Shades of 1999.

I’m not certain that I understand the chorus of those claiming that our current market reminds them of 1999.

Mind you, I’m as cautious, maybe much more so than the next guy and have been awaiting some kind of a correction for more than 2 months now, but I just don’t see the resemblance.

Much has also been made of the fact that the S&P 500 is now some 12% above its 200 Day Moving Average, which in the past has been an untenable position, other than back when sock puppets were ruling the markets. Back then that metric was breached for years.

Back in 1999 and the years preceding it, the catalyst was known as the “dot com boom” or “dot com bubble” or the “dot com bust,” depending on what point you entered. The catalyst was clear, perhaps best exemplified by the ubiquitous sock puppet and the short lived PSINet Stadium, back then home to the world Champion Baltimore Ravens. The Ravens survived, perhaps even thrived since then, while PSINet was a casualty of the excesses of the era. When it was all said and done you could stuff PSINet’s assets into a sock.

During the height of that era the catalyst was thought to be in endless supply. But in the current market, what is the catalyst? Most would agree that if anything could be identified it would likely be the Federal Reserve’s policy of Quantitative Easing.

But as last week’s rumor of its upcoming end and then an article suggesting that the Federal Reserve already has an exit plan, the catalyst is clearly not thought to be unending. Unless the economy is much worse than we all believe it to be the fuel will be depleted sooner rather than later.

Now if you’re really trying to find a year comparable to this one, look no further than 1995, when the market ended the year 34% higher and never even had anything more than a 2% correction.

If llke me, and you’re selling covered options; let’s hope not.

For me, this Friday marked the end of the May 2013 option cycle. As I had been cautious since the end of February and transitioned into more monthly option contract sales, I am faced with a large number of assignments. Considering that the market has essentially been following a straight line higher having so many assignments isn’t the best of all worlds.

While I now find myself with lots of available cash the prevailing feeling that I have is that there is a need to protect those assets more than before in anticipation of some kind of correction, or at least an opportunity to discover some temporary bargains.

This week I have more than the usual number of potential new positions, however, I’m unlikely to commit wholeheartedly to their purchase, as I would like to maintain about a 40% cash position by the end of next week. I’m also more likely to continue looking at monthly option sales rather than the weekly contracts.

As usual, the week’s potential stock selections are classified as being in Traditional, Double Dip Dividend, Momentum or the “PEE” category (see details). Additionally, although the height of earnings season has passed there may still be some more opportunity to sell well out of the money puts prior to earnings on some reasonably high profile names..

There’s no doubt that the tone for the week was changed by the down to earth utterances of David Tepper, founder of the Appaloosa Hedge Fund. He has a long term enviable record and when he speaks, which isn’t often, people do take notice. Apparently markets do, as well.

However, among the things that he mentioned was that he had lightened up on his position in Apple (AAPL). It didn’t take long for others to chime in and Apple shares fell substantially even when the market was going higher. Although I was waiting for Apple to get back into the $410-420 range, the rebound in share price following news of reduced positions by high profile investors is a good sign and I believe warrants consideration toward the purchase of new shares.

I recently purchased shares of Sunoco Logistics (SXL) in order to capture its generous and reliable dividend. My shares were assigned this past Friday, but I’m willing to repurchase, even at a higher price and even with a monthly option contract to tie me down. In the oil services business it is a lesser known entity and trades with low volume, however, it will share in sector strength, just in a much more low profile manner.

Pfizer (PFE) is another stock that was recently purchased in order to capture it’s dividend and premium and was also assigned this past week. However, it is among the “defensive” stocks that I think would fare relatively well regardless of near term market direction. Like many others that do offer weekly options, my inclination is to consider the selling monthly contracts for the time being.

While healthcare has certainly already had its time in the sun in 2013 and Bristol Myers Squibb (BMY) has had its share of that glory, after some recent tumult in its price and most recently its next day reversal of a strong move the previous day, I find the option premium appealing. However, as opposed to Pfizer, which I’m more inclined to consider a monthly option, Bristol Myers has too much downside potential for me to want to commit for longer periods.

Although I already own shares of Petrobras (PBR) and am not a big fan of adding additional shares after such a strong climb hig

her off of its rapidly achieved lows, Petrobras recently and quietly had quite an achievement. WHile everyone was talking about Apple’s $17 Billion bond offering that had about $50 Billion in bids, Petrobras just closed an $11 Billion offering with more than $40 Billion in bids.

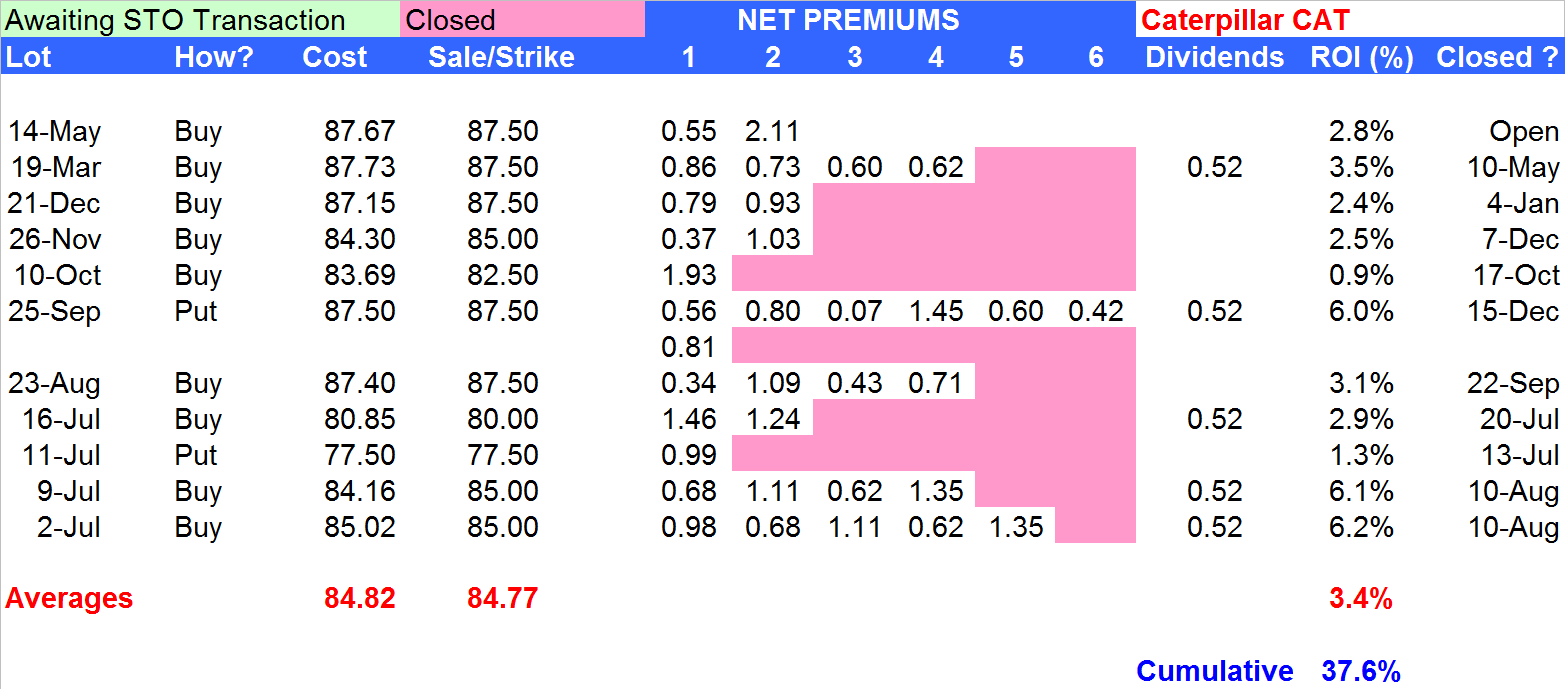

Caterpillar (CAT), which I also currently own, is a perennial member of my portfolio. To a very large degree it has been recently held hostage to rumors of contraction and slowing in the Chinese economy. It has, however, shown great resiliency at the current price level and has been an excellent vehicle upon which to sell call options.

As shown in the table above, I’ve owned shares of Caterpillar on 11 separate occasions in less than a year. While the price has barely moved in that period, the net result of the in and out trades, as a result of share assignments has been a gain in excess of 35%.

As shown in the table above, I’ve owned shares of Caterpillar on 11 separate occasions in less than a year. While the price has barely moved in that period, the net result of the in and out trades, as a result of share assignments has been a gain in excess of 35%.

The more ambiguity and equivocation there is in understanding the direction of the Chinese economy the better it has been to own Caterpillar as it just bounces around in a fairly well defined price range, making it an ideal situation for covered call strategies.

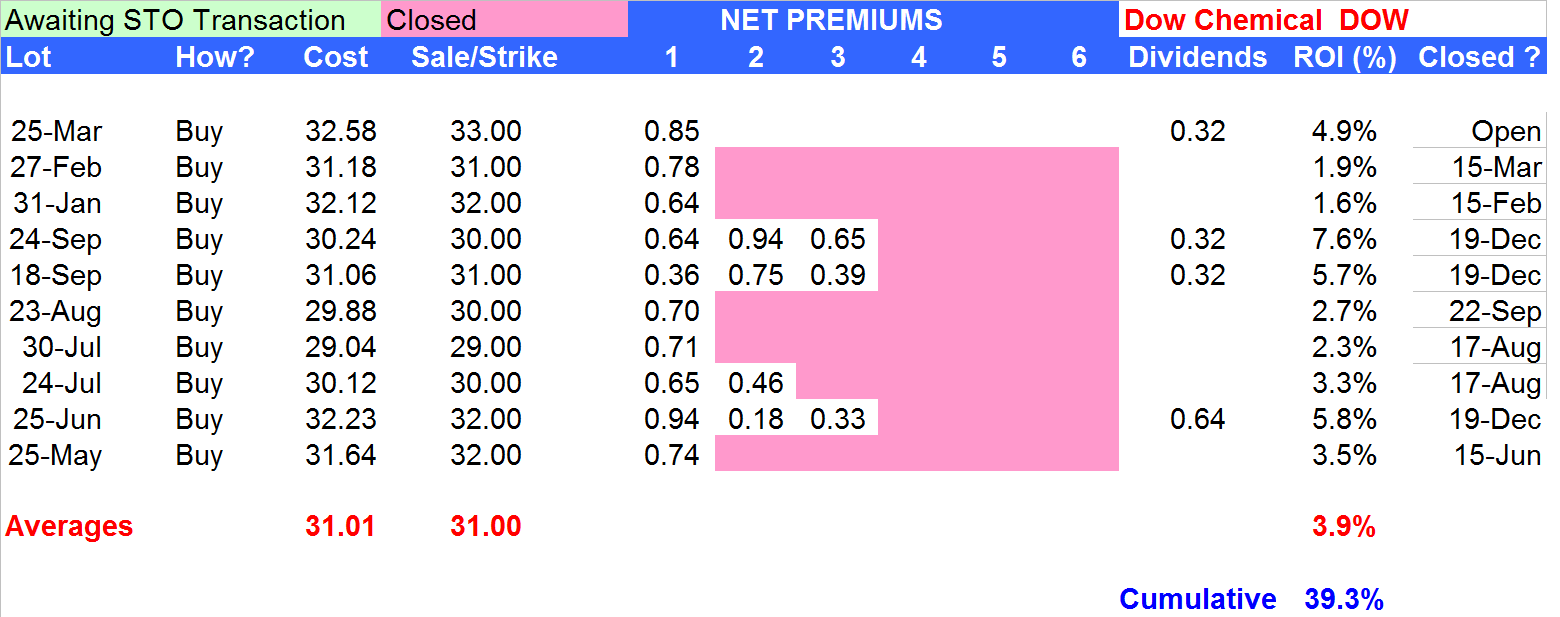

Continuing the theme of shares that I currently own, but am considering adding more shares, is British Petroleum (BP). With much of its Deepwater Horizon liabilities either behind it or well defined, shares appear to have a floor. However, in the past year, that has already been the case, as my experience with British Petroleum ownership has paralleled that of Caterpillar in both the number of separate times owning shares and in return – only better.

Of course, better than either Caterpillar or British Petroleum has been Chesapeake Energy (CHK). I’ve owned it 18 times in a year. It too has had much of its liability removed as Aubrey McClendon has left the scene and it is already well known that Chesapeake will be selling assets under a degree of duress. With its turnaround on Thursday and dip below $20, I am ready to add even more shares.

I’ve probably not owned Conoco Phillips (COP) as much as I would have imagined over the past year probably As a result of owning British Petroleum and Chesapeake Energy so often. Shares do go ex-dividend this week which always adds to the appeal, particularly when I’m in a defensive mode.

Salesforce.com (CRM) was a recommendation last week. I did make that purchase and subsequently had shares assigned. This week it reports earnings and as many of the earnings related trades that I prefer, it offers what I believe to be a good option premium even in the event of a large downward move. In this case a 1% return for the week may be achieved if share price doesn’t exceed 8%

Sears Holdings (SHLD) always seems like a ghost town when I enter one of its stores, although perhaps a moment of introspection would indicate that I drive shoppers away. I’m aware of other story lines revolving around Sears and its real estate holdings, but tend not to think in terms of what has been playing out a s a very, very long term potential. Instead, I like Sears as a hopefully quick earnings trade.

In a week that saw beautiful price action from Macys (M), Kohls (KSS) and others, perhaps even Sears can pull out good numbers and even provide some positive guidance. However, what appeals to me is a put sale approximately 8% below Friday’s close that could offer a 4% ROI for the month or shorter.

Another retailer, The Gap (GPS), has certainly been an example of the ability to arise from the ashes and how a brand can be revitalized. Along with it, so too can its share price. The Gap reports earnings this week and has already had an impressive price run. As opposed to most other earnings related trades, I’m not looking for a significant downward move and the market isn’t expecting such a move either. Based on some of the strong retail earnings announced this past week I think The Gap may be an outright purchase, but I would be more likely to look at a weekly option sale and hope for quick assignment of shares.

TIVO (TIVO) is one of those technologies that I’ve never adopted. Maybe that’s because I never leave the house and the television is always on and I rarely see a need to change the station. But here, too, I believe TIVO offers a good short term opportunity even if shares go down as much as 20% following Monday’s earnings release. In the event that shares go appreciably higher, it is the ideal kind of earnings trade, in that coming during the first day of a monthly option contract, it could likely be quickly closed out and the money then used for another investment vehicle.

Om the other hand, Dunkin Brands (DNKN) is definitely one of those technologies that I’ve adopted, especially when having lived in New England. Fast forward 20 years and they are now everywhere in the Mid-Atlantic and spreading across the country as their new offerings also spread waists around the country. Going ex-dividend this coming week and offering a nice monthly option premium, I may bite at more than a jelly donut. However, it is trading at the upper end of its recent price range, like all too many other stocks.

Finally, Carnival (CCL) hasn’t exactly been the recipient of much good news lately. Although it’s up from its recent woes and lows. It does report earnings at the end of the June 2013 option cycle, but it also goes ex-dividend in the first week of the cycle, in addition to a offering a reasonable option premium

Traditional Stocks: Bristol Myers, Caterpillar, Pfizer, Sunoco Logistics

Momentum Stocks: Apple, Chesapeake Energy, Petrobras

Double Dip Dividend: Carnival Line (ex-div 5/22), Conoco Phillips (ex-div 5/22), Dunkin Brands (ex-div 5/23)

Premiums Enhanced by Earnings: Salesforce.com (5/23 PM), Sears Holdings (5/23 AM), The Gap (5/23 PM), TIVO (5/20 PM)

Remember, these are just guidelines for the coming week. Some of the above selections may be sent to Option to Profit subscribers as actionable Trading Alerts, most often coupling a share purchase with call option sales or the sale of covered put contracts. Alerts are sent in adjustment to and consideration of market movements, in an attempt to create a healthy income stream for the week with reduction of trading risk.

A long time ago there was a reasonably popular song by a group that itself was reasonably popular at a time when Disco was dying, Punk Rock had out-grown its shock factor and Heavy Metal and long hair bands were taking root.

A long time ago there was a reasonably popular song by a group that itself was reasonably popular at a time when Disco was dying, Punk Rock had out-grown its shock factor and Heavy Metal and long hair bands were taking root. (A version of this article appeared in

(A version of this article appeared in  As an example, I’m going to look at Petrobras (PBR) shares that I bought on January 7, 2013 at $20.05 and currently trading at $13.48. An advanced degree is mathematics is unnecessary to recognize that represents more than a 10% decline and would violate investing rules sometimes attributed to famed financier Bernard Baruch.

As an example, I’m going to look at Petrobras (PBR) shares that I bought on January 7, 2013 at $20.05 and currently trading at $13.48. An advanced degree is mathematics is unnecessary to recognize that represents more than a 10% decline and would violate investing rules sometimes attributed to famed financier Bernard Baruch.