barely a week ago when we got a glimpse of where prices could be.

When it comes to short term memory the part that specializes in stock prices is still functioning and it doesn’t allow me to forget that the concept of lower does still exist.

The salivating that I recall doing a week ago was not related to the maladies that accompany my short term memory deficits. Instead it was due to the significantly lower share prices.

For the briefest of moments the market was down about 6% from its May 2013 high, but just as quickly those bargains disappeared.

I continue to beat a dead horse, that is that the behavior of our current market is eerily reminiscent of 2012. Certainly we saw the same kind of quick recovery from a quick, but relatively small drop last year.

What would be much more eerie is if following the recovery the market replicated the one meaningful correction for that year which came fresh off the hooves of the recovery.

I promise to make no more horse references.

Although, there is always that possibility that we are seeing a market reminiscent of 1982, except that a similar stimulus as seen in 1982 is either lacking or has neigh been identified yet. In that case the market just keeps going higher.

I listened to a trader today or was foaming at the mouth stating how our markets can only go higher from here. He based his opinion on “multiples” saying that our current market multiple is well below the 25 times we saw back when Soviet missiles were being pointed at us.

I’ll bet you that he misses “The Gipper,” but I’ll also bet that he didn’t consider the possibility that perhaps the 25 multiple was the irrational one and that perhaps our current market multiple is appropriate, maybe even over-valued.

But even if I continue to harbor thoughts of a lower moving market, there’s always got to be some life to be found. Maybe it’s just an involuntary twitch, but it doesn’t take much to raise hope.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend or Momentum categories. With earnings season set to begin July 8, 0213, there are only a handful of laggards reporting this coming week, none of which appear risk worthy (see details).

I wrote an article last week, Wintel for the Win, focusing on Intel (INTC) and Microsoft (MSFT). This week I’m again in a position to add more shares of Intel, as my most recent lots were assigned last week. Despite its price having gone up during the past week, I think that there is still more upside potential and even in a declining market it will continue to out-perform. While I rarely like to repurchase at higher prices, this is one position that warrants a little bit of chasing.

While Intel is finally positioning itself to make a move into mobile and tablets and ready to vanquish an entire new list of competitors, Texas Instruments (TXN) is a consistent performer. My only hesitancy would be related to earnings, which are scheduled to be announced on the first day of the August 2013 cycle. Texas Instruments has a habit of making large downward moves on earnings, as the market always seems to be disappointed. With the return of the availability of weekly options I may be more inclined to consider that route, although I may also consider the August options in order to capitalize somewhat on premiums enhanced by earnings anticipation.

Already owning shares of Pfizer (PFE) and Merck (MRK), I don’t often own more than one pharmaceutical company at a time. However, this week both Eli Lilly (LLY) and Abbott Labs (ABT) may join the portfolio. Their recent charts are similar, having shown some weakness, particularly in the case of Lilly. While Abbott carries some additional risk during the July 2013 option cycle because it will report earnings, it also will go ex-dividend during the cycle. However, Lilly’s larger share drop makes it more appealing to me if only considering a single purchase, although I might also consider selling an August 2013 option even though weekly contracts are available.

I always seem to find myself somewhat apologetic when considering a purchase of shares like Phillip Morris (PM). I learned to segregate business from personal considerations a long time ago, but I still have occasional qualms. But it is the continued ability of people to disregard that which is harmful that allows companies like Phillip Morris and Lorillard (LO), which I also currently own, to be the cockroaches of the market. They will survive any k

ind of calamity. It’s recent under-performance makes it an attractive addition to a portfolio, particularly if the market loses some ground, thereby encouraging all of those nervous smokers to sadly rekindle their habits.

The last time I purchased Walgreens (WAG) was one of the very few times in the past year or two that I didn’t immediately sell a call to cover the shares. Then, as now, shares took, what I believed to be an unwarranted large drop following the release of earnings, which I believed offered an opportunity to capture both capital gains and option premiums during a short course of share ownership. It looks as if that kind of opportunity has replicated itself after the most recent earnings release.

Among the sectors that took a little bit of a beating last week were the financials. The opportunity that I had been looking for to re-purchase shares of JP Morgan Chase (JPM) disappeared quickly and did so before I was ready to commit additional cash reserves stored up just for the occasion. While shares have recovered they are still below their recent highs. If JP Morgan was not going ex-dividend this trade shortened week, I don’t believe that I would be considering purchasing shares. However, it may offer an excellent opportunity to take advantage of some option pricing discrepancies.

I rarely use anecdotal experience as a reason to consider purchasing shares, but an upcoming ex-dividend date on Darden Restaurants (DRI) has me taking another look. I was recently in a “Seasons 52” restaurant, which was packed on a Saturday evening. I was surprised when I learned that it was owned by Darden. It was no Red Lobster. It was subsequently packed again on a Sunday evening. WHile clearly a small portion of Darden’s chains the volume of cars in their parking lots near my home is always impressive. While my channel check isn’t terribly scientific it’s recent share drop following earnings gives me reason to believe that much of the excess has already been removed from shares and that the downside risk is minimized enough for an entry at this level.

While I did consider purchasing shares of Conoco Phillips (COP) last week, I didn’t make that purchase. Instead, this week I’ve turned my attention back to its more volatile namesake, Phillips 66 (PSX) which it had spun off just a bit more than a year ago. It has been a stellar performer in that time, despite having fallen nearly 15% since its March high and 10% since the market’s own high. It fulfills my need to find those companies that have fared more poorly than the overall market but that have a demonstrated ability to withstand some short term adverse price movements.

Finally, I haven’t recommended the highly volatile silver ETN products for quite a while, even though I continue to trade them for my personal accounts. However, with the sustained movement of silver downward, I think it is time for the cycle to reverse, much as it had done earlier this year. The divergence between the performance of the two leveraged funds, ProShares UltraShort Silver ETN (ZSL) and the ProShares Ultra Silver ETN (AGQ) are as great as I have seen in recent years. I don’t think that divergence is sustainable an would consider either the sale of puts on AGQ or outright purchase of the shares and the sale of calls, but only for the very adventurous.

Traditional Stocks: Abbott Labs, Eli Lilly, Intel, Mosaic, Phillip Morris, Texas Instruments, Walgreens

Momentum Stocks: Phillips 66, ProShares UltraSilver ETN

Double Dip Dividend: Darden Restaurants (ex-div 7/8), JP Morgan (ex-div 7/2)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

A Final Thought About the Pfizer Tender Offer

In the weeks since Pfizer’s (PFE) announcement that it was offering the remainder of its 400+ million holding in Zoetis (ZTS) in exchange for Pfizer shares many opinions have been offered regarding the relative merits of the tender offer.

In the weeks since Pfizer’s (PFE) announcement that it was offering the remainder of its 400+ million holding in Zoetis (ZTS) in exchange for Pfizer shares many opinions have been offered regarding the relative merits of the tender offer.

My own opinion, previously cast some skepticism regarding what appeared to be a very favorable offer that might provide as much as a 7.52% premium for individuals offering their shares of Pfizer in exchange for Zoetis shares.

I did not offer my shares for tender, with the deadline for having done so, passing on Monday, June 17, 2013.

However, Pfizer has announced that its tender offer for exchange of its shares for Zoetis shares has been over-subscribed and that the offer has been automatically extended, as provided by the terms of the tender offer.

“The final exchange ratio is 0.9898 because the upper limit is in effect. Accordingly, the exchange offer has been automatically extended by its terms until 12:00 midnight, New York City time, on June 21, 2013”

That simple phrase means one very important thing for those that had believed a quick pay day by selling their new shares of Zoetis..

As explained in the prospectus, plainly in sight on the cover page, although the exchange premium was 7.52%, it was subject to an “upper limit” of 0.9898 shares of Zoetis for each share of Pfizer exchanged. The prospectus warned that the actual amount of in-kind value received could end up being substantially less if the “upper limit” was reached.

And it was.

At the conclusion of the initial phase of the tender offer, more than 800 million shares of Pfizer had been tendered for about 400 million shares of Zoetis.

That means that on a pro-rated basis an individual will have less than half of their tendered Pfizer shares accepted for exchange. The potential impact and costs associated with small share lots was discussed in my previous article that included the impact of transaction administrative fees that could wipe out any potential profit for those seeking to immediately sell shares in order to capitalize on any exchange premium.

While the final exchange rate is known, 0.9898 shares of Zoetis for each share of Pfizer tendered and accepted, it isn’t yet known what the pro-rated figure will be. In other words, what proportion of each 100 shares of Pfizer tendered will be accepted. It will likely be less than the current ratio. The greater the additional number of shares tendered the greater the adverse impact on small share holders.

For those still considering tendering shares, you have until midnight, Friday, June 22, 2013 to do so.

The following may be helpful:

At Zoetis’ current price of $30.19 after the close of trading on Thursday, June 20, 2013, each share of Pfizer that is accepted for tender will be worth $29.88, as compared to the Pfizer actual closing price of $28.64 on Thursday. That represents a 4.32% premium, which is substantially below the initial 7.52% premium.

Since the tender offer was made public Zoetis shares have subsequently fallen more on a percentage basis than have Pfizer shares and the premium has contracted. The Zoetis share price may or may not be maintained at that level when trading begins, so even that reduced premium may or may not be realized for those seeking to sell their new Zoetis shares.

For those that decide to accept the extended offer and had sold June 22, 2013 call options on their shares, you must be certain that your shares were not assigned. Strictly speaking, option contracts that expire at the end of a monthly cycle, do not expire until Saturday, which is after the extended deadline to tender shares.

If you accept the tender offer and your Pfizer shares were subsequently discovered to have been assigned you would still be obligated to deliver Pfizer shares in exchange for Zoetis shares and could do so by purchasing them in the after-market. That has additional risk if the price of Pfizer shares increase while the price of Zoetis shares decrease.

What to do?

Stick with Pfizer. If and when there is a time to own Zoetis shares you can always do so based on its own merits and without a clock ticking away in the background.

Picking a Winner in the Pfizer-Zoetis Divorce

Strictly speaking, Pfizer’s (PFE) decision to separate from Zoetis (ZTS) is called a spin-off.

Strictly speaking, Pfizer’s (PFE) decision to separate from Zoetis (ZTS) is called a spin-off.

It did so initially on February 1, 2013 and there was much excitement about the prospects of being able to invest in the pets and livestock healthcare business, which was being touted as that portion of Pfizer that had the greater growth potential and by inference the greatest likelihood of out-performing the market and certainly out-performing stodgy old Pfizer, itself.

Certainly, if you are able to remember back to the heady days of Pfizer when Viagra was brought to an eager consumer demographic, there isn’t much reason to believe that sort of growth is in Pfizer’s future. From every logical point of view the best way to unlock shareholder value was to unleash hidden gems that were buried inside of a behemoth.

Additionally, if you look at the recent experience of the spin off by Conoco Phillips (COP) of its refiner arm, Phillips 66 (PSX) you might be of the belief that such spin-offs are akin to a license to print money.

By now Pfizer shareholders may have received the offer to exchange shares of Pfizer for Zoetis. With consummation of this offer, the separation of the two entities will be complete.

Pfizer refers to it as an “exchange offer to separate the Zoetis animal health business from Pfizer’s bio-pharmaceutical businesses in a tax-efficient manner, thereby enhancing stockholder value and better positioning Pfizer to focus on its core bio-pharmaceutical business.”I call that a divorce.

In some situations, I suppose that the children of divorce could see themselves as winners, particularly if they are able to leverage their parents against one another, but that sort of thing may be more common in situational comedies than in real life.

Perhaps shareholders of Pfizer see themselves as winners, as well, although, Zoetis shareholders may have a very different view of melding families.

On the surface, the offer looks very attractive. In a nutshell Pfizer shareholders are being given the opportunity to exchange $100 worth of their Pfizer shares for approximately $107.52 of Zoetis shares.

When in a red hot stock market, that kind of exchange is actually more than just appealing. Where else can you get a 7.52% return from one minute to the next?

For me, the decision isn’t quite so straightforward, as I have sold Pfizer calls with an expiration of June 22, 2013, while the deadline to respond to the offer is on June 17, 2013. There is no mechanism in the option market, particularly for contracts that may be exercised to identify those Pfizer shares that have been offered for tender.

There may, in fact, be some liability if, having sold calls and accepted the tender offer, the shares are subsequently assigned as a result of option exercise. That would be potentially onerous, especially if Zoetis shares were to go on a run higher, but I’m not overly concerned about that occurring.

But forget about me and my problems, or the problems of an option buyer. For the ordinary buy and hold investor the decision should be a fairly easy one to make.

Right?

Well not so fast.

For starters, the likelihood of being able to exchange all of your shares is small. There are over 7 billion shares of Pfizer and only about 400 million shares of Zoetis being offered. That’s good enough reason to inform shareholders that the exchange may be made on a pro-rata basis. Unlike a Facebook (FB) IPO offering you’re not likely to get more shares than you imagined.

Incidentally, about 75% of Pfizer’s shares are institutionally owned. The greatest likelihood is that those holdings are in excess of 100 shares per institution, but more on that later.

Assuming that everyone in the world salivates at the prospect of that 7.52% premium and the ability to cash in by selling shares of Zoetis, there are a number of considerations before counting your profits.

Among those considerations is that institutions, which currently only own approximately 18% of Zoetis shares, would be more facile in being able to unload shares quickly, as they are freely transferable upon exchange. That 7.52% premium may not be destined to withstand a lack of buyers, even if some discipline existed and there was an attempt to create orderly selling.

With the differential in the number of shares between the two companies, assuming that all shares were tendered, each shareholder would receive an allocation of about 6% of their request.

Before you get exp

osed to too much math, you should also know that there is a $30 fee to exchange shares. As with all investing transactions, there is an economy achieved in volume, especially when there’s a fixed price involved.

In the event that someone holds 100 shares of Pfizer, approximately 6 of those would be eligible for exchange, based on the assumption that all outstanding Pfizer shares would be offered for tender. The final number of shares of Zoetis received in exchange for Pfizer shares will be based upon an exchange rate as determined by the 3 day weighted closing price as announced on June 19, 2013, or after, if the deadline is extended by Pfizer.

For illustrative purposes, let’s assume the final Pfizer share price was $29. That would entitle the shareholder to $31.18 worth of Zoetis shares.

Your 6 share allocation would mean a profit on the exchange of $13.08, less the $30 transaction fee, leaving you with a loss of nearly $17.

That is an example of snatching defeat from the jaws of victory.

Of course if less than all shares are tendered the 100 share stock owner would fare better. If only 3 billion shares are offered for exchange he would break even.

Or would he?

The next part of the equation is what happens to Zoetis. At the moment the float is approximately 500 million shares, which will increase from one moment to the next to 900 million shares.

Then comes the real fun as there will certainly be those looking to quickly capitalize on that 7.52% differential before the opportunity disappears.

One can only imagine that would put some downward pressure on share price, which incidentally hasn’t fared terribly well since the initial spin-off.

Zoetis became a publicly traded company in a successful IPO, having been priced above expectations and closing up 19% on its first day of trading, from an IPO price of $26. Unlike Phillips 66, however, it hasn’t left its parent in the dust.

In fact, despite an early positive showing, Zoetis has lagged Pfizer in its performance, while both have trailed the S&P 500.

In fact, despite an early positive showing, Zoetis has lagged Pfizer in its performance, while both have trailed the S&P 500.

As with many stocks that hold the promise of growth, Zoetis doesn’t offer a terribly appealing dividend, although that could change as it has already been increased for Phillips 66. Currently the Zoetis yield is 0.8%. Compare that to the stodgy Pfizer that is yielding 3.4%

Ultimately. in terms of the offer itself, the fewer that express an interest, the far better the offer would likely be as allocations would be increased and pricing pressure on Zoetis would be decreased.

A classic battle of greed versus common sense.

As an inveterate option seller, I have an additional consideration. Zoetis does offer option contracts, but unlike Pfizer it does not offer weekly contracts, nor does it have a multitude of unit denominated strike prices, making the prospects of holding shares less attractive for me.

With a bit more than two weeks until a decision is required my initial reaction to the offer has undergone quite a transformation, but I’ll still end up following the numbers and determining whether some additional return can be squeezed out of the transaction owing to the size of my Pfizer position

While I now anticipate the possibility of continuing to hold onto my Pfizer shares, I do hope that perhaps someone who hasn’t given the subject too much thought may end up exercising their $29 option early, at a price below the strike, as they may perceive Pfizer priced at anything greater than $27 to be the equivalent of Zoetis priced at $29 and hope to make a killing in what they believe to be an arbitrage opportunity.

Maybe divorce isn’t that bad? At least if you don’t think about it too much.

Weekend Update – May 19, 2013

Shades of 1999.

I’m not certain that I understand the chorus of those claiming that our current market reminds them of 1999.

Mind you, I’m as cautious, maybe much more so than the next guy and have been awaiting some kind of a correction for more than 2 months now, but I just don’t see the resemblance.

Much has also been made of the fact that the S&P 500 is now some 12% above its 200 Day Moving Average, which in the past has been an untenable position, other than back when sock puppets were ruling the markets. Back then that metric was breached for years.

Back in 1999 and the years preceding it, the catalyst was known as the “dot com boom” or “dot com bubble” or the “dot com bust,” depending on what point you entered. The catalyst was clear, perhaps best exemplified by the ubiquitous sock puppet and the short lived PSINet Stadium, back then home to the world Champion Baltimore Ravens. The Ravens survived, perhaps even thrived since then, while PSINet was a casualty of the excesses of the era. When it was all said and done you could stuff PSINet’s assets into a sock.

During the height of that era the catalyst was thought to be in endless supply. But in the current market, what is the catalyst? Most would agree that if anything could be identified it would likely be the Federal Reserve’s policy of Quantitative Easing.

But as last week’s rumor of its upcoming end and then an article suggesting that the Federal Reserve already has an exit plan, the catalyst is clearly not thought to be unending. Unless the economy is much worse than we all believe it to be the fuel will be depleted sooner rather than later.

Now if you’re really trying to find a year comparable to this one, look no further than 1995, when the market ended the year 34% higher and never even had anything more than a 2% correction.

If llke me, and you’re selling covered options; let’s hope not.

For me, this Friday marked the end of the May 2013 option cycle. As I had been cautious since the end of February and transitioned into more monthly option contract sales, I am faced with a large number of assignments. Considering that the market has essentially been following a straight line higher having so many assignments isn’t the best of all worlds.

While I now find myself with lots of available cash the prevailing feeling that I have is that there is a need to protect those assets more than before in anticipation of some kind of correction, or at least an opportunity to discover some temporary bargains.

This week I have more than the usual number of potential new positions, however, I’m unlikely to commit wholeheartedly to their purchase, as I would like to maintain about a 40% cash position by the end of next week. I’m also more likely to continue looking at monthly option sales rather than the weekly contracts.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details). Additionally, although the height of earnings season has passed there may still be some more opportunity to sell well out of the money puts prior to earnings on some reasonably high profile names..

There’s no doubt that the tone for the week was changed by the down to earth utterances of David Tepper, founder of the Appaloosa Hedge Fund. He has a long term enviable record and when he speaks, which isn’t often, people do take notice. Apparently markets do, as well.

However, among the things that he mentioned was that he had lightened up on his position in Apple (AAPL). It didn’t take long for others to chime in and Apple shares fell substantially even when the market was going higher. Although I was waiting for Apple to get back into the $410-420 range, the rebound in share price following news of reduced positions by high profile investors is a good sign and I believe warrants consideration toward the purchase of new shares.

I recently purchased shares of Sunoco Logistics (SXL) in order to capture its generous and reliable dividend. My shares were assigned this past Friday, but I’m willing to repurchase, even at a higher price and even with a monthly option contract to tie me down. In the oil services business it is a lesser known entity and trades with low volume, however, it will share in sector strength, just in a much more low profile manner.

Pfizer (PFE) is another stock that was recently purchased in order to capture it’s dividend and premium and was also assigned this past week. However, it is among the “defensive” stocks that I think would fare relatively well regardless of near term market direction. Like many others that do offer weekly options, my inclination is to consider the selling monthly contracts for the time being.

While healthcare has certainly already had its time in the sun in 2013 and Bristol Myers Squibb (BMY) has had its share of that glory, after some recent tumult in its price and most recently its next day reversal of a strong move the previous day, I find the option premium appealing. However, as opposed to Pfizer, which I’m more inclined to consider a monthly option, Bristol Myers has too much downside potential for me to want to commit for longer periods.

Although I already own shares of Petrobras (PBR) and am not a big fan of adding additional shares after such a strong climb hig

her off of its rapidly achieved lows, Petrobras recently and quietly had quite an achievement. WHile everyone was talking about Apple’s $17 Billion bond offering that had about $50 Billion in bids, Petrobras just closed an $11 Billion offering with more than $40 Billion in bids.

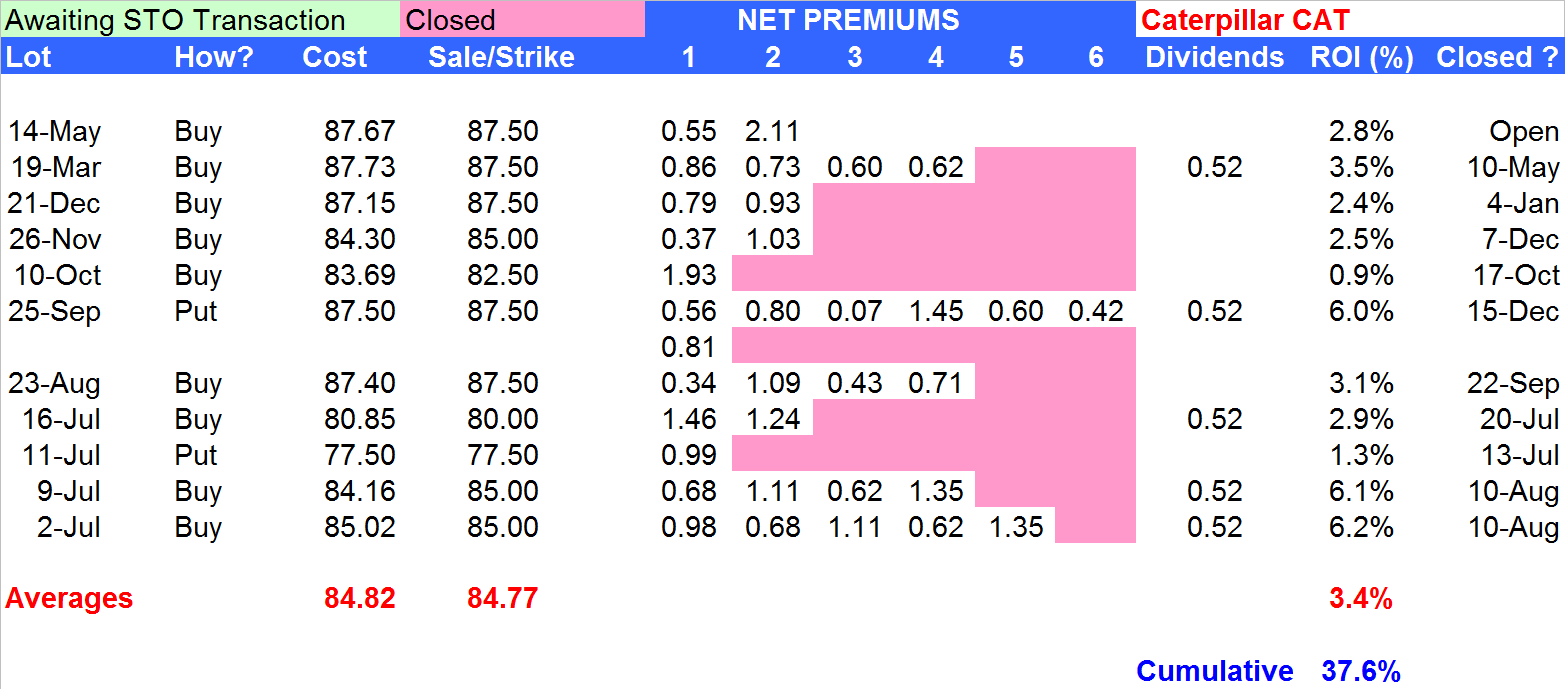

Caterpillar (CAT), which I also currently own, is a perennial member of my portfolio. To a very large degree it has been recently held hostage to rumors of contraction and slowing in the Chinese economy. It has, however, shown great resiliency at the current price level and has been an excellent vehicle upon which to sell call options.

As shown in the table above, I’ve owned shares of Caterpillar on 11 separate occasions in less than a year. While the price has barely moved in that period, the net result of the in and out trades, as a result of share assignments has been a gain in excess of 35%.

As shown in the table above, I’ve owned shares of Caterpillar on 11 separate occasions in less than a year. While the price has barely moved in that period, the net result of the in and out trades, as a result of share assignments has been a gain in excess of 35%.

The more ambiguity and equivocation there is in understanding the direction of the Chinese economy the better it has been to own Caterpillar as it just bounces around in a fairly well defined price range, making it an ideal situation for covered call strategies.

Continuing the theme of shares that I currently own, but am considering adding more shares, is British Petroleum (BP). With much of its Deepwater Horizon liabilities either behind it or well defined, shares appear to have a floor. However, in the past year, that has already been the case, as my experience with British Petroleum ownership has paralleled that of Caterpillar in both the number of separate times owning shares and in return – only better.

Of course, better than either Caterpillar or British Petroleum has been Chesapeake Energy (CHK). I’ve owned it 18 times in a year. It too has had much of its liability removed as Aubrey McClendon has left the scene and it is already well known that Chesapeake will be selling assets under a degree of duress. With its turnaround on Thursday and dip below $20, I am ready to add even more shares.

I’ve probably not owned Conoco Phillips (COP) as much as I would have imagined over the past year probably As a result of owning British Petroleum and Chesapeake Energy so often. Shares do go ex-dividend this week which always adds to the appeal, particularly when I’m in a defensive mode.

Salesforce.com (CRM) was a recommendation last week. I did make that purchase and subsequently had shares assigned. This week it reports earnings and as many of the earnings related trades that I prefer, it offers what I believe to be a good option premium even in the event of a large downward move. In this case a 1% return for the week may be achieved if share price doesn’t exceed 8%

Sears Holdings (SHLD) always seems like a ghost town when I enter one of its stores, although perhaps a moment of introspection would indicate that I drive shoppers away. I’m aware of other story lines revolving around Sears and its real estate holdings, but tend not to think in terms of what has been playing out a s a very, very long term potential. Instead, I like Sears as a hopefully quick earnings trade.

In a week that saw beautiful price action from Macys (M), Kohls (KSS) and others, perhaps even Sears can pull out good numbers and even provide some positive guidance. However, what appeals to me is a put sale approximately 8% below Friday’s close that could offer a 4% ROI for the month or shorter.

Another retailer, The Gap (GPS), has certainly been an example of the ability to arise from the ashes and how a brand can be revitalized. Along with it, so too can its share price. The Gap reports earnings this week and has already had an impressive price run. As opposed to most other earnings related trades, I’m not looking for a significant downward move and the market isn’t expecting such a move either. Based on some of the strong retail earnings announced this past week I think The Gap may be an outright purchase, but I would be more likely to look at a weekly option sale and hope for quick assignment of shares.

TIVO (TIVO) is one of those technologies that I’ve never adopted. Maybe that’s because I never leave the house and the television is always on and I rarely see a need to change the station. But here, too, I believe TIVO offers a good short term opportunity even if shares go down as much as 20% following Monday’s earnings release. In the event that shares go appreciably higher, it is the ideal kind of earnings trade, in that coming during the first day of a monthly option contract, it could likely be quickly closed out and the money then used for another investment vehicle.

Om the other hand, Dunkin Brands (DNKN) is definitely one of those technologies that I’ve adopted, especially when having lived in New England. Fast forward 20 years and they are now everywhere in the Mid-Atlantic and spreading across the country as their new offerings also spread waists around the country. Going ex-dividend this coming week and offering a nice monthly option premium, I may bite at more than a jelly donut. However, it is trading at the upper end of its recent price range, like all too many other stocks.

Finally, Carnival (CCL) hasn’t exactly been the recipient of much good news lately. Although it’s up from its recent woes and lows. It does report earnings at the end of the June 2013 option cycle, but it also goes ex-dividend in the first week of the cycle, in addition to a offering a reasonable option premium

Traditional Stocks: Bristol Myers, Caterpillar, Pfizer, Sunoco Logistics

Momentum Stocks: Apple, Chesapeake Energy, Petrobras

Double Dip Dividend: Carnival Line (ex-div 5/22), Conoco Phillips (ex-div 5/22), Dunkin Brands (ex-div 5/23)

Premiums Enhanced by Earnings: Salesforce.com (5/23 PM), Sears Holdings (5/23 AM), The Gap (5/23 PM), TIVO (5/20 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – May 5, 2013

ADP. ISM. FOMC. ECB

ADP. ISM. FOMC. ECB

They came one after another at us last week. Not to mention the Jobless Report and the Employment Situation Reports to end the week.

Following the previous week where I had temporarily gone on one of my wild and drunken spending ways buying new shares with assignment proceeds, I returned to a more cautious note this past week.

Maybe it was the soup. While I have much greater comfort when on a shopping spree, usually borne out of a bullish view of the world, this week even the comfort food was sending me some kind of misleading message, spoonful after spoonful. I don’t always listen to my soup, but when I do, I know that things are serious. This week’s message wasn’t exactly cryptic in nature. For certain, the message wasn’t “Buy, Buy, Buy.”

But to simply assume the message is correct is bordering on lunacy, so I just decided not to buy quite as much, proving that we can all get along. Besides, “sell, sell, sell,” seemed so draconian.

Although so often a drastically sharp move downward comes from unexpected or lightly regarded catalysts, there’s not too much of an excuse to overlook some potentially obvious catalysts when the market appears to be in an overbought condition. For me, already sensitized to a possible drop, the FOMC, ECB and Employment Situation were individually capable of initiating and speeding a sudden descent.

Aligned? Had the Federal Reserve given a strong hint of an end to Quantitative Easing, had they suggested an earlier timetable for interest rate hikes, or had the European Central Bank not lowered rates that combination had the makings of a nasty punch. Throw a second successive month of disappointing employment numbers, perhaps with downward revisions of previous months and now you’ve got a party.

For short sellers, at least.

While the market did have a slightly delayed reaction to the FOMC minutes, it was fairly mute, despite doubling the early losses. The following day, which is often the day the real action occurs after an FOMC meeting, had its tone already set earlier by the ECB decision to drop rates.

That just left Friday, with a little hint from Wednesday’s release of the ADP statistics. that job growth may be slowing due to some headwinds in the economy. Much of the talk on Wednesday was how fearful everyone was that the number on Friday would be terribly negative.

The fact that the number was, in fact, an indication of a growing economy and there were massive upward revisions to earlier months was the surprise that should never have been a surprise, as thesis changing revisions are routine.

So all of the important letters were aligned, as no one really cares about ISM, and there was reason for a party. The order of the day on Friday was “buy, buy, buy,” once again delaying the “Sell in May” crowd’s ascent and giving me cause to reflect as the majority of my monthly covered call positions are now in the money and do not stand to further profit in the event of a continued market rise.

Of course, if I wanted to continue the lunacy, I would simply rationalize it all and convince myself that I now have a nice cushion between share and strike prices to withstand a fall between now and May 18, 2013. Sooner or later my call for a significant market drop will have to take on broken clock qualities.

Yet, the rationalizations aren’t working. Maybe I need another spoonful of soup.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend or Momentum categories, with no selections in the “PEE” category, despite earnings season still going strong (see details). Additionally, this week the emphasis is once again on dividend paying stocks and still giving greater consideration to monthly contracts, in order to lock into option premiums for a longer period in order to ride out any pauses in the runaway train. Of course, after Friday’s run higher capping off a week when the S&P 500 moved 2% higher, good luck finding any bargain priced shares. Bargains may be justifiably so. Sometimes there’s a reason no one asks you to dance. You just refuse to look in the mirror, justifiably so.

I jumped the gun a bit on Friday afternoon and purchased shares of Pfizer (PFE). After a very impressive share run higher, which hasn’t really occurred in the post-Viagra era, Pfizer reported earnings last week and continued the weakness that immediately preceded the report, after some European regulatory disappointments. A case of too much and too fast from my perspective, but the shares appear as a reasonably low risk over the coming weeks, particularly with a safe and healthy dividend and an upcoming ex-dividend date this week.

Wells Fargo (WFC) has been a frequent purchase target. While I do like shares, it along with so many others is more expensive than I would like. However, it has proven resilient in defending its share price when tested and the test levels have been slowly climbing higher. That’s certainly a more healthy way to see appreciation and I think offers less risk in what may become a risky environment. Additionally, their new ad campaign, “At least we’re not JP Morgan” (JPM) speaks volumes with regard to superfluous risk. As often before, my entry point is not so coincidentally synchronized with an ex-dividend date.

Weyerhauser (WY) is not a stock that I buy very often, but in hindsight I wonder why. Not because it does anything spectacular, but rather because it is so unspectacular that it has the core requirements of being an ideal covered call stock. It generally trades in a narrow range, has an options premium that is more than symbolic and pays a competitive dividend. What’s not to like, especially this week as it also goes ex-dividend.

Although I don’t have any “PEE” selections this week, Marathon Oil (MRO) does report earnings on May 7, 2013. However, unlike the usual earnings related plays that I prefer, it isn’t expected to trade in a wide range after the announcement. It’s implied move is far less than the 10% or greater that I usually look for while still offering a 1% ROI. Instead, it’s just like any other stock that happens to be reporting earnings, except that it’s approximately 5% off of its recent high, satisfying another of the criteria I look for when considering the risk associated with trading around earnings season.

I already own shares of St. Jude Medical (STJ) at a price slightly higher than Friday’s close. I rarely think about adding additional shares unless the price has had a significant drop. However, St. Judes Medical has had a fall relative to the market and certainly to the heath care sector. I don’t envision it as being at undue risk in the event of a market downturn, due to its modest existence during the upturn.

Parker Hannefin (PH) and W.W. Grainger (GWW) both go ex-dividend this week. Although their share rise on Friday adds to some reluctance to add them to the portfolio next week, if the Employment Situation statistics and the revisions are any guide, there may be very good reason to suspect that industrials and the companies that support the industrials may be ready for a little bit of a resurgence. Neither offer incredibly exciting dividends, but share appreciation may be more a part of the equation than it is for most stocks that I consider due to their option and dividend income potential.

I’ve been looking for a re-entry point in Goldman Sachs (GS) for a while. Again, hindsight told me that may have been a couple of weeks ago as shares were a relative bargain. The fact that shares have greatly under-performed the S&P 500 over the past 12 weeks has appeal for me, as I believe it marks a company that may be better equipped to out-perform going forward, particularly in a downturn.

Finally, Abercrombie and FItch (ANF) is an always exciting stock to own, especially as earnings are approaching. In this case earnings aren’t expected until May 15, 2013, so there is a little bit of breathing space to consider shares before the added volatility kicks in. When it moves, the moves are spectacular and certainly the option premiums reflect that kind of risk. My bias at the moment is that if an opportunity will arise it will likely take the form of put sales. However, that is only something that I would do if emotionally prepared to hold shares going into earnings if assigned. If so, a bit of luck may be necessary to turn the tables and sell call contracts going into earnings or sell additional puts if you’re really adventurous.

Traditional Stocks: Goldman Sachs, Marathon Oil, St. Jude Medical

Momentum Stocks: Abercrombie and Fitch

Double Dip Dividend: W.W. Grainger (ex-div 5/9), Parker-Hannefin (ex-div 5/8), Pfizer (ex-div 5/8), Wells Fargo (ex-div 5/8), Weyerhauser (ex-div 5/8)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – April 28, 2013

Schadenfreude suits me just fine.

Schadenfreude suits me just fine.

Is it really “schadefreude” when you don’t really know or see the people upon whom misfortune has been heaped?

For those that aren’t familiar with the word, “schadenfreude” is the strangely good feeling that some people derive when others fail or are subject to misfortune.

In Talmudic teaching the highest form of charity is when neither the donor nor the recipient are aware of one another’s identity. Complete ignorance raises the act of charity to a higher level.

Of course, we will never be able to answer the question of whether there is really a sound produced when a tree falls in the forest and there is no one present to lay witness. A single degree of separation can completely call into question that which seems patently obvious. Ignorance of an event can be is as if it doesn’t even exist.