![]() Everything is crystal clear now.

Everything is crystal clear now.

After three straight weeks of losses to end the trading week, including deep losses the past two weeks everyone was scratching their heads to recall the last time a single month had fared so poorly.

What those mounting losses accomplished was to create a clear vision of what awaited investors as the past week was to begin.

Instead, it was nice to finish on an up note to everyone’s confusion.

When you think you are seeing things most clearly is when you should begin having doubts.

Who saw a two day 350 point gain coming, unless they had bothered to realize that this week was featuring an Employment Situation Report? The one saving grace we have is that for the past 18 months you could count on a market rally to greet the employment news, regardless of whether the news met, exceeded or fell short of expectations.

That’s clarity. It’s confusing, but it’s a rare sense of clarity that comes from being so successful in its ability to predict an outcome that itself is based upon human behavior.

As the week began with a 325 point loss in the DJIA voices started bypassing talk of a 10% correction and starting uttering thoughts of a 15-20% correction. 10% was a bygone conclusion. At that point most everyone agreed that it was very clear that we were finally being faced with the “healthy” correction that had been so long overdue.

When in the middle of that correction nothing really feels very healthy about it, but when people have such certainty about things it’s hard to imagine that they might be wrong. With further downside seen by the best and brightest we were about to get healthier than our portfolios might be able to withstand.

It was absolutely amazing how clearly everyone was able to see the future. What made things even more ominous and sustaining their view was the impending Employment Situation Report due at the end of the week. Following last month’s abysmal numbers, ostensibly related to horrid weather across the country, there wasn’t too much reason to expect much in the way of an improvement this time around. Besides, the Nikkei and Russian stock markets had just dipped below the 10% threshold that many define as a market correction and as we’re continually reminded, it’s an inter-connected world these days. It wasn’t really a question of “whether,” it was a matter of “when?”

Then there was all that talk of how high the volatility was getting, even though it had a hard time even getting to October 2013 levels, much less matching historical heights. As everyone knows, volatility comes along with declining markets so the cycle was being put in place for the only outcome possible.

After Monday’s close the future was clear. Crystal clear.

Instead, the week ended with an 0.8% gain in the S&P 500 despite that plunge on Monday and a highly significant drop in volatility. The market responded to a disappointing Employment Situation Report with what logically or even using the “good news is bad news” kind of logic should not have been the case.

Now, with a week that started by confirming the road to correction we were left with a week that supported the idea that the market is resistant to a classic correction. Instead of the near term future of the markets being crystal clear we are left beginning this coming week with more confusion than is normally the case.

If it’s true that the market needs clarity in order to propel forward this shouldn’t be the week to commit yourself. However, the only thing that’s really clear about our notions is that they’re often without basis so the only reasonable advice is to do as in all weeks – look for situational opportunities that can be exploited without regard to what is going on in the rest of the world.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories this week (see details).

If you’re looking for certainty, or at least a company that has taken steps to diminish uncertainty, Microsoft (MSFT) is the one. With the announcement of the appointment of Satya Nadella, an insider, to be its new CEO, shares did exactly what the experts said it wouldn’t do. Not too long ago the overwhelming consensus was that the appointment of an outsider, such as Alan Mullaly would drive shares forward, while an insider would send shares tumbling into the 20s.

Microsoft simply stayed on its path with the news of an inside candidate taking the reigns. Regardless of its critics, Microsoft’s strategy is more coherent than it gets credit for and this leadership decision was a quantum leap forward, certainly far more important than discussions of screen size. With this level of certainty also comes the certainty of a dividend and attractive option premiums, making Microsoft a perennial favorite in a covered option strategy.

The antithesis of certainty may be found in the smallest of the sectors. With the tumult in pricing and contracts being promulgated by T-Mobile (TMUS) and its rebel CEO John Legere, there’s no doubt that the margins of all wireless providers is being threatened. Verizon (VZ) has already seen its share price make an initial response to those threats and has shown resilience even in the face of a declining market, as well. Although the next ex-dividend date is still relatively far away, there is a reason this is a favorite among buy and hold investors. As long as it continues to trade in a defined range, this is a position that I wouldn’t mind holding for a while and collecting option premiums and the occasional dividend.

Lowes (LOW) is always considered an also ran in the home improvement business and some recent disappointing home sales news has trickled down to Lowes’ shares. While it does report earnings during the first week of the March 2014 option cycle, I think there is some near term opportunity at it’s current lower price to see some share appreciation in addition to collecting premiums. However, I wouldn’t mind being out of my current shares prior to its scheduled earnings report.

Among those going ex-dividend this week are Conoco Phillips (COP), International Paper (IP) and Eli Lilly (LLY). In the past month I’ve owned all three concurrently and would be willing to do so again. While International Paper has outperformed the S&P 500 since the most recent market decline two weeks ago, it has also traded fairly rangebound over the past year and is now at the mid-point of that range. That makes it at a reasonable entry point.

Conoco Phillips appears to be at a good entry point simply by virtue of a nearly 12% decline from its recent high point which includes a 5% drop since the market’s own decline. With earnings out of the way, particularly as they have been somewhat disappointing for big oil and with an end in sight for the weather that has interfered with operations, shares are poised for recovery. The premiums and dividend make it easier to wait.

Eli Lilly is down about 5% from its recent high and I believe is the next due for its turn at a little run higher as the major pharmaceutical companies often alternate with one another. With Pfizer (PFE) and Merck (MRK) having recently taken those honors, it’s time for Eli Lilly to get back in the short term lead, as it is for recent also ran Bristol Myers Squibb (BMY) that was lost to assignment this past week and needs a replacement, preferably one offering a dividend.

Zillow (Z) reports earnings this week. In its short history as a publicly traded company it has had the ability to consistently beat analyst’s estimates and then usually see shares fall as earnings were released. That kind of doubled barrel consistency warrants some consideration this week as the option market is implying an 11% move this week. While that is possible, there is still an opportunity to generate a 1% ROI for the week if the share price falls by anything less than 16%.

While I’m not entirely comfortable looking for volatility among potential new positions two that do have some appeal are Coach (COH) and Morgan Stanley (MS).

Coach is a frequent candidate for consideration and I generally like it more when it’s being maligned. After last week’s blow-out earnings report by Michael Kors (KORS) the obvious next thought becomes how their earnings are coming at the expense of Coach. While there may be truth to that and has been the conventional wisdom for nearly 2 years, Coach has been able to find a very comfortable trading range and has been able to significantly increase its dividend in each of the past 4 years in time for the second quarter distribution. It’s combination of premiums, dividends and price stability, despite occasional swings, makes it worthy of consistent consideration.

I’ve been waiting for a while for another opportunity to add shares of Morgan Stanley. Down nearly 12% in the past 3 weeks may be the right opportunity, particularly as some European stability may be at hand following the European Central Bank’s decision to continue accommodation and provide some stimulus to the continent, where Morgan Stanley has interests, particularly being subject to “net counterparty exposure.” It’s ride higher has been sustained and for those looking at such things, it’s lows have been consistently higher and higher, making it a technician’s delight. I don’t really know about such things and charts certainly aren’t known for their clarity being validated, but its option premiums do compel me as do thoughts of a dividend increase that it i increasingly in position to institute.

Finally, if you’re looking for certainty you don’t have to look any further than at Chesapeake Energy (CHK) which announced a significant decrease in upcoming capital expenditures, which sent shares tumbling on the announcement. Presumably, it takes money to make money in the gas drilling business so the news wasn’t taken very well by investors. A very significant increase in option premiums early in the week suggested that some significant news was expected and it certainly came, with some residual uncertainty remaining in this week’s premiums. For those with some daring this may represent the first challenge since the days of Aubrey McClendon and may also represent an opportunity for shareholder Carl Icahn to enter the equation in a more activist manner.

Traditional Stocks: Lowes, Microsoft, Verizon

Momentum Stocks: Chesapeake Energy, Coach, Morgan Stanley,

Double Dip Dividend: Conoco Phillips (ex-div 2/13), International Paper (ex-div 2/12), Eli Lilly (ex-div 2/12)

Premiums Enhanced by Earnings: Zillow (2/12 PM)

Remember, these are just guidelines for the coming week. The above selections may become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The overriding objective is to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – September 1, 2013

Behind every “old wives’ tale” there has to be a kernel of truth. That’s part of the basis for it being handed down from one generation to the next.

Behind every “old wives’ tale” there has to be a kernel of truth. That’s part of the basis for it being handed down from one generation to the next.

While I don’t necessarily believe that the souls of dead children reside in toads or frogs, who knows? The Pets.com sock puppet was real enough for people to believe in it for a while. No one got hurt holding onto that belief.

The old saw “Sell in May and go away,” has its origins in a simpler time. Back when The Catskills were the Hamptons and international crises didn’t occur in regular doses. There wasn’t much reason to leave your money in the stock market and watch its value predictably erode under the hot summer sun back in the old days.

Lately, some of those old wives’ tales have lost their luster, but the Summer of 2013 has been pretty much like the old days. With only a bare minimum of economic news and that part of the world that could impact upon our stock market taking a summer break, it has been an idyllic kind of season. In fact, with the market essentially flat from Memorial Day to Labor Day it was an ideal time to sell covered options.

So you would think that Syria could have at least waited just another week until the official end to the summer season, before releasing chemical weapons on its own citizens and crossing that “red line,” that apparently has meaning other than when sunburn begins and ends.

Or does it?

On Monday, Secretary of State John Kerry made it clear where the United States believed that blame lay. He used a kind of passion and emotion that was completely absent during his own Presidential campaign. Had he found that tone back in 2004 he might be among that small cadre of “President Emeritus” members today. On Friday he did more of the same and sought to remove uncertainty from the equation.

Strangely, while Kerry’s initial words and intent earlier in the week seemed to have been very clear, the market, which so often snaps to judgment and had been in abeyance awaiting his delayed presentation, didn’t know what to do for nearly 15 minutes. In fact, there was a slightly positive reaction at first and then someone realized the potentially market adverse meaning of armed intervention.

Finally, someone came to the realization that any form of warfare may not be a market positive. Although selling only lasted a single day, attempts to rally the markets subsequently all faded into the close as a variant on another old saying – “don’t stay long going into the weekend,” seemed to be at play.

That’s especially true during a long weekend and then even more true if it’s a long weekend filled with uncertainty. As it becomes less clear what our response will be, paradoxically that uncertainty has led to some calm. But at some point you can be assured that there will be a chorus of those questioning President Obama’s judgment and subsequent actions and wondering “what would Steve Jobs have done.”

John Kerry helped to somewhat answer that question on Friday afternoon and the market ultimately settled on interpreting the message as being calming, even though the message implied forceful action. What was clear in watching the tape is that algorithms were not in agreement over the meaning of the word “heinous.”

With the market having largely gone higher for the past 20 months the old saying seeking to protect against uncertainty during market closures has been largely ignored during that time.

But now with uncertainty back in the air and the summer season having come to its expected end, it is back to business as usual.

That means that fundamentals, such as the way in which earnings have ruled the market this past summer take a back seat to “events du jour” and the avalanche of economic reports whose relevance is often measured in nano-seconds and readily supplanted by the next bit of information to have its embargo lifted.

This coming week is one of great uncertainty. I made fewer than the usual number of trades last week and if i was the kind that would be prone to expressing regret over some of them, I would do so. I expect to be even more cautious this week, unless there is meaningful clarity introduced into the equation. While wishing for business as usual, that may not be enough for it to become reality.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend and , Momentum categories, with no suitable “PEE” selections this week (see details).

While I currently own more expensive shares of Caterpillar (CAT), I almost always feel as if it’s a good time to add shares. Caterpillar has become everyone’s favorite stock to disparage, reaching its peak with famed short seller Jim Chanos’ presentation at the “Delivering Alpha Conference” a few weeks ago. as long as it continues trading in a $80-$90 range it is a wonderful stock for a covered call writing strategy and it has reliably stayed in that range.

Joy Global (JOY) reported its earnings last week and beat analysts estimates and reaffirmed its 2014 guidance. Nonetheless it was brutalized in the aftermath. Although already owning shares I took the opportunity to sell weekly put options in the belief that the reaction was well overdone.

If the reports of an improving Chinese economy are to be believed, and that may be a real test of faith, then Joy Global stands to do well. Like Caterpillar, it has traded in a reasonably narrow range and is especially attractive in the $48-53 neighborhood.

eBay (EBAY) is simply on sale, closing the week just below the $50 level. With no news to detract from its sh

are price and having traded very well in the $50 -53 range, it’s hard to justify why it fell along with other stocks in the uncertainty that attended the concerns over Syria. It’s certainly hard to draw a straight line from Syria related fears to diminished earnings at eBay.

By the recent measure that I have been using, that is the comparison to the S&P 500 performance since May 21, 2013, the market top that preceded a small post-Ben Bernanke induced correction, eBay has well underperformed the index and may be relatively immune from short term market pressure.

Baxter International (BAX) is one of those stocks that I like to own and am sad to see get assigned away from me. Every job has its negative side and while most of the time I’m happy seeing shares assigned, sometimes when it takes too long for them to return to a reasonable price, I get forlorn. In this case, timing is very serendipitous, because Baxter has fallen in price and goes ex-dividend this week.

Coach (COH) also goes ex-dividend this week and that increases its appeal. At a time when retail has been sending very mixed messages, and at a time when Coach’s position at the luxury end is being questioned as Michael Kors (KORS) is everyone’s new darling, COach is yet another example of a stock that trades very well in a specific range and has been very well suited to covered option portfolios.

In general, I’ve picked the wrong year to be bullish on metals and some of my patience is beginning to wear thin, but I’ve been seeing signs of some stability recently, although once again, the risk of putting too much faith into a Chinese recovery may carry a steep price. BHP Billiton (BHP) is the behemoth that all others bow to and may soon receive the same kind of fear and respect from the potash industry, as it is a prime reason the cartel has lost some of its integrity. BHP Billiton also goes ex-dividend this week and is now about 6% below its recent price spurt higher.

Seagate Technology (STX) isn’t necessarily for the faint of heart. but it is down nearly 20% from its recent high, at a time when there is re-affirmation that the personal computer won’t be disappearing anytime soon. While many of the stocks on my radar screen this week have demonstrated strength within trading ranges, Seagate can’t necessarily lay claim to the same ability and you do have to be mindful of paroxysms of movement which could take shares down to the $32 level.

While Seagate Technology may offer the thrills that some people need and the reward that some people want, Walgreen (WAG) may be a happy compromise. A low beta stock with an option premium that is rewarding enough for most. Although Walgreen has only slightly under-performed the S&P 500 since May 21st, I think it’s a good choice now, given potential immunity from the specific extrinsic issues at hand, particularly if you are under-invested in the healthcare sector.

Another area in which I’m under-invested is in the Finance sector. While it hasn’t under-performed the S&P 500 recently, Bank of New York Mellon (BK) is still about 7% lower in the past 5 weeks and offers a little less of a thrill in ownership than some of my other favorites, JP Morgan Chase (JPM) and Morgan Stanley (MS). Sometimes, it’s alright giving up on the thrills, particularly in return for a competitive option premium and the ability to sleep a bit sounder at night.

Finally, with the excitement about Steve Ballmer finally leaving Microsoft (MSFT) after what seems like an eternity of such calls, the share price has simply returned to a more inviting re-entry levels. In fact, when Ballmer announced his decision to leave the CEO position in 12 months, I did something that I rarely do. I bought back my call options at a loss and then sold shares at the enhanced share price. Occasionally you see a shares appreciation outstrip the appreciation in the in the money premium and opportunities are created to take advantage of the excitement not being reflected in future price expectations.

At the post-Ballmer excitement stage there is still reason to consider share ownership, including the anticipation of another dividend increase and option premiums while awaiting assignment of shares

Traditional Stocks: Bank of New York Mellon, Caterpillar, eBay, Microsoft, Walgreen

Momentum Stocks: Joy Global, Seagate Technology

Double Dip Dividend: Baxter International (ex-div 9/4), BHP Billiton (ex-div 9/4), Coach (ex-div 9/5)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may be become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The over-riding objective is to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – August 11, 2013

I like to end each week taking a look at the upcoming week’s economic calendar just to have an idea of what kind of curveballs may come along. It’s a fairly low value added activity as once you know what is in store for the coming week the best you can do is guess about data releases and then further guess about market reactions.

I like to end each week taking a look at the upcoming week’s economic calendar just to have an idea of what kind of curveballs may come along. It’s a fairly low value added activity as once you know what is in store for the coming week the best you can do is guess about data releases and then further guess about market reactions.

Just like the professionals.

That’s an even less productive endeavor in August and this summer we don’t even have much in the way of extrinsic factors, such as a European banking crisis to keep us occupied in our guessing. In all, there have been very few catalysts and distractions of late, hearkening back to more simple times when basic rules actually ruled.

In the vacuum that is August you might believe that markets would be inclined to respond to good old fundamentals as histrionics takes a vacation. Traditionally, that would mean that earnings take center stage and that the reverse psychology kind of thinking that attempts to interpret good news as bad and bad news as good also takes a break.

Based upon this most recent earnings season it’s hard to say that the market has fully embraced traditional drivers, however. While analysts are mixed in their overall assessment of earnings and their quality, what is clear is that earnings don’t appear to be reflective of an improving economy, despite official economic data that may be suggesting that is our direction.

That, of course, might lead you to believe that discordant earnings would put price pressure on a market that has seemingly been defying gravity.

Other than a brief and shallow three day drop this week and a very quickly corrected drop in May, the market has been incredibly resistant to broadly interpreting earnings related news negatively, although individual stocks may bear the burden of disappointing earnings, especially after steep runs higher.

But who knows, maybe Friday’s sell off, which itself is counter to the typical Friday pattern of late is a return to rational thought processes.

Despite mounting pessimism in the wake of what was being treated as an unprecedented three days lower, the market was able to find catalysts, albeit of questionable veracity, on Thursday.

First, news of better than expected economic growth in China was just the thing to reverse course on the fourth day. For me, whose 2013 thesis was predicated on better than expected Chinese growth resulting from new political leadership’s need to placate an increasingly restive and entitled society, that kind of news was long overdue, but nowhere near enough to erase some punishing declines in the likes of Cliffs Natural Resources (CLF).

That catalyst lasted for all of an hour.

The real surprising catalyst at 11:56 AM was news that JC Penney (JCP) was on the verge of bringing legendary retail maven Allen Questrom back home at the urging of a newly vocal Bill Ackman. The market, which had gone negative and was sinking lower turned around coincident with that news. Bill Ackman helped to raise share price by being Bill Ackman.

Strange catalyst, but it is August, after all. In a world where sharks can fall out of the sky why couldn’t JC Penney exert its influence, especially as we’re told how volatile markets can be in a light volume environment? Of course that bump only lasted about a day as shares went down because Bill Ackman acted like Bill Ackman.The ensuing dysfunction evident on Friday and price reversal in shares was, perhaps coincidentally mirrored in the overall market, as there really was no other news to account for any movement of stature.

With earnings season nearly done and most high profile companies having reported, there’s very little ahead, just more light volume days. As a covered option investor if I could script a market my preference would actually be for precisely the kind of market we have recently been seeing. The lack of commitment in either direction or the meandering around a narrow range is absolutely ideal, especially utilizing short term contracts. That kind of market present throughout 2011 and for a large part of 2012 has largely been missing this year and sorely missed. Beyond that, a drop on Fridays makes bargains potentially available on Mondays when cash from assigned positions is available.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend and Momentum, with no “PEE” selections this week. (see details).

For an extended period I’ve been attempting to select new positions that were soon to go ex-dividend as a means to increase income, offset lower option premiums and reduce risk, while waiting for a market decline that has never arrived.

This week, I’m more focused on the two selections that are going ex-dividend this coming week, but may have gotten away after large price rises on Thursday.

Both Cliffs Natural Resources and Microsoft (MSFT) were beneficiaries of Chinese related ne

ws. In Cliffs Natural’s case it was simply the perception that better economic news from China would translate into the need for iron ore. In Microsoft’s case is was the introduction of Microsoft Office 365 in China. Unfortunately, both stocks advanced mightily on the news, but any pullback prior to the ex-dividend dates would encourage me to add shares, even in highly volatile Cliffs, with which I have suffered since the dividend was slashed.

A bit more reliable in terms of dividend payments are Walgreens (WAG), Chevron (CVX) and Phillips 66 (PSX).

Although I do like Walgreens, I’ve only owned it infrequently. However, since beginning to offer weekly options I look more frequently to the possibility of adding shares. Despite being near its high, the prospect of a short term trade in a sector that has been middling over the past week, with a return amplified by a dividend payment, is appealing.

Despite being near the limit of the amount of exposure that I would ordinarily want in the Energy Sector, both Chevron and Phillips 66 offer good option premiums and dividends. The recent weakness in big oil makes me gravitate toward one of its members, Chevron, however, if forced to choose between just one to add to my portfolio, I prefer Phillips 66 due to its greater volatility and enhanced premiums. I currently own Phillips 66 shares but have them covered with September call contracts. In the event that I add shares I would likely elect weekly hedge contracts.

If there is some validity to the idea that the Chinese economy still has some life left in it, Joy Global (JOY), which is currently trading near the bottom of its range offers an opportunity to thrive along with the economy. Although the sector has been relatively battered compared to the overall market, option premiums and dividends have helped to close that gap and I believe that the sector is beginning to resemble a compressed spring. On a day when Deere (DE) received a downgrade and Caterpillar was unable to extend its gain from the previous day, Joy Global moved strongly higher on Friday in an otherwise weak market.

Oracle (ORCL) is one of the few remaining to have yet reported its earnings and there will be lots of anticipation and perhaps frayed nerves in advanced for next month’s report, which occurs the day prior to expiration of the September 2013 contract.

You probably don’t need the arrows in the graph above to know when those past two earnings reports occurred. Based Larry Ellison’s reaction and finger pointing the performance issues were unique to Oracle and one could reasonably expect that internal changes have been made and in place long enough to show their mark.

Fastenal (FAST) is just a great reflection of what is really going on in the economy, as it supplies all of those little things that go into big things. Without passing judgment on which direction the economy is heading, Fastenal has recently seemed to established a lower boundary on its trading range after having reported some disappointing earnings and guidance. Trading within a defined range makes it a very good candidate to consider for a covered option strategy

What’s a week without another concern about legal proceedings or an SEC investigation into the antics over at JP Morgan Chase (JPM)? While John Gotti may have been known as the “Teflon Don,” eventually after enough was thrown at him some things began to stick. I don’t know if the same fate will befall Jamie Dimon, but he has certainly had a well challenged Teflon shell. Certainly one never knows to what degree stock price will be adversely impacted, but I look at the most recent challenge as just an opportunity to purchase shares for short term ownership at a lower price than would have been available without any legal overhangs.

Morgan Stanley (MS), while trading near its multi-year high and said to have greater European exposure than other US banks, continues to move forward, periodically successfully testing its price support.

With any price weakness in JP Morgan or Morgan Stanley to open the week I would be inclined to add both, as I’ve been woefully under-invested in the Finance sector recently.

While retailers, especially teen retailers had a rough week last week, Footlocker (FL) has been a steady performer over the past year. A downgrade by Goldman Sachs (GS) on Friday was all the impetus I needed and actually purchased shares on Friday, jumping the gun a bit.

Using the lens of a covered option seller a narrow range can be far more rewarding than the typical swings seen among so many stocks that lead to evaporation of paper gains and too many instances of buying high and selling low. Some pricing pressure was placed on shares as its new CEO was rumored a potential candidate for the CEO at JC Penney. However, as that soap opera heats up, with the board re-affirming its support of their one time CEO and now interim CEO, I suspect that after still being in limbo over poaching Martha Stewart products, JC Penney will not likely further go where it’s unwelcome.

Finally, Mosaic (M

OS) had a good week after having plunged the prior week, caught up in the news that the potash cartel was falling apart. Estimates that potash prices may fall by 25% caused an immediate price drop that offered opportunity as basically the fear generated was based on supposition and convenient disregard for existing contracts and the potential for more rationale explorations of self-interest that would best be found by keeping the cartel intact.

The price drop in Mosaic was reminiscent of that seen by McGraw Hill FInancial (MHFI) when it was announced that it was the target of government legal proceedings for its role in the housing crisis through its bond ratings. The drop was precipitous, but the climb back wonderfully steady.

I subsequently had Mosaic shares assigned in the past two weeks, but continue to hold far more expensively priced shares. I believe that the initial reaction was so over-blown that even with this past week’s move higher there is still more ahead, or at least some price stability, making covered options a good way to generate return and in my case help to whittle down paper losses on the older positions while awaiting some return to normalcy.

Traditional Stocks: Fastenal, Footlocker, JP Morgan, Morgan Stanley, Oracle

Momentum Stocks: Joy Global, Mosaic

Double Dip Dividend: Chevron (ex-div 8/15), Phillips 66 (ex-div 8/14), Walgreen (ex-div 8/16)

Premiums Enhanced by Earnings: none

Remember, these are just guidelines for the coming week. The above selections may be become actionable, most often coupling a share purchase with call option sales or the sale of covered put contracts, in adjustment to and consideration of market movements. The over-riding objective is to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – July 7, 2013

Much has been made of the recent increase in volatility.

Much has been made of the recent increase in volatility.

As someone who sells options I like volatility because it typically results in higher option premiums. Since selling an option provides a time defined period I don’t get particularly excited when seeing large movements in a share’s price. With volatility comes greater probability that “this too shall pass” and selling that option allows you to sit back a bit and watch to see the story unwind.

It also gives you an opportunity to watch “the smart money” at play and wonder “just how smart is that “smart money”?

But being a observer doesn’t stop me from wondering sometimes what is behind a sudden and large movement in a stock’s price, particularly since so often they seem to occur in the absence of news. They can’t all be “fat finger ” related. I also sit and marvel about entire market reversals and wildly alternating interpretations of data.

I’m certain that for a sub-set there is some sort of technical barrier that’s been breached and the computer algorithms go into high gear. but for others the cause may be less clear, but no doubt, it is “The Smart Money,” that’s behind the gyrations so often seen.

Certainly for a large cap stock and one trading with considerable volume, you can’t credit or blame the individual investor for price swings, especially in the absence of news. Since for those shares the majority are owned by institutions, which hopefully are managed by those that comprise the “smart money” community, the large movements certainly most result in detriment to at least some in that community.

But what especially intrigues me is how the smart money so often over-reacts to news, yet still can retain their moniker.

This week’s announcement that there would be a one year delay in implementing a specific component of the Affordable Care Act , the Employer mandate, resulted in a swift drop among health care stocks, including pharmaceutical companies.

Presumably, since the markets are said to discount events 6 months into the future, the timing may have been just right, as a July 3, 2013 announcement falls within that 6 month time frame, as the changes were due to begin January 1, 2014.

By some kind of logic the news of the delay, which reflects a piece of legislation that has regularly alternated between being considered good and bad for health care stocks, was now again considered bad.

But only for a short time.

As so often is seen, such as when major economic data is released, there is an immediate reaction that is frequently reversed. Why in the world would smart people have knee jerk reactions? That doesn’t seem so smart. This morning’s reaction to the Employment Situation report is yet another example of an outsized initial reaction in the futures market that saw its follow through in the stock market severely eroded. Of course, the reaction to the over-reaction was itself then eroded as the market was entering into its final hour, as if involved in a game of volleyball piting two team of smart money against one another.

Some smart money must have lost some money during that brief period of time as they mis-read the market’s assessment of the meaning of a nearly 200,000 monthly increase in employment.

After having gone to my high school’s 25th Reunion a number of years ago, it seemed that the ones who thought they were the most cool turned out to be the least. Maybe smart money isn’t much different. Definitely be wary of anyone that refers to themselves as being part of the smart money crowd.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or “PEE” categories. (see details).

As a caveat, with Earnings Season beginning this week some of the selections may also be reporting their own earnings shortly, perhaps even during the July 2013 option cycle. That knowledge should be factored into any decision process, particularly since if you select a shorter term option sale that doesn’t get assigned, since yo may be left with a position that is subject to earnings related risk. By the same token, some of those positions will have their premiums enhanced by the uncertainty associated with earnings.

Both Eli Lilly (LLY) and Abbott Labs (ABT) were on my list of prospective purchases last week. Besides being a trading shortened week in celebration of the FOurth of July, it was also a trade shortened week, as I initiated the fewest new weekly positions in a few years. Both shares were among those that took swift hits from fears that a delay in the ACA would adversely impact companies in the sector. In hindsight, that was a good opportunity to buy shares, particularly as they recovered significantly later in the day. Lilly is well off of its recent highs and Abbott Labs goes ex-dividend this week. However, it does report earnings during the final week of the July 2013 option cycle. I think that healthcare stocks have further to run.

AIG (AIG) is probably the stock that I’ve most often thought of buying over the past two years but have too infrequently gone that path. While at one time I thought of it only as a speculative position it is about as mainstream as they come, these days. Under the leadership of Robert Ben Mosche it has accomplished what no one believe was possible with regard to paying back the Treasury. While its option premiums aren’t as exciting as they once were it still offers a good risk-reward proposition.

Despite having given up on “buy and hold,” I’ve almost always had shares of Dow Chemical (DOW) over the past 5 years. They just haven’t been the same shares f

or very long. It’s CEO, Andrew Liveris was once the darling of cable finance news and then fell out of favor, while being roundly criticized as Dow shares plummeted in 2008. His star is pretty shiny once again and he has been a consistent force in leading the company to maintain shares trading in a fairly defined channel. That is an ideal kind of stock for a covered call strategy.

The recent rise in oil prices and the worries regarding oil transport through the Suez Canal, hasn’t pushed British Petroleum (BP) shares higher, perhaps due to some soon to be completed North Sea pipeline maintenance. British Petroleum is also a company that I almost always own, currently owning two higher priced lots. Generally, three lots is my maximum for any single stock, but at this level I think that shares are a worthy purchase. With a dividend yield currently in excess of 5% it does make it easier to make the purchase or to add shares to existing lots.

General Electric (GE) is one of those stocks that I only like to purchase right after a large price drop or right before its ex-dividend date. Even if either of those are present, I also like to see it trading right near its strike price. Its big price drop actually came 3 weeks ago, as did its ex-dividend date. Although it is currently trading near a strike price, that may be sufficient for me to consider making the purchase, hopeful of very quick assignment, as earnings are reported July 19, 2013.

Oracle (ORCL) has had its share of disappointments since the past two earnings releases. Its problems appear to have been company specific as competitors didn’t share in sales woes. The recent announcement of collaborations with Microsoft (MSFT and Salesforce.com (CRM) says that a fiercely competitive Larry Ellison puts performance and profits ahead of personal feelings. That’s probably a good thing if you believe that emotion can sometimes not be very helpful. It too was a recent selection that went unrequited. Going ex-dividend this week helps to make a purchase decision easier.

This coming week and next have lots of earnings coming from the financial sector. Having recently owned JP Morgan Chase (JPM) and Morgan Stanley (MS) I think I will stay away from those this week. While I’ve been looking for new entry points for Citigroup (C) and Bank of America (BAC), I think that they’re may be a bit too volatile at the moment. One that has gotten my attention is Bank of New York Mellon (BK). While it does report earnings on July 17, 2013 it isn’t quite as volatile as the latter two banks and hasn’t risen as much as Wells Fargo (WFC), another position that I would like to re-establish.

YUM Brands (YUM) reports earnings this week and as an added enticement also goes ex-dividend on the same day. People have been talking about the risk in its shares for the past year, as it’s said to be closely tied to the Chinese economy and then also subject to health scare rumors and realities. Shares do often move significantly, especially when they are stoked by fears, but YUM has shown incredible resilience, as perhaps some of the 80% institutional ownership second guess their initial urge to head for the exits, while the “not so smart money” just keeps the faith.

Finally, one place that the “smart money” has me intrigued is JC Penney (JCP). With a large vote of confidence from George Soros, a fellow Hungarian, it’s hard to not wonder what it is that he sees in the company, after all, he was smart enough to have fled Hungary. The fact that I already own shares, but at a higher price, is conveniently irrelevant in thinking that Soros is smart to like JC Penney. In hindsight it may turn out that ex-CEO Ron Johnson’s strategy was well conceived and under the guidance of a CEO with operational experience will blossom. I think that by the time earnings are reported just prior to the end of the August 2013 option cycle, there will be some upward surprises.

Traditional Stocks: Bank of New York, British Petroleum, Dow Chemical, Eli Lilly, General Electric,

Momentum Stocks: AIG, JC Penney

Double Dip Dividend: Abbott Labs (ex-div 7/11), Oracle (ex-div)7/10)

Premiums Enhanced by Earnings: YUM Brands (7/10 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as act

ionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – May 26, 2013

That was the crash, dummy.

That was the crash, dummy.

“I’ll know it when I see it,” is a common refrain when you’re at a loss for just the right descriptors or just can’t quite define what it is that should be obvious to everyone.

While there are definitions for what constitutes a recession, for example, an individual may have a very good sense of personally being in one before anyone else recognizes or confirms its existence.

Certainly there’s also a distinction between a depression and a recession, but it’s not really necessary to know the details, because you’ll probably know when you’ve transitioned from one to another.

The same is probably true when thinking about the difference between a market crash and a market correction. While people may not agree on a standard definition of what constitutes either, a look at your own portfolio balance can be all the definition that you need.

I’ve been waiting, even hoping for a correction for over two months now. That hoping came to a crescendo as a covered option writer with the expiration of many May 2013 contracts and finding more cash than I would have liked faced with the aspects of either being re-invested at a top or sitting idly.

Then came Federal Reserve Chairman Ben Bernanke’s congressional testimony and the mixed signals people perceived. Was it tapering or not tapering? Was it now or later?

What came as a result was what some called a “Key Reversal Day.” That is a day when the market reaches new highs and then suddenly reverses to go even lower than the previous day’s low. It’s thought that the greater the range of movement and the greater the trading volume the more reliable of an indicator is the reversal,

On both counts the aftermath of the reaction to Bernanke’s words, or as the “Bond King” Bill Gross of PIMCO called “talking out of both sides of his mouth” was significant.

Was that the beginning of the long over-due correction? After all we are now in the 52nd month of the current bull run, which has been the duration of the past two.

With news that the Japanese market lost more than 7% overnight following our own key reversal day was the sense that the correction may take on crash-like qualities, but instead our own markets almost had another key reversal day, but this time in the other direction. After an early 150 point drop and subsequent recovery all that was missing was to have exceeded the previous day’s high point.

Correction? Crash? That was so yesterday. It’s time to move on, dummy

While hopeful that some kind of correction might bring some meaningful opportunities to pick up some bargains, the correction was too shallow and the correction to the correction was too quick.

So this week is more of the same. Nearly 50% cash and no place to go other than to be mindful of a great 1995 article by Herb Greenberg that has some very timeless investing advice in the event of a crash, having drawn upon some Warren Buffett, Bob Stovall and Jeremy Siegel wisdom.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details).

Already owning shares of both Deere (DE) and Caterpillar (CAT), as I often do, a frequent companion is their more volatile counter-part, Joy Global (JOY). Always sensitive to news regarding the Chinese economy, Joy Global reports earnings this week, as well, which certainly adds to its risk profile. Most recently the news coming out of China has pointed toward slowing growth, although historically the Chinese data have demonstrated as much ability to contradict themselves longitudinally as the US data. I believe bad news is already incorporated into the current prices of the heavy machinery sector and all three of these companies are trading within a long established price range that provides me some level of comfort, even in a declining market. For that reason, I may also add shares of Deere, particularly if it approaches $85.

Morgan Stanley (MS) has gone along the uphill ride with the rest of the financial sector in recent weeks. It was among the many stocks whose shares I lost to assignment at the end of the May 2013 cycle, but it too, has been a constant portfolio companion. It tends to have greater European exposure than its US competitors, but for the time being it appears as if much of the European drama is abating. Over the past year it’s shares have traded in a wide range but has shown great resilience when the price has been challenged and has offered very attractive premiums to help during the periods of challenge.

Unlike the prior week, this past week wasn’t very good for the retailers. WIth earnings now past, one of the elite, JW Nordstrom (JWN) goes ex-dividend this week. While it still has downside room, even after a 3% earnings related drop along with the rest of the more “high end” oriented retailer sector, it will likely out-perform other lesser retailers in the event of a market pause.

Also in the higher end range, Michael Kors (KORS) has been one of my recent favorites, although I must admit I didn’t see the reason for the excitement on a retail level during a recent early morning trip to the mall. No matter, I’m not in their demographic. What I do know is that their shares move with great ease in either direction, other reversing course during the trading session and it offers an appealing option premium. That premium is a bit more enhanced as it reports earnings this week and I may look to establish a position after having shares also assigned recently.

I approach any purchases in the Technology sector with some concern for being over-invested in such shares. Although Cypress Semiconductor (CY) is now trading 10% higher from where I had shares recently assigned on two previous occasions it continues to offer a reasonably attractive options premium and trades in a stable price range.

Lexmark (LXK) is now well above the strike price that I had shares recently assigned. It’s appeal is enhanced by being ex-dividend this week and the knowledge that it appears to have gotten beyond the initial shock that this “printer maker” was getting out of the “Printer maker” business. Thus far, it appears as if the transition to a more content management and solutions oriented company is proceeding smoothly.

Also going ex-dividend this week is one of the little known, but largest owner of television stations around the nation. Sinclair Broadcasting (SBGI). It may be in position to pick up a rare gem as an ABC station in Washington, DC is rumored to be available for purchase. While it has appreciated significantly in the past two months, it’s shares are down approximately 7% from recent highs.

Not that I would suggest lighting up one of their products while watching a fine situation comedy being broadcast by SInclair, but Lorillard (LO), which assuages some of its health related guilt by offering a rich dividend, does go ex-dividend this week. It too, has been trading higher of late, but is down just a bit from its recent high.

Finally, Salesforce.com (CRM) reported earnings after this past Thursday’s (May 23, 2013) closing bell. The market assessed an 8% penalty for its disappointing numbers, but that should just be a minor bump in their road and not likely a deep pothole. Unfortunately, I didn’t execute the earnings related put sale trade last week as I thought I might, which would have returned 1% even in the face on an 8% drop in share price, but this week brings new opportunity, only on the share purchase and option sale side.

In fact, I was so convinced by the previous paragraph that I sent out that Trading Alert on Friday rather than waiting for Tuesday.

Traditional Stocks: Cypress Semiconductor, Deere, Morgan Stanley, Salesforce.com

Momentum Stocks: none

Double Dip Dividend: JW Nordstrom (ex-div 5/29), Lexmark (ex-div 5/29), Lorillard (ex-div 5/29), Sinclair Broadcasting ex-div 5/29)

Premiums Enhanced by Earnings: Joy Global (5/30 AM), Michael Kors (5/29 AM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Weekend Update – April 7, 2013

I’m was beginning to feel like one of those Pacific Island soldiers that never found out World War II had ended and remained ever-presently vigilant for an impending attack that never came.

I’m was beginning to feel like one of those Pacific Island soldiers that never found out World War II had ended and remained ever-presently vigilant for an impending attack that never came.

Amazingly, some held up their vow to defend for decades while I’m having difficulty after a bit more than a month waiting for a correction. Nothing big, just in line with this same time period in 2012, as I see lots of similarities to that time, not only in the parallel nature of the charts, but also in my own less than stellar performances, having been selling covered options as religiously as a sentinel keeps an eye on the horizon.

Having weathered the acute shock value of Cyprus, decreasing economic growth in China, currency manipulation in Japan and digested the initial uncertainty of the Korean Peninsula, it looked as if any sentinel for a sell-off would be a lonely soldier.

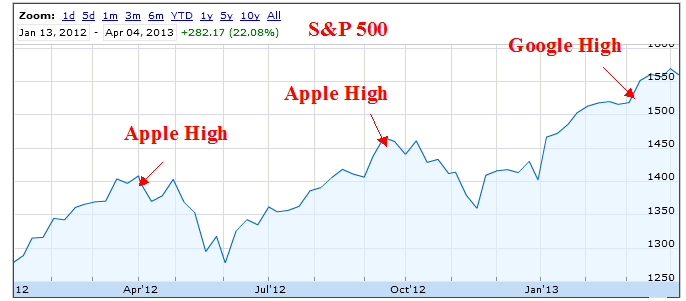

Now faced with a disappointing employment situation there’s opportunity to wonder over the weekend whether the pole has been sufficiently greased or whether this is simply the very quick mini sell-off of April 2012 that occurred just as Apple (AAPL) hit its high, then quickly recovered, just in time to lead to a 9% sell-off.

Apple had came off its April high by 5% at that point that the greater market downturn began, which is that same point that Google (GOOG) was down from its recent high point, at the close of Thursday’s trading (April 4, 2013). Coincidentally, that was the day before today’s sell-off. For those that have believed that Google has rotated into market leadership, having wrestled the position away from Apple, that may be a cause for concern. as does the fact that Google has traded below that dreaded 50 Day Moving Average.

I don’t know much about those kind of technical factors, but I do recognize that sometimes there is a basis for deja vu being more than just a feeling. What actually exists over the horizon is still anyone’s guess, but unlike those lonely soldiers you can feel relatively assured that at some point an unwelcome visitor will appear and wreak some havoc on the market. From my perspective that comes along every 52 months, so I’m not quite ready to accept that the time has come to drop defenses, but there may be room to let the guard down a bit.

I don’t know much about those kind of technical factors, but I do recognize that sometimes there is a basis for deja vu being more than just a feeling. What actually exists over the horizon is still anyone’s guess, but unlike those lonely soldiers you can feel relatively assured that at some point an unwelcome visitor will appear and wreak some havoc on the market. From my perspective that comes along every 52 months, so I’m not quite ready to accept that the time has come to drop defenses, but there may be room to let the guard down a bit.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum and “PEE” categories, as earnings season begins anew on April 8, 2013 (see details). Additionally, for the first time in a few weeks there is a somewhat greater emphasis on Momentum stocks, as a coming downslide might reasonably be expected to unduly impact upon issues that have thrived recently, particularly the more defensive stocks. However, I am still inclined to consider monthly contracts over weekly ones, simply for a little extra breathing room while continuing to await a market heading in a southerly direction.

One Momentum stock that has also thrived up until very recently is YUM Brands (YUM). It also happens to go ex-dividend this week and has already given back much of its gains in the absence of any news. In the past it has demonstrated itself very capable of bouncing back from both real news and speculation regarding its forward prospects. Simultaneously being held hostage to the Chinese economy and also proving to be independent of swirling winds, YUM Brands serves as a model of what can be achieved in a marketplace where the playing field is anything but level.

A real signal that something is evolving, at least from my perspective, is that I no longer classify AIG (AIG) as a Momentum stock. Over the past year, had I followed by frequent suggestions that AIG might be an appropriate covered call position, I think I could have limited my portfolio to a single stock. Robert Ben Mosche, it’s CEO is the poster child for leadership and focus. With some recent share weakness, I think it may be time to add it back to a portfolio in need of income and reasonable price stability.

A couple of months ago I made an earnings related trade in F5 Networks (FFIV) that worked out nicely. Having sold puts just prior to earnings, F5 surpassed expectations and the trade was closed in 4 days. Thursday evening after the closing bell, F5 release disappointing guidance that saw its shares fall more than 15%.

I hate guidance that comes out weeks before earnings and catches me off-guard. In the past I’ve seen Cummins Engine (CMI) and Abercrombie and Fitch (ANF) seem t

o regularly upset happy shareholders with that kind of timed guidance. Despite the fact that analysts seem to be in agreement that this is solely an F5 issue, it indiscriminately drags down the sector, perhaps offering opportunities.

In this case, I think the opportunities are now in both Cisco (CSCO) and Riverbed Technology (RVBD), both unduly hit in the aftermath of F5 and just a couple of weeks ago by Oracle’s (ORCL) disappointing earnings, which were also agreed to be an Oracle specific shortcoming. I currently own shares of Riverbed and would even consider adding to the position ahead of earnings later in the month.

Western Refining (WNR) returns to the list from last week, as an unrequited purchase. It is, possibly another example of how the market acts indiscriminately and emotionally. Following Valero’s (VLO) moaning about the costs of upcoming EPA initiatives for cleaner gas the market punished the entire sector, despite the fact that the EPA suggested that the costs of compliance were minimal for most refiners. The market made no distinction and assumed that all refiners would be subject to additional costs similar to the $300-400 million suggested by Valero. Unfortunately, I didn’t have the fortitude to pick up shares of Western Refining as it briefly dipped below $30 or Phillips 66 (PSX) as it fell about 10%. It didn’t stay there very long and certainly never confirmed the worst case scenario that Valero so openly shouted.

MetLife (MET) also returns from last week, which was another week of hesitancy to commit cash in favor of building reserves. There were, however, a number of times that I was ready to part with some of the cash, but ultimately resisted. As opposed to Western Refining, MetLife’s shares went down even further, so those decisions to embrace inaction may have balanced one another out. I continue to believe that shares will benefit from an increasingly healthy housing market, although that is far from MetLife’s core and highest profile business.

The financial sector was hit quite hard this past week. Since I owned shares of both Morgan Stanley (MS) and JP Morgan (JPM), I was acutely aware of their duress. However, in addition to JP Morgan and Wells Fargo (WFC) releasing earnings this Friday and perhaps representing some opportunity, Bank of America (BAC), whose shares I had assigned just a week ago has given up much of its recent run-up higher and is becoming attractive again.

Finally, Bed Bath and Beyond (BBBY) s one of my favorite stores, but not one of my favorite stocks. It has had a bit of a price rise on some buy-out speculation and it has demonstrated past ability to disappoint on earnings. Already down about 4% from its very recent high, I would be comfortable owning shares at $60 and would consider a 1.5% ROI for a 2 week holding period to be a decent reward while anticipating less than a 5% decline in share price in the after-math of earnings.

Traditional Stocks: AIG, Cisco, MetLife

Momentum Stocks: Bank of America, Riverbed Technology, Western Refining,

Double Dip Dividend: YUM Brands (ex-div 4/10)

Premiums Enhanced by Earnings: JP Morgan (4/12 AM), Pier 1 (4/11 AM), Wells Fargo (4/12 AM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Some of the stocks mentioned in this article may be viewed for their past performance utilizing the Option to Profit strategy.

Weekend Update – March 24, 2013

Common sense tells us that at some point there has to be some retracement following an impressive climb higher. My common sense has never been very good, so I’m beginning to question the pessimism that overtook me about 4 weeks ago.

Common sense tells us that at some point there has to be some retracement following an impressive climb higher. My common sense has never been very good, so I’m beginning to question the pessimism that overtook me about 4 weeks ago.

Maybe the new version of a market plunge is simply staying at or near the same level for a few days. After all, who doesn’t believe that if you’re not moving ahead that you’re falling behind? It is all about momentum and growth. Besides, if history can be re-written by the victors, why not the rules that are based on historical observations?

During the previous 4 weeks I’ve made very few of the trades that I would have ordinarily made, constantly expecting either the sky to fall down or the floor to disappear from underneath. Of the trades, most have fallen in line with the belief that what others consider a timeless bit of advice. Investing in quality companies with reliably safe dividends may be timeless, but it can also be boring. Of course, adding in the income from selling options and it’s less so, but perhaps more importantly better positioned to cushion any potential drops in an overall market.

That makes sense to me, so there must be something flawed in the reasoning, although it did work in 2007-2009 and certainly worked in 1999-2000. I can safely say that without resorting to a re-writing of history.

Among the areas that I would like to consider adding this week are healthcare, industrials and financial sectors, having started doing so last week with Caterpillar (CAT) and Morgan Stanley (MS).

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend or “PEE” categories, with no selections in the “Momentum” category, befitting common sense. (see details). Additionally, there is a greater emphasis on stocks that offer monthly contracts only, eschewing the usual preference for the relatively higher ROI of weekly options for the guarantee of premiums for a longer period in order to ride out any turbulence.

Deere (DE) has been unnecessarily caught in the headlights recently, as it frequently trades in parallel to other heavy machinery giants, despite Deere not having the same kind of global economic exposure. The fact that it goes ex-dividend this week and always offers a reasonable premium, even when volatility is low, makes it a good selection, especially at its current price, which is down about 8% in a time that the S&P 500 has been up 3%. That seems a bit incongruous.

State Street Bank (STT) also goes ex-dividend this week. At a time when banks with global interests are at risk due to European Union and Euro related issues, State Street is probably the lowest profile of all of our “too big to fail” banks that play with the “big boys” overseas. Despite a marked climb, particularly from mid-January, it has shown resistance to potentially damaging international events.

While State Street Bank looks appealing, I have wanted to pick up shares of JP Morgan (JPM) for the past couple of weeks as it and its one time invincible CEO and Chairman, have come under increasing scrutiny and attack. Although it doesn’t pay a dividend this week, if purchased and call options are not assigned, it does offer a better dividend to holders than State Street and will do so on April 3, 2013. Better yet, Jamie Dimon will be there to oversee the dividend as both CEO and Chairman, as the Board of Directors re-affirmed his dual role late Friday afternoon, to which shares showed no response.

If you’re looking for a poster child to represent the stock market top of 2007, then look no further than Blackstone (BX). It was even hotter than Boston Chicken of a generation earlier, and it, too, quickly left a bad after taste. Suddenly, Blackstone no longer seems irrelevant and its name is being heard more frequently as buyouts, mergers and acquisitions are returning to the marketplace, perhaps just in time for another top.

Back in the days when I had to deal with managed care health companies, I wasn’t particularly fond of them, perhaps because I was wrong in the early 1980s when I thought they would disappear as quickly as they arrived. As it turns out, it was only the managed care company on whose advisory board I served that left the American landscape for greener pastures in The Philippines. Humana, one of the early managed care companies at that time was predominantly in the business of providing health care. These days it’s divested itself of that side of the social contract and now markets and offers insurance products.

Humana (HUM) is a low volatility stock as reflected in its “beta” of 0.85 and is trading close to its two year low. The fear with Humana, as with other health care with a large Medicare population is that new reimbursement rates, which are expected to be released on April 1, 2013 will be substantially lower. Shares have already fallen more almost 20% in the past 6 weeks at a time when insurers, on the other side of the equation, have fared well.

UnitedHealth Care (UNH) is the big gorilla in the healthcare room. It has real

ly lagged the S&P 500 ever since being add to the DJIA. However, if your objective is to find stocks upon which you can generate revenue from dividends and the sale of option premiums, you really don’t need much in the way of share performance. In fact, it may be antithetical to what you really want. UnitedHealth Group, though, doesn’t have the same degree of exposure to Medicare fees, as does Humana.

While the insurers and the health care providers battle it out between themselves and the government, there’s another component to healthcare that comes into focus for me this week. The suppliers were in the news this week as Cardinal Health (CAH) reportedly has lost its contract with Walgreens (WAG). Cardinal Health and Baxter (BAX) do not do anything terribly exciting, they just do somethings that are absolutely necessary for the provision of healthcare, both in formal settings and at home. Although also subject to Medicare reimbursement rates and certainly susceptible to pricing pressure from its partners, they are consistently reliable companies and satisfy my need to look for low beta positions. Besides their option premiums, Cardinal Health also goes ex-dividend this week.

Then again, what’s healthcare without pharmaceuticals? Merck (MRK) is another of those companies whose shares I’ve wanted to buy over the past few weeks. It’s now come down from its recent Vytorin related high and may round out purchases in the sector.

With the safe and boring out of the way, there are still a few laggard companies that have yet to report their quarterly earnings before the cycle starts all over again on April 8th. Of those, one caught my attention.

Why anyone goes into a GameStop (GME) store is beyond me. Yet, if you travel around the country you will still see the occasional Blockbuster store, as well. Yet, somehow GameStop shares tend not to suffer terribly when earnings are released, although it is very capable of making large moves at any other time. The current proposition is whether the sale of puts to derive a 2.8% ROI in the event of less than a 12% decline in share price is worthwhile.

Now that’s a challenging game and you don’t even have to leave home to play it.

Traditional Stocks: Baxter, Blackstone, JP Morgan, UnitedHealth Group

Momentum Stocks: none

Double Dip Dividend: Cardinal Health (3/27), Deere (3/26), Humana (3/26), State Street Bank (3/27)

Premiums Enhanced by Earnings: GameStop (3/28 AM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

Some of the stocks mentioned in this article may be viewed for their past performance utilizing the Option to Profit strategy.

Weekend Update – March 10, 2013

It only seems fitting that one of the final big stories of the week that saw the Dow Jones eclipse its nearly 6 year old record high would be the latest reports of how individual banks performed on the lmost recent round of “stress tests.” After all, it was the very same banks that created significant national stress through their equivalent of bad diet, lack of exercise and other behavioral actions.

It only seems fitting that one of the final big stories of the week that saw the Dow Jones eclipse its nearly 6 year old record high would be the latest reports of how individual banks performed on the lmost recent round of “stress tests.” After all, it was the very same banks that created significant national stress through their equivalent of bad diet, lack of exercise and other behavioral actions.

Just as I know that certain foods are bad for me and that exercise is good, I’m certain that the banks knew that sooner or later their risky behavior would catch up with them. The difference is that when I had my heart attack the effects were restricted to a relatively small group of people and I didn’t throw any one out of their homes.

Having had a few stress tests over the years myself, I know that sometimes the anticipation of the results is its own stress test. But for some reason, I don’t believe that the banks that were awaiting the results are facing the same concerns. Although I’m only grudgingly modifying my behavior, it’s not clear to me that the banks are or at least can be counted to stay out of the potato chip bag when no one is looking.

Over the past year I’ve held shares in Goldman Sachs (GS), JP Morgan Chase (JPM), Wells Fargo (WFC), Citibank (C), Bank of America (BAC) and Morgan Stanley (MS), still currently holding the latter two. They have been, perhaps, the least stressful of my holdings the past year or so, but I must admit I was hoping that some among that group would just go and fail so that they could become a bit more reasonably priced and perhaps even drag the market down a bit. But in what was, instead, a perfect example of “buy on the rumor and sell on the news,” success led to most stressed bank shares falling.

The other story is simply that of the market. Now that its surpassed the 2007 highs it just seems to go higher in a nonchalant manner, not giving any indication of what’s really in the works. I’ve been convinced for the past 2 or three weeks that the market was headed lower and I’ve taken steps for a very mild Armageddon. Raising cash and using longer term calls to cover positions seemed like a good idea, but the only thing missing was being correct in predicting the direction of the market. For what it’s worth, I was much closer on the magnitude.

The employment numbers on Friday morning were simply good news icing on the cake and just added to my personal stress, which reflected a combination of over-exposure to stocks reacting to speculation on the Chinese economy and covered call positions in a climbing market.

Fortunately, the news of successful stress test results serves to reduce some of my stress and angst. With news that the major banking centers have enough capital to withstand severe stresses, you do have to wonder whether they will now loosen up a bit and start using that capital to heat up the economy. Not to beat a contrarian horse to death, but since it seems inevitable that lending has to resume as banking portfolios are reaching maturity, it also seems inevitable that the Federal Reserve’s exit strategy is now in place.

For those that believe the Federal Reserve was the prime sponsor of the market’s appreciation and for those who believe the market discounts into the future, that should only spell a market that has seen its highs. Sooner or later my theory has to be right.

I’m fine with that outcome and would think it wonderfully ironic if that reversal started on the anniversary of the market bottom on March 10, 2009.

But in the meantime, individual investment money still has to be put to work. Although I continue to have a negative outlook and ordinarily hedge my positions by selling options, the move into cash needs to be hedged as well – and what better way to hedge than with stocks?

Not just any stocks, but the boring kind, preferably dividend paying kind, while limiting exposure to more controversial positions. People have their own unique approaches to different markets. There’s a time for small caps, a time for consumer defensive and a time for dividend paying companies. The real challenge is knowing what time it is.

As usual, this week’s selections are categorized as being either Traditional, Momentum or Double Dip DIvidend (see details). As earnings season is winding down there appear to be no compelling earnings related trades in the coming week.

Although my preference would be for shares of Caterpillar (CAT) to approach $85, I’m heartened that it didn’t follow Deere’s (DE) path last week. I purchased Deere and subsequently had it assigned, as it left Caterpillar behind, for the first time in 2013, as they had tracked one another fairly closely. With the latest “news du jour” about a Chinese government commitment to maintaining economic growth, there may be enough positive news to last a week, at which point I would be happy to see the shares assigned and cash redeployed elsewhere.

Along with assigned shares of Deere were shares of McGraw Hill (MHP). It’s price spiked a bit early in the week and then returned close enough to the strike price that a re-purchase, perhaps using the same strike price may be a reasonable and relatively low risk trade, if the market can mai

ntain some stability.

There’s barely a day that goes by that you don’t hear some debate over the relative merits of Home Depot (HD) and Lowes (LOW). Home Depot happens to be ex-dividend this week and, unless it causes havoc with you need to be diversified, there’s no reason that both companies can’t be own concurrently. Now tat Lowes offers weekly options I’ve begun looking more frequently at its movement, not just during the final week of a monthly option cycle, which coincidentally we enter on Monday.

I rarely find good opportunity to purchase shares of Merck (MRK). It’s option premium is typically below the level that seems to offer a fair ROI. That’s especially true when shares are about to go ex-dividend. However, this week looks more appealing and after a quick look at the chart there doesn’t appear to be much more than a 5% downside relative to the overall market.

Macys (M) is another company that I’ve enjoyed purchasing to capture its dividend and then hold until shares are assigned. It’s trading about 6% higher than when I last held shares three weeks ago and is currently in a high profile legal battle with JC Penney (JCP). There is certainly downside in the event of an adverse decision, however, it now appears as if the judge presiding over the case may hold some sway as he has suggested that the sides find a resolution. That would be far less likely to be draconian for any of the parties. The added bonuses are that Macys is ex-dividend this week and it too has been added to the list of those companies offering weekly option contracts.

Cablevision (CVC) is one of New York’s least favorite companies. The distaste that people have for the company goes well beyond that which is normally directed at utilities and cable companies. There is animus director at the controlling family, the Dolans, that is unlike that seen elsewhere, as they have not always appeared to have shareholder interests on the list of things to consider. But, as long as they are paying a healthy dividend that is not known to be at risk, I can put aside any personal feelings.

Michael Kors (KORS) isn’t very consistent with the overall theme of staid, dividend paying stocks. After a nice earnings related trade a few weeks ago and rise in share price, Kors ran into a couple of self-made walls. First, it announced a secondary offering and then the founder, Michael Kors, announced a substantial sale of personal shares. It also may have more downside potential if you are one that likes looking at charts. However, from a consumer perspective, as far as retailers go, it is still” hot” and offers weekly options with appealing enough premiums for the risk. This turned out to be one of the few selections for which I couldn’t wait until the following week and sent out a Trading Alert on Friday morning.