With the S&P 500 having reached an all time high this past week you could certainly draw the conclusion that a government shutdown is a good thing and flirting with default is a constructive strategy. At a reported cost of only $24 Billion associated with closure and nothing more than a symbolic “Fitch slap” credit watch issued, perhaps we should look forward to the next potential round in just a few months.

With the S&P 500 having reached an all time high this past week you could certainly draw the conclusion that a government shutdown is a good thing and flirting with default is a constructive strategy. At a reported cost of only $24 Billion associated with closure and nothing more than a symbolic “Fitch slap” credit watch issued, perhaps we should look forward to the next potential round in just a few months.

For me, this past week marked the slowest week of opening new positions that I can recall since the 2009 market bottom. Although history suggests that the eleventh hour is a charm, the zeal of some more newly elected officials was reminiscent of a theological premise that believes in order to save it you must first destroy the world. That kind of uncertainty is the kind in which you get your affairs in order rather than embarking on lots of new and exciting initiatives.

With manufactured uncertainty temporarily removed the market can focus on earnings and other things that most of us believe are somewhat important.

One thing that will be certain is that wherever possible the next earnings season will attempt to lay some blame for any disappointments upon the government shutdown. This past week it certainly didn’t take Stanley Black and Decker (SWK) and eBay (EBAY) very long to already take advantage of that excuse. Who knew that government purchasing agents were unable to use eBay for Blackhawk helicopter replacement parts during their unexpected furlough?

As with the previous earnings season the financial sector started off the reports in a promising way, although early in the season the results are mixed, with some significant surges and plunges. What is clear is that investors are paying particular attention to guidance.

One earnings report that caught my attention was from Pet Smart (PETM). My father always believed that no matter what the economic environment, people would always find the wherewithal to spend on the pets and their kids. Pet Smart’s disappointing earnings focused on a “challenged consumer” and lower customer traffic. That can’t be a good sign. If pets are going wanting what does that portend for the rest of us?

Yet, on the other hand, Align Technology (ALGN) discussed last week, was a different story. Certainly representing discretionary spending and not benefiting from any provisions in the Affordable Care Act, their orthodontic appliances see no barriers from the economy ahead, as they reported great earnings and guidance.

Also clouding the picture, perhaps both literally and figuratively, is the positive guidance provided by Peabody Energy (BTU). For a nation that has been said to “move on coal,” that has to be a signal of something positive going forward.

This week, with lots of cash from assignments of October 2013 option contracts, I’m anxious to get back to business as usual, but still have a bit of wariness. However, despite the appearances of a reluctant consumer, I’m encouraged by recent activity in the speculative portion of my portfoli0, enough so to consider adding to those positions, even at market highs.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

The news from Peabody Energy in addition to some recent price stabilization in Walter Energy (WLT), Cliffs Natural Resources (CLF) and Freeport McMoRan (FCX) have me in a hopeful mood after long having suffered with positions in all three.

A year ago at this time I believed that Freeport McMoRan would be among the best performers in 2013, but subsequent to that it has only recently started on its recovery from the price plunge it sustained when announcing plans to acquire Plains Exploration and Production, as it planned to expand its asset base to include oil and natural gas. While the long term vision may be someday vindicated, 2013 has not been a stellar year. But, like some others this week, there has been a steady strengthening in its price, despite significantly lower gold, oil and copper prices, year to date. While its dividend has made holding shares marginally tolerable through the year, I think it is now ready to start a sustained climb and it offers appealing call premiums to create income or provide downside protection. Earnings are reported this week, but the option market is not expecting a very large move.

Another company slowly climbing higher, but still with a great distance to travel is Walter Energy . In addition to suffering through a proxy fight this year and significant challenges to management, declining coal prices and a slashed dividend, I believe that it is also poised to continue climb higher. I recently tested the waters and added shares along with selling in the money calls. Those were just assigned, but I think that I’m ready to dip deeper.

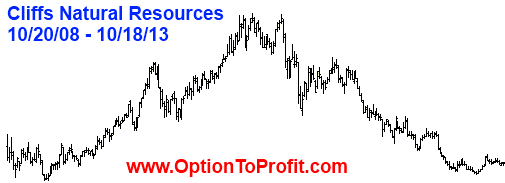

Sticking to the same theme, Cliffs Natural Resources goes hand in hand with Walter Energy, at least in its price behavior and disappointments. I

t too has slashed its dividend and its CEO has retired. Like Walter Energy, I recently started adding shares and had them assigned this week. Cliffs reports earnings this week and unlike Freeport McMoRan, the option market is expecting a larger price move.

While I rarely do more than glance at charts, in the case of Cliffs Natural Resources the 5 Year price chart may suggest a long term pattern that has shares at the beginning of a sustained climb higher.

While I rarely do more than glance at charts, in the case of Cliffs Natural Resources the 5 Year price chart may suggest a long term pattern that has shares at the beginning of a sustained climb higher.

As with many positions that are preparing to report earnings, I typically consider potential entry through the sale of put options.

Also reporting earnings this week is Cree (CREE). Thanks to legislation its LED light bulbs have become ubiquitous in home improvement stores and homes. It has the features of companies that make potentially alluring earnings trades. In this case, this always volatile moving company can sustain up to a 14% price decline and still return a 1% ROI for the week. The only real consideration is that it is capable of making that decline a reality, so if selling puts you do have to be prepared to take ownership.

While already having reported earnings and falling into the “disappointing” category, Fastenal (FAST), which I look at as being an economic barometer kind of company has already started regaining its price decline. It will be ex-dividend this week offering an additional reason to consider its purchase, even though I already own lower priced shares and rarely buy additional lots at higher prices. However, with W.W. Grainger (GWW) recently reporting positive earnings I’m encouraged that Fastenal will follow, but in the meantime the dividend and option premium make it easier to wait.

Also going ex-dividend this week is Williams-Sonoma (WSM). I considered its purchase last week, but it fell victim to a week of my inaction. While perhaps at risk to suffer from decreased spending at some higher end stores it has already fallen about 11% from its recent high point. However, since it reports earnings just prior to the expiration of the November 2013 option cycle, I might consider utilizing a December 2013 covered call sale.

The Gap (GPS) isn’t at risk of losing too many high end customers, it has just been losing customers, at least on the basis of its most recent monthly report. It is one of those retailers that still reports monthly comparison figures. That’s just one more bullet that needs to be dodged in addition to potential surprises during earnings season. Shares went precipitously lower with its most recent retail report and caught me along with it. It is near a price support level and represents an opportunity to either purchase additional shares to attempt to offset paper losses of an earlier lot or to establish an initial covered position.

While eBay may not sell used Blackhawk helicopter parts it somehow found a way to link its coming fortunes to the government shutdown. Suffering a significant price drop following earnings and guidance shares were once again in a channel of great familiarity. Having traded reliably in the $50-$52.50 range the sight of it falling was well received. However, late in the trading session on Friday someone else must have seen the same appeal as shares suddenly jumped $1.65 in about 20 minutes. That takes away some of the appeal. What takes away more of the appeal was the explanation by CEO Donahoe that spurred the surge, when he explained that he and his CFO did not mean to sound so dour about holiday prospects, it’s just that they both had colds.

On the other hand UnitedHealth Group (UNH) is a company that may be able to justifiably point its finger at the Federal government when it reports earnings again in January 2014. Already suffering a nearly 10% drop in the past week related to 2014 guidance, UnitedHealth is a major player in the options available on the Affordable Health Care Act exchanges. While perhaps not being able to blame the shutdown for any revenue related woes, disappointing enrollment statistics may be in the making. The additional price drop on Friday, following the large drop on Thursday may be related to enrollment challenges rather than projections of lower Medicare funding in the coming year. However, nearing a price support and following such a large price drop provides a combination that makes ownership appealing. Perhaps eBay employees should consider signing up en masse in the event they are all prone to colds that effect their ability to perform. In enough numbers that may be helpful to UnitedHealth Group’s 2014 revenues.

Of course, while the market seemed to rejoice at what could only be construed as the return to health of the eBay executives, Groupon (GRPN) is another example of a stock whose price has returned to more lofty levels following surgical removal of its CEO. It is one of a handful of stocks that I sold last year taking a capital loss and swore that I would never buy again. Now down about 15% from its recent high, which itself was up approximately 500% from its not too distant low, Groupon is a different company in leadership, product and prospects. While still a risky position

Finally, a name that everyone seems to disparage these days is Coach (COH). While there is certainly sufficient reason to believe that retailers, even the higher end retailers are being challenged, Coach is beginning to be perceived as taking a back seat to retailer Michael Kors (KORS). SHares have certainly been volatile, especially at earnings and Coach reports earnings this week. Having owned shares a number of times in the past year, my preference is to sell puts in advance of earnings in anticipation of a large drop. Currently, the option market is implying nearly a 9% move. A 1% ROI for the week can be obtained through such a sale if the price drop is less than 12%.

Traditional Stocks: eBay, The Gap, United Health Group

Momentum Stocks: Groupon, Walter Energy

Double Dip Dividend: Fastenal (ex-div 10/23), Williams Sonoma (ex-div 10/23)

Premiums Enhanced by Earnings: Coach (10/22 AM), Freeport McMoRan (10/22), Cree (10/22 PM), Cliffs Natural Resources (10/24 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.